Not Much Has Changed, Or Has It?

It’s hard to see beyond the Iran war. That’s true of it’s humanitarian, but also of its economic/financial market effects. Not much has changed in a week besides the rhetoric. Or at least that’s the case if you look at the four factors that I illustrated in a recent issue of Beyond the News.

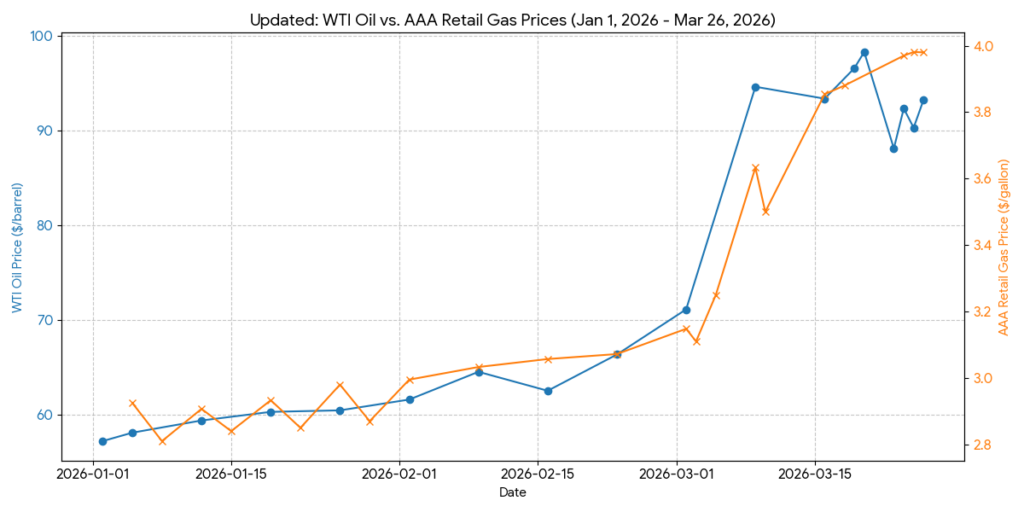

Oil is Elevated

Oil prices remain high. Importantly the small concession this week to suggestions that the war might wind down shortly did not move prices on downstream products. Gasoline is one of them, but there are others such as fertilizer and petroleum-based feedstocks that are not going to snap back just because oil prices drop a dollar or two. It’s not just that our perception of prices is strongly shaped by the drive-up price for gas. It’s also a reality. And it is the reason inflation forecasts have moved up.

Inflation is Expected to Rise

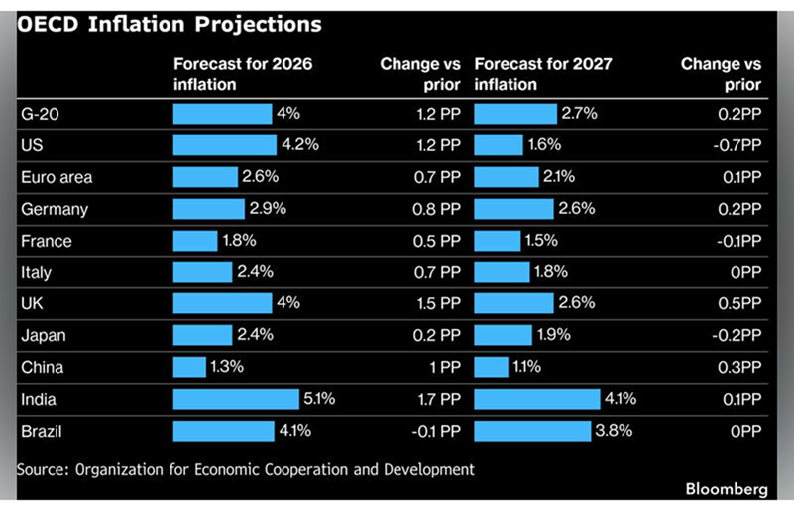

The Organization for Economic Cooperation and Development has raised its forecast for inflation this year to four percent for the developed countries and 4.2% for the U.S. This is bad news for those counting on the Federal Reserve to reduce short term rates. There are a few, in addition to, or perhaps on account of, Donald Trump. Steven Miran, who is Trump’s appointee to the Federal Reserve, recently said that the central bank should look beyond what he characterizes as transient inflation, and reduce rates. And Rick Rieder, Chief Investment Officer of global Income at BlackRock and someone Trump considered nominating to chair the Fed, made a similar point this week.

That’s not likely to happen. One of the ironies of the current situation is that the Fed, which has ben criticized as being too data dependent, and thus reactive rather than leading the direction of the U.S. economy, is likely to become even more data dependent.

Perhaps the day will come when central bankers, informed by the “perfect knowledge” of artificial intelligence, will be able to turn the dials just so to achieve a desired outcome rather than trying to steer the ship to respond to current conditions.

Perhaps the day will come when, as a small boat sailor, I would let the tiller and sails be set by a computer that reads wind, wave, and current sensors a quarter mile ahead. Call me old school but I wouldn’t try this without expecting to be doused when the boat capsizes.

