2024 Investment Environment: Treasuries on Top

The year begins with a fresh look at the public funds investment universe. Since most public sector investment policies limit investments by maturity and quality we focus on the universe of high-quality investment grade securities with maturities of three years or less. Excluded are foreign-issued securities and corporate bonds rated less than A.

The big picture.

- Treasuries dominate the market. This dominance has increased in recent years as Treasury issuance has mushroomed. The growing supply of risk-free highly liquid investments offers a safe haven for public funds investments though the yield is often lower than that of investments with similar maturity that are not as safe or liquid.

- The continued growth of Treasury issuance will put pressure on corporate and other issuers to “pay-up” to compensate for the higher risk and lower liquidity associated with their securities.

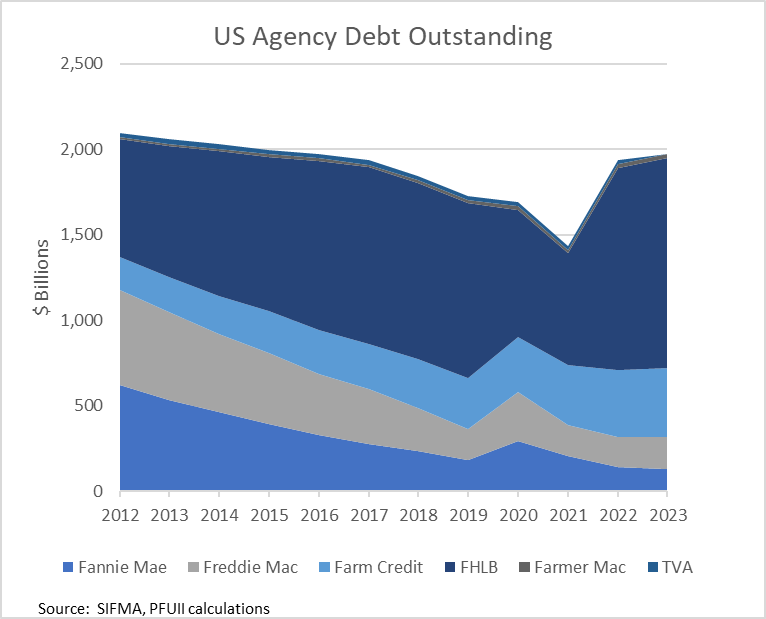

- Federal agency/GSE debt is a shrinking presence in the market as issuance has contracted over the past decade. The character of Agency/GSE debt has shifted so the sector is now dominated by the FHL Banks.

- Investment grade credit instruments make up less than 20% of the universe. The volume has grown slowly, so it is a smaller segment of the universe than it was five years ago. But trading volume has grown, leading to a more liquid market.

- The supply of investments normally included in public funds portfolios is concentrated in the front-end of the market, with money market securities (maturing in 12 months or less) constituting nearly two-thirds of the 0–3-year universe.

The bottom line. We expect growing Treasury volume, shrinking Agency issuance and stable credit volumes in 2024. With spreads at historically narrow levels the risk/liquidity premium for investing in securities other than Treasuries is low.

The detail. Treasuries dominate the maturity-constrained public funds investment market. In the universe limited to Treasuries, Agencies and domestic investment grade credit instruments rated “A” or better, Treasuries make up about 72% of investment securities. Treasury volume is expected to increase this year by $1.4 trillion or nearly 10% overall driven entirely by increased Treasury issuance.

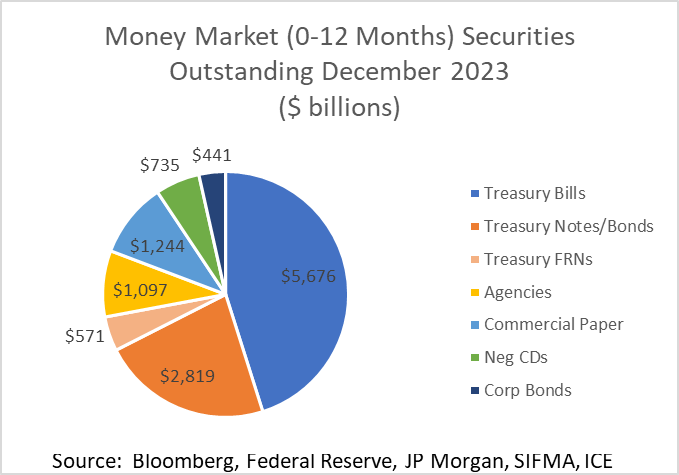

The Money Market Segment. The universe of money market securities is even more heavily weighted to Treasuries.

