Are LGIPs a Safe Harbor from Bond Market Volatility?

With financial news headlines screaming Treasury market volatility and commentators warning that the sharp rise in interest rates could cause dangerous market dislocations, one might wonder about the stability of money funds and LGIPs.

Are they a safe harbor? It appears at this point that they are not affected by the interest rate moves that appear in the headlines almost daily.

What has market observers practically screaming is the path of long-term interest rates.

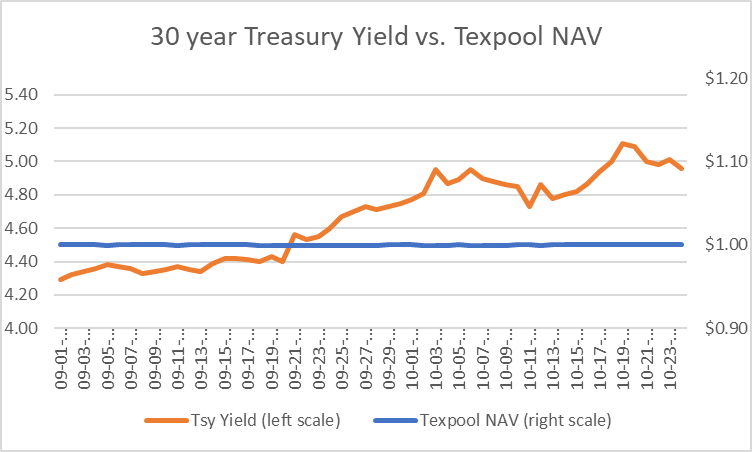

Here’s a chart of the recent yield history of the 30-year Treasury bond.

The yield moved from about 4.20% on September 1 to 5.10% a few days ago.

That’s a big deal. The rise of 30-year Treasury yields by nearly 90 basis points since September 1 has reduced the value of these bonds by about 14%. Yet stable net asset value funds, including money funds and LGIPs have barely moved.

Short term rates, which are reflected in the yields of LGIPs and money funds, are tied tightly to Federal Reserve monetary policy. Investors in long term bonds pay less attention to Fed monetary policy as they consider the long-term outlook for inflation, financial stability, the volume of future bond issuance and macro trends that could boost the demand for investment capital. Many of these factors support the “higher for longer” outlook for interest rates that now pervades the bond market.

Money funds publish their NAVs daily so investors can satisfy themselves on this matter. LGIPs generally are not transparent in this respect, but several follow the “gold standard” of disclosure for money funds. One of these is Texpool.

Just for chuckles here is a graph comparing the 30-year Treasury yield and the Texpool NAV:

Since September 1, the market value NAV of this $28 billion pool averaged .99986 and the low was .99983. It would be fair to say it was not affected by bond market volatility.

The Texpool Prime portfolio, which holds credit instruments, had the same NAV pattern. So did the North Carolina Capital Management Trust-Government Portfolio, an $18 billion LGIP and the Colotrust Plus and Prime portfolios. A number of other LGIPs do not publish this information.

I guess, if you’ve taken bond math 101, and certainly if you have a CFA, this exercise may seem silly, but I’m pretty sure there are not a few investors who may have wondered how headline bond market volatility has impacted their LGIP investments.

Money in Motion

At the short end of the yield curve the opportunity set for public funds investors is changing. Here are a couple of data points:

• The Federal Reserve’s direct repurchase agreement facility, which peaked at $2.6 trillion in early January, continues to fall. It is now down to $1.1 trillion and shrinking. Where did the money go? Assets of money funds are still near their highs and bank deposits have recovered from the small post-Silicon Valley Bank shrinkage.

• Debt outstanding of the FHL Banks has declined by nearly $300 billion as of September 30 from the May 2023 peak of $1.5 trillion. This, the largest GSE these days in terms of issuance, has been a major source of high-quality short-term investments for public funds investors.

• Commercial paper outstanding is up about $100 billion from the beginning of the year.

• Treasury Bills outstanding are up $1.5 trillion as the Treasury has expanded its borrowing to fund the Federal deficit.

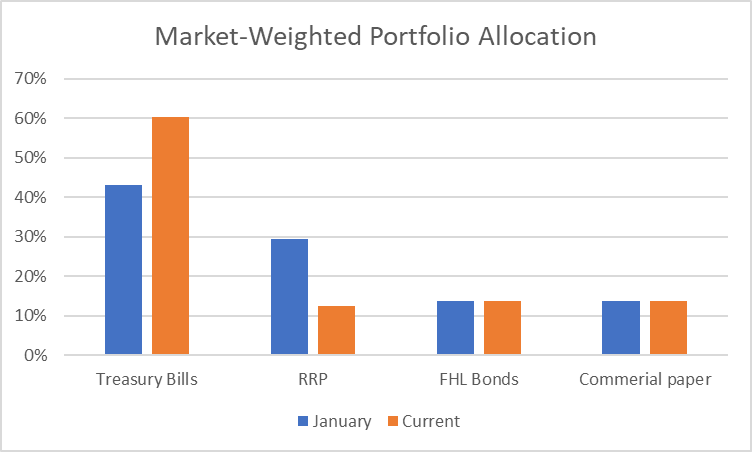

If you managed a short-term (one year or less) money market portfolio and sought to maintain market weightings in these four security types, the portfolio today should be about 60% invested in Treasuries (vs. 43% in January) and 13% in repurchase agreements (vs. 30% in repurchase agreements in January).

That would suit the Federal Reserve and Treasury just fine since the central bank is in the midst of reducing its Treasury holdings to reverse its Covid-related quantitative easing, and Treasury is laboring to finance near record budget deficits.

Market analysts generally expect these supply trends to carry through the fourth quarter and into 2024:

• Treasury supplies should increase.

• FHL Bank issuance should decline as commercial banks that tapped the FHL Bank advances after the bank funding crisis last spring repay these, replacing these liabilities with deposits.

• Commercial paper issuance should continue at current levels.

Meanwhile Treasury is considering how to ramp up issuance of Bills. It has asked the Treasury Borrowing Advisory Committee (an industry advisory group) to comment on the idea of adding a regular issuance of 42-day Bills to the calendar, along with the six other tenors that are on a regular schedule.

Note to self: It would be a good idea to brush up on T. Bill trading if you manage short-term funds.

Oklahoma’s New LGIP Law

Oklahoma Has a new LGIP law that eases the ability of cities, counties and related authorities to pool funds and expands the investment authority of LGIPs to include commercial paper and negotiable certificates of deposit.

The new law, HB 2538, will be effective November 1. It permits county and city treasurers to invest in “qualified pooled investment programs” (defined elsewhere in the statutes) as long as the investment is authorized in the local government’s written investment policy. This eases participation, which might otherwise require a specific act of the local government unit.

Qualified pooled investment programs are also freed from investment concentration restrictions that apply to commercial paper, negotiable certificates of deposit and bankers acceptances otherwise authorized for local government investment in Oklahoma.

School districts are not included in the new law. Schools participate in the Oklahoma Liquid Asset Pool which was organized in 1996. It is managed by PMA Asset Management LLC. and sponsored by various school associations. Its net assets totaled about $95 million as of June 30, 2023, and do not include credit instruments.