Beware the Ides of March

Yesterday’s Federal Open Market Committee meeting concluded with no change. Or did it? While the committee voted 11 to 1 to keep rates unchanged and released its quarterly Summary of Economic Projections with only modest tweaks, it also came at a time of a significant swing in market sentiment.

Yesterday’s Federal Open Market Committee meeting concluded with no change. Or did it? While the committee voted 11 to 1 to keep rates unchanged and released its quarterly Summary of Economic Projections with only modest tweaks, it also came at a time of a significant swing in market sentiment.

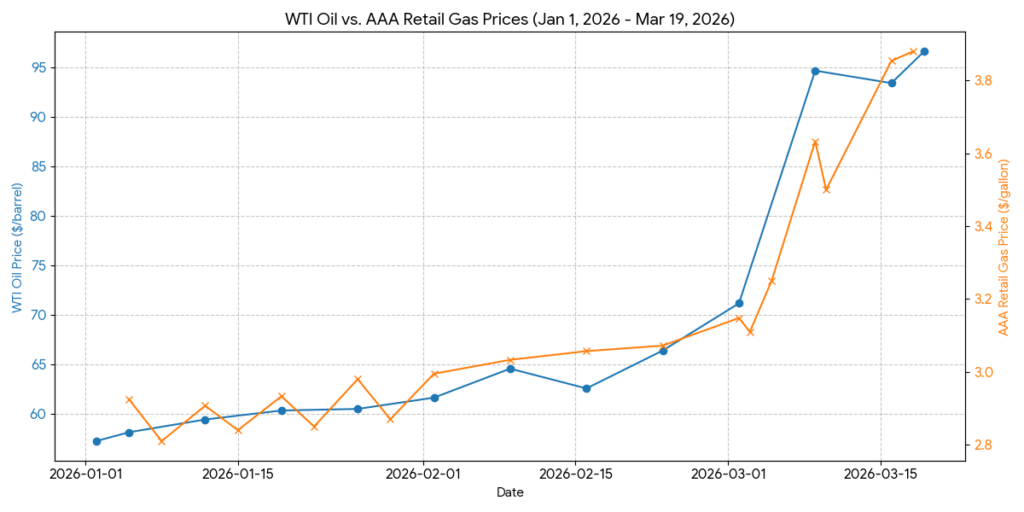

Point to oil. At this writing WTI oil is just below $100, up from $65 at the beginning of March, while the retail price of gas, everyone’s favorite personal indicator of inflation, was reported by AAA to be $3.88, up nearly $1 from a month ago.

Point to uncertainty that threatens to gnarl global supply lines and disrupt domestic production. Reorienting the U.S. economy to support a war will mean moving from butter to guns, as the economist Paul Samuelson described it, in short order. You can’t produce bombs and food in the same way, with the same emphasis and costs in peacetime vs. in a war economy.

Point to uncertainty around the two Fed mandates: managing price stability (inflation at two percent) and achieving maximum employment (4%-4.3%, based on the current Summary of Economic Projections).

Inflation was running closer to three percent before the surge in oil prices, and while there was much hope that it would fall to the Fed’s target later this year, underlying data suggested this might have been too optimistic. The personal consumption expenditures and producer price reports (for January and February respectively) are examples. Meanwhile labor market conditions have weakened, with recent data showing slow to no growth in new private sector jobs, weaker private hiring plans, and weaker wage growth.

And the stock market, which seems to be the Trump Administration’s favored economic health indicator, is down 4% to 5% year to date.

In the background, pushed from the front pages and chyrons by the Iran War, there is the private credit story and the uncertain future of the tariffs.

