Fair Weather: Public Funds Investors Are Well-Positioned to Meet Investment Expectations

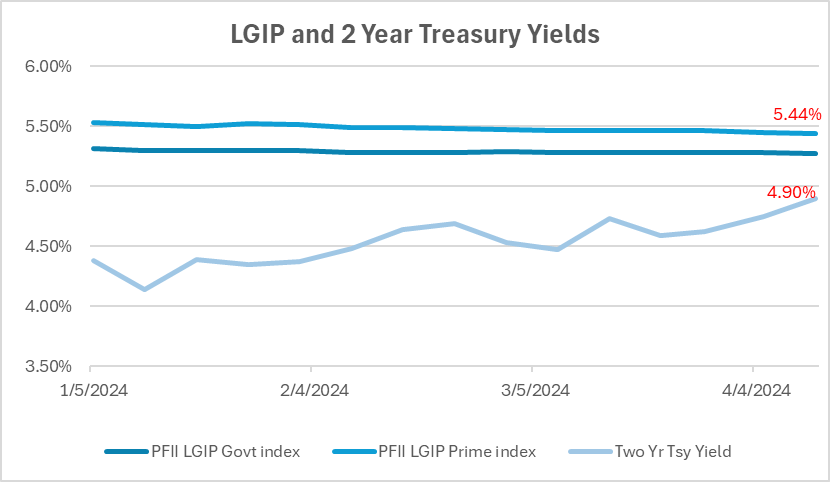

The accompanying chart of recent moves in yields speaks volumes about the current market environment and its implications for public funds investors.

Since the year began short-term money market rates have been at or near their generation highs. And they have barely noticed the big moves in market sentiment. LGIP rates, as measured by the Public Funds Investment Institute’s Prime LGIP Index ended last week at 5.44%, nine basis points below the 2024 high levels. (See the updated Investment Dashboard here.)

Not so for rates further out the yield curve. The two-year Treasury yield has risen by 75 basis points since early January and is now within reach of 5%. Why? market economists in January encouraged investors to act on the (mistaken) belief that the Federal Reserve would begin by early spring to cut rates aggressively. This pushed up the prices for securities like the two-year Treasury note as a way to lock in yields—anything higher than 4% was deemed a bargain. Investors in the short-maturity segment of the market might think of this as rate insurance.

Meanwhile the underlying economic conditions persist: solid economic growth, strong job creation, rising real income, rising stock prices and inflation that is persistently below the Fed’s 2% goal but much less threatening than it was a year ago when it was 6% or in the spring of 2022 when it was at 8.5%.

This is all good news for public agency investment programs—especially for those that are cash-rich. Investment earnings forecasts completed before the start of the year are likely to be exceeded by the persistence (or rise) in short-term rates.

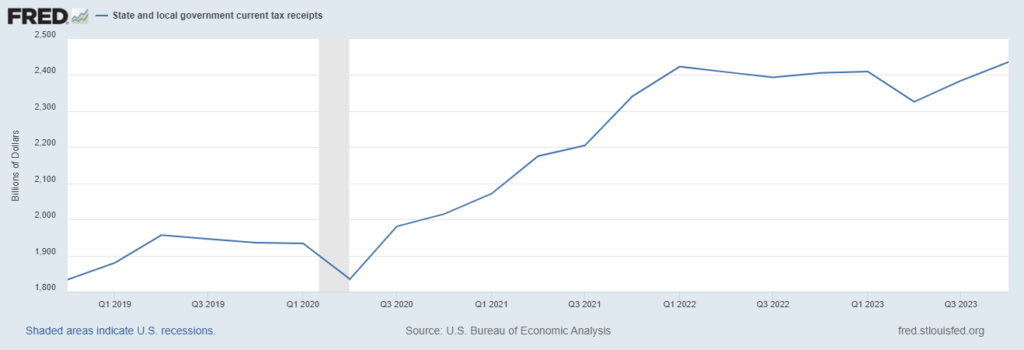

Meanwhile state and local government tax and revenue collections continue to support stable investment balances. The following chart may not immediately point to this conclusion—the year over year growth in state and local government tax receipts is only 1.3%.

But this period included tax cuts by many states—analysis by the National Association of State Budget Officers concluded that they amounted to 1.1% of revenue—and a slowing of GDP growth in the first quarter of 2023 to less than 1%. In the second half of 2023 revenue receipts grew at an annual rate of 9.5%.

And as we reported last month state and local government investment assets expanded by7.5% in 2023.

For all the angst over the state of the economy and longer-term trends in state and local government financial resources—which could be drawn down as COVID relief funds are spent down—at least in the short run things are positive.

The Squeeze: Money Market Reforms Will Alter the Commercial Paper Market

We reported in February that money market reform would change the institutional prime money market business with implications for public funds investors who invest in commercial paper and other short team credit instruments. Last week Bank of America analysts published a report with their take on this. Their conclusion: institutional prime funds closing because of the reforms would cause yield spreads to widen between short-term Treasuries and commercial paper, boosting commercial