Treasury bills, notes and bonds represent 72% of outstandings at the end of 2023 and the total is forecast to rise by $675 billion to 74% of outstandings. More than 81% of investment opportunities will be in Treasuries and Agencies this year.

The increase in Treasury Bill is, of course, related to financing the Federal deficit, now estimated at $1.8 trillion. It continues a trend of rising Bill issuance that stretches back a decade and is an element in the dramatic shift in money markets over this period.

A look-back 10 years paints a dramatic picture of the rise to dominance of Treasuries.

Another factor is that the commercial paper market is only about half the size at its peak in 2008, though of course the economy has expanded since then. The character of the commercial paper market has also changed over the years. Market-making and liquidity have improved for asset backed commercial paper, while dealers are hesitant to make markets in direct issue names.

Federal Agencies. Not What They Used to Be.

Not only is the Federal Agency market smaller than it has been in recent years but the composition has changed: the FHL Banks now dominate issuance. Much of the recent FHL Banks issuance has been in response to depository institutions that found a cheap source of short-term borrowing, using FLH Banks advances in place of raising deposits. The FHL Banks’ regulator, the Federal Housing Finance Agency, has recently begun pushing to scale back this aspect of

FHL Banks business and other bank regulators are also of this mind, so we estimate that FHL borrowings will fall back in 2024 toward the lower levels of 2020 and 2021.FHL Banks debt was as low as $653 billion at the end of 2021 before exploding to over $1 billion in June 2023. This pull-back is likely to accelerate in 2024 and 2025.

As a consequence of the diverging issuance trends, Treasury and Agency yield spreads, which in recent years have been as wide as 10-15 basis points, are now more likely to be in the 3-5 basis point range in 2024.

Agency/GSE debt with maturities under one year (largely issued as discount notes) declined from $718 billion in 2015 to $241 billion in 2021. While short-term debt rose last year, it is likely to bear the brunt of cuts in 2024-2025.

As a consequence government-oriented investors are likely to find opportunities outside of Treasuries are scarce and expensive (i.e., with little income advantage) in 2024.

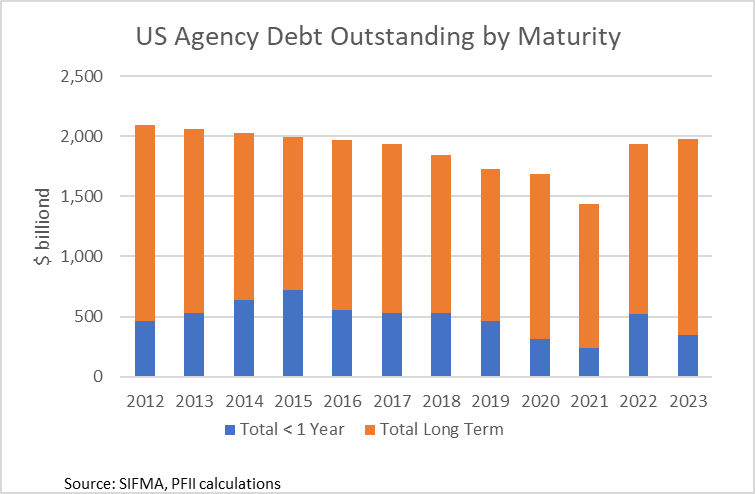

Federal agency trading volume has also declined, consistently over the last decade, implying lower liquidity and less opportunity to buy agencies on the secondary market.

What to Watch: Factors that Could Affect Supply, Demand and Value.

Beyond supply forecasts, several other factors will affect the short-term fixed income markets:

- Federal Reserve monetary policy.

- Moves to change the Federal Reserve’s policy rate (currently 5.25%-5.50%) have close to a one for one effect on short term rates. Anticipated changes in this rate will be a significant factor in rates for securities maturing beyond the overnight period and out to two years.