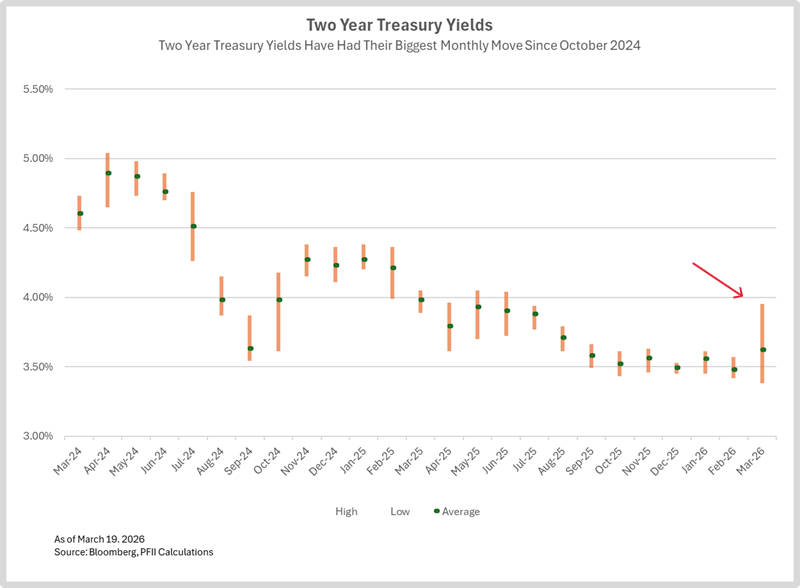

All of this has led to higher market volatility. Below is a model I use to track short term market volatility. Several weeks ago, I included this in a Beyond the News issue noting that volatility had receded to very low levels. Not now. The updated measure shows that two-year Treasury rates have ranged over 57 points this month.

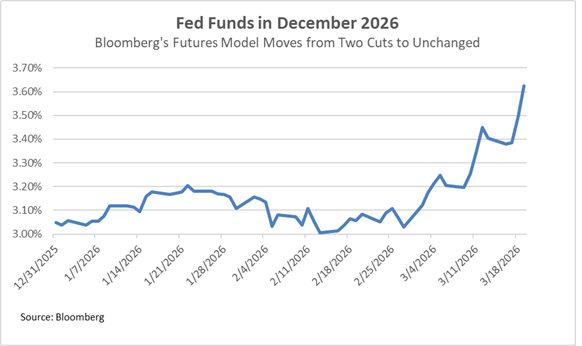

It also has led to a sharp revision in the forecast for federal funds, a key to the investment earnings outlook for many public funds investment portfolios, from 3% last month to 3.60% now.

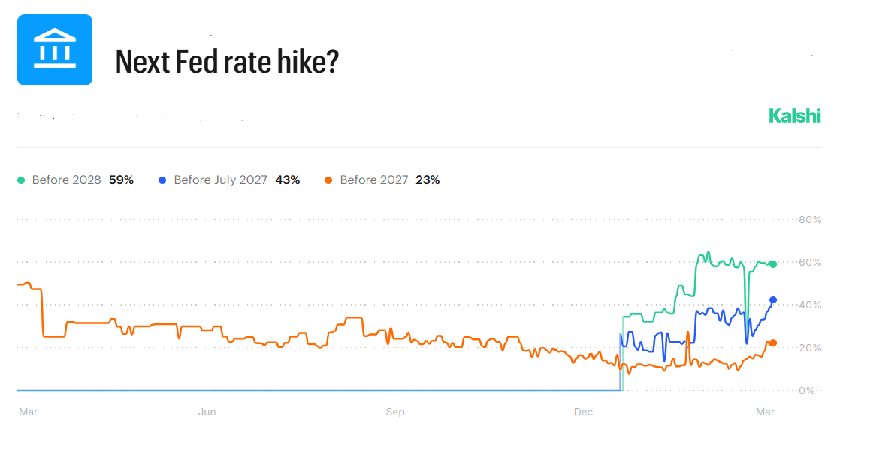

And talk of the next move in federal funds as being up is no longer just the whisper of a few outliers. A month ago, Adam Posen, president of the Peterson Institute for International Economics and former member of the Monetary Policy Committee of the Bank of England, rolled this out on a Bloomberg Odd Lots podcast but the view was largely ignored. However in the past several weeks bets that this would be the case have grown. In the unregulated betting market, there is now nearly a one in four chance that the Fed will hike rates before the beginning of 2027. (In fairness, this is a thin market with low volume, but still. . . . )

Bottom Line.

The (very recent) change in market sentiment is interesting (to some) but don’t bet your investment strategy on market calls. Rather, take the change as another reason why staking investment plans on a market outlook is risky. To win, you have to be able to call ups and downs on a consistent basis, to time moves into and out of long or short positions. There are a few billionaire hedge fund managers who can do this successfully (though in truth many more hedge funds are successful because they are able to process information and act more quickly than the rest of us and/or rely on leverage). But for the rest of us, whose mandate does not include taking risks, the market move should be taken as a sign of caution.