Credit Remains Suspect

The problems in the private credit market remain. They’ve not pushed into the segment of the market that serves public funds investors—or at least not in a big way. Commercial paper spreads are wider by a bit and because of this prime local government investment pools are likely to widen their yield advantage over government funds by a few basis points.

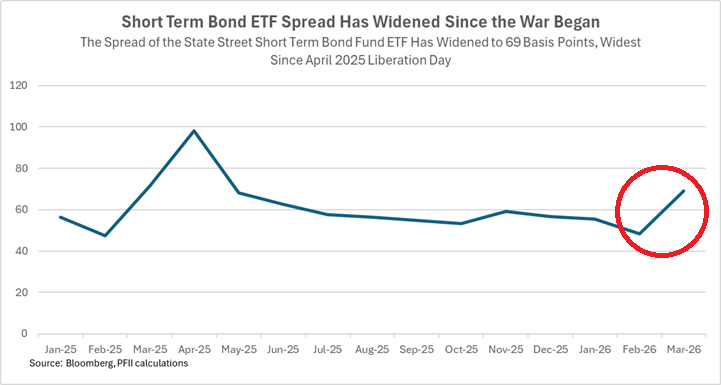

Short term corporate bond spreads also are wider. As a measure, the interest rate spread between a short-term corporate bond fund such as the one managed by State Street, and matched Treasuries, has widened out to 69 basis points from the level of 48.5 at the beginning of February. That’s not an indication of an imminent crash but rather a sign that investors are requiring more compensation, in the way of higher interest margins, to invest in investment grade credit.

The prospect for rising inflation, lower economic growth and greater uncertainty has had an identifiable effect on investment grade credit including the bonds that public funds investors may hold in their portfolios.

With this rise in spread expect that credit holdings will drag down portfolio returns when compared with those achievable by investing solely in Treasuries.

The Dollar is Firm

Demand for U.S. dollars has been solid. Despite, or maybe on account of, the war, the dollar is viewed as a haven. Not so much for other “safe” havens. Gold has lost about 13% of its value and Bitcoin is down about five percent since beginning of March.

The dollar had lost more than 10% of its value in 2025. The rebound is a (small) bit of good news when it comes to inflation because it limits the cost of imports.

Bond Investors are Bearish

The level on long maturity Treasuries is worrisome. It reflects political uncertainty, both domestically and abroad, and worries about the future course of fiscal policy. Congress and the President seem unable to keep the government open. The Trump Administration is likely to seek $200 billion to pay for the war. And there is cost of refunding tariffs declared illegal by the Supreme Court. The Penn Wharton Economic Model estimates this to be $182 billion. The Administration has not explained how it will pay for this nearly $400 billion in new costs, but the bond market suspects it will be by borrowing. That would increase the federal budget deficit by almost 25%. No wonder 10-year Treasuries are now yielding nearly 4.50% (and 30-year Treasuries are near five percent).

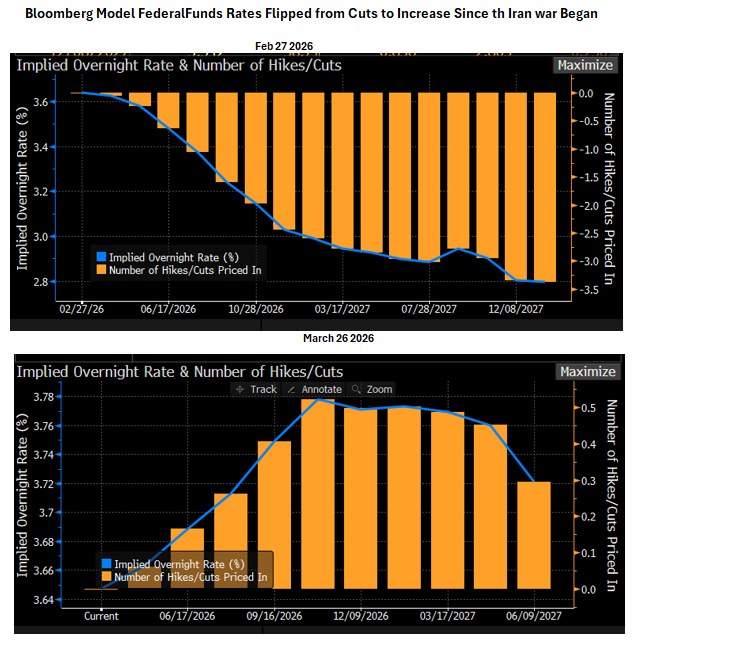

The Outlook for Fed Funds is Upside Down

There is no more graphic way to portray the outlook for short term rates than the charts below that display the results of factoring the federal funds futures and interest rate options markets for the future course of overnight rates. At the end of February investors were betting on a rate of three percent at the end of this year and 2.8% at the end of 2027. Turn that upside down and you have the current outlook: rates at year-end are projected to be higher, with about one in two chances that the central bank will raise rates by a quarter percent.

Bottom line

Public funds investment opportunities are closely tied to the level of federal funds. Where investors saw the possibility of multiple cuts this year, the new view is that the Fed will not cut and could actually raise rates by year-end. If something breaks—the job market crashes or the financial markets freeze—that could change, but with uncertainty high it may be better to keep your head down and stay under the turtle shell.