- The current Fed action to “taper” the quantitative easing program it undertook in early 2020 could alter marketable Treasury supply. The Fed is currently letting $65 billion of Treasuries and $35 billion in Agencies that it holds on its balance sheet mature each month without replacing them. Analysts expect this run-off to slow and/or end sometime in 2024. To slow it the Fed will have to replace some of the maturing securities by buying non-marketable Treasuries directly and this will affect the volume of Bills, notes and bonds sold to investors. To estimate the impact this would have on supply one might assume $200 billion in 2024. This factor is NOT accounted for in the forecasts shown in this Spotlight. A change or end to quantitative easing might lead the Treasury to reduce Treasury bill issuance to investors by an equivalent amount. (The impact will likely be on Treasury Bills initially because the Fed’s Bill holdings are modest—only about $200 billion—and Bills provide the most flexibility for the Fed managing its open market account.)

- Money fund asset trends.

- Money fund assets surpassed $6 trillion at the end of 2023, up 21% in the year. The inflow has been concentrated in government money market funds. Importantly they are the biggest buyer of short-term government obligations, and their appetite has a big effect on yields and liquidity of these securities. At the end of the year government money funds owned $2.2 trillion of Treasuries and $700 billion of Agencies, according to Cranedata. This represents approximately 15% of outstanding short-term (0-12 month) Treasuries and 37% of Agencies. If the recent money fund asset trend were to reverse, this could cause liquidity in these markets to weaken and yields to rise when compared with other benchmarks.

- Prime money market funds are much smaller ($1.3 trillion at year end). They grew by 23% in 2023. But their future course is a bit uncertain as they will have to accommodate the Securities and Exchange Commission’s new money fund rules this year. Some analysts speculate that the imposition of new rules will cause investors to leave prime funds. At year-end prime money market funds owned approximately $350 billion of commercial paper (according to SEC filings), 28% of the total outstanding. Market behavior in the spring of 2020 when prime money market funds were under stress suggests that even modest sudden changes in their holdings of commercial paper could cause spreads to widen dramatically and liquidity to disappear in this market.

- Regulatory policy and bank borrowing.

- At the end of the year the FHL Banks represented nearly 90% of Agency securities issued with less than one year to maturity and 57% of long term (one year or longer) maturities. FHL Banks’ regulator and commercial bank regulators have signaled that they want the banks to reduce reliance on the FHL Banks. As recently as year-end 2021, before the rise in short term interest rates the FHL Banks had only about $650 billion of outstanding debt, half of the level at the end of 2023.

- This could reduce new issuance by the FHL Banks significantly and pressure Treasury to Agency yield spreads to narrow.

- The repurchase agreement market.

- The repurchase agreement market is not included in the supply forecast for the short-term market because most public funds investors do not access repo directly, but it does have an effect on demand for other securities included in the forecast.

- At the end of 2023 outstanding dealer/bank placed repurchase agreements totaled about $2.9 trillion, and the Fed’s reverse repo facility totaled about $700 billion in late December. Money fund managers and managers of some LGIPs that are active in the repo market actively shop repo rates/opportunities with those of Treasuries, so changes in repo rates could move rates on Treasury bills.

- The Fed’s RRP facility declined in 2023 from a peak of $2.6 trillion to the year-end level of $700 billion and this put modest pressure on short-term Treasury bill rates. A continued decline toward zero, which would be consistent with the Fed’s stated monetary policy of tightening credit, could keep upward pressure on short Treasury bill rates.

- Macro-economic effects on credit.

- The year begins with credit risk premia at levels approaching historic lows. Events that disrupt the economy or threaten to weaken investment grade credit could push the spreads wider and weaken liquidity for commercial paper and corporate bonds.

- The year begins with credit risk premia at levels approaching historic lows. Events that disrupt the economy or threaten to weaken investment grade credit could push the spreads wider and weaken liquidity for commercial paper and corporate bonds.

Summing up. Government-oriented investors are likely to be increasingly oriented toward Treasuries, which will be in ample supply and are the most liquid segment of the market. Investors who seek to enhance portfolio returns by investing in credit instruments should be sensitive to the fact that liquidity/risk premia are narrow and the credit markets are more likely to be disrupted by macro-economic events.