Solid Growth of Investment Assets in 2025 Helped Support State and Local Government Budgets

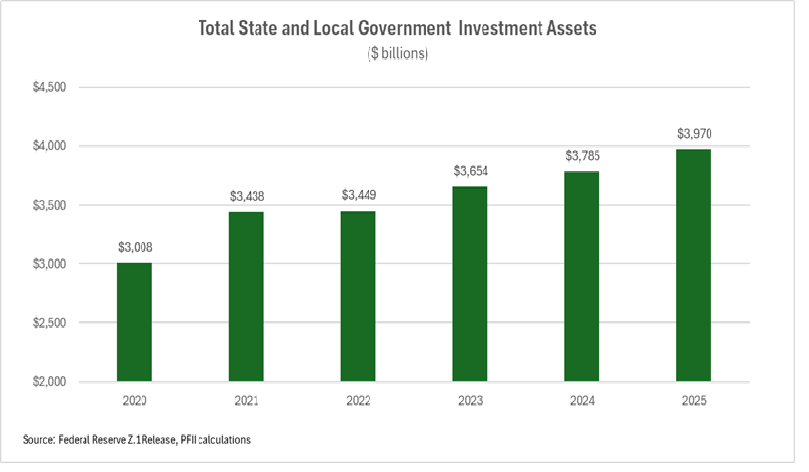

State and local government investment assets grew at a strong pace in 2025, extending a trend that goes back to the pre-covid era. Data released by the Federal Reserve last month showed investment assets ended last year at $4.05 trillion, up from $3.8 trillion in 2024.

State and local government investment assets grew at a strong pace in 2025, extending a trend that goes back to the pre-covid era. Data released by the Federal Reserve last month showed investment assets ended last year at $4.05 trillion, up from $3.8 trillion in 2024.

- The five percent growth rate was ahead of the growth rate of expenditures, allowing public units to add to fund reserves and budget stabilization funds.

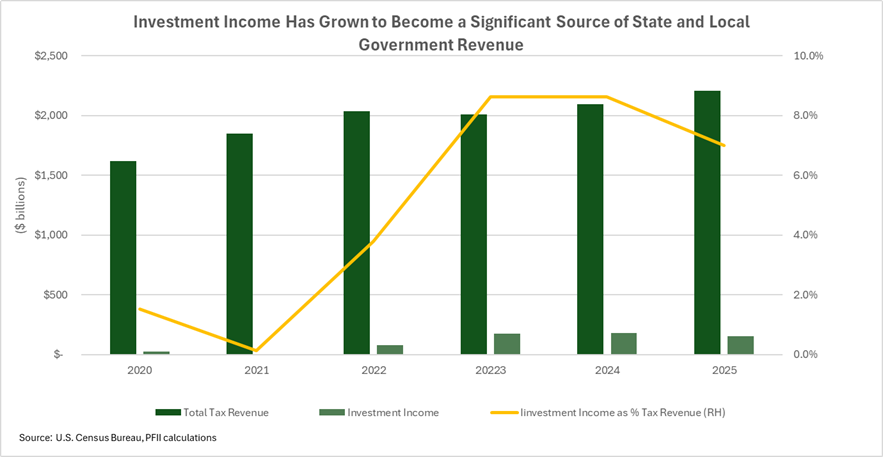

- The expansion benefitted from strong investment portfolio earnings. We estimate earnings were equal to about $150 billion of the increase. Portfolio balances also grew by about $50 billion as a result of additional accruals to fund balances.

- The five percent growth rate in total investment assets is consistent with the growth rate for local government investment pool assets rated by S&P Global. These pools totaled $409 billion at the end of the year, up five percent over the year.

- Earnings on investment assets represent a hefty share of tax revenue and provided a vital source of revenue for public units. Financial managers have come to rely on them to relieve pressure to raise taxes or cut spending. We estimate the earnings represented more than eight percent of tax receipts in 2023 and 2024 and seven percent last year.

- By contrast, in 2021, when short term rates were near zero, we estimate that investment earnings totaled only about $2.3 billion(!) for state and local governments, a small fraction of the annual totals in the 2023-2025 years.

- These results highlight the importance of planning around set-asides for rainy day funds or reserves and considering the sensitivity of multi-year budget strategies to investment-related interest rates. For example, a cut in short-term rates from the current level of about 3.60% to 2% could cut interest earnings by nearly 50%, costing states and localities $70 to $80 billion a year. For some public units, the effect could be on the order of five percent of tax revenue.

A Deeper Dive

To gain added perspective on the relative importance of investment earnings for states and localities we analyzed the financial statements of a sample of 23 states, municipalities, and school districts over the 2020-2025 period. The sample represented both affluent and poor areas of the country. We observed a number of things:

- The states in our sample had the highest growth rate of cash and investments of the 23. These assets more than doubled in the 2020-2024 period. (We used 2024 because 2025 data are not complete.) This is consistent with other research that concluded that states generally built up rainy day fund balances in the post-pandemic years.

- Budget decisions rather than economic and demographic factors appear to be the determinants of investment reserves. Overall, our sample of public units had investment balances equal to 61% of revenue in 2024. Several affluent municipalities had ratios close to the overall average; poorer localities in our sample had higher average balance ratios over the period, indicating that investment balances were more closely tied to budgeting than to economic capacity.

- Investment strategy and portfolio structure can have a notable effect on budgets. When rates rose sharply in 2022, a number of entities booked negative interest earnings. The accruals for these amounted to three percent or more of total revenue and as much as five percent of tax revenue for several of the sample entities.

- Likewise, the small decline in interest rates in 2024 and 2025 produced fair value adjustments that boosted reported annual income for those portfolios invested for longer duration.

- A decline in earnings (reported for financial statement purposes) when interest rates rise and a boost when they fall may complicate year-to-year spending decisions and communication with elected officials and taxpayers over year-to-year budgeting. This should be a consideration in investment strategy and portfolio positioning.

Looking Forward

Investment income has become a significant element in public unit budgeting. The $150 billion or so in earnings in each of the last several years, a product of strong investment balances and high interest rates, has been a welcome budget resource. A sharp drop in interest rates could leave a gap in budgets. Similarly, a plan to draw down balances to pay current expenses can leave a recurring revenue gap in the future. Financial managers should work hard to understand the effects of reserve management on their budget strategies and the interest rate risk that may be embedded in their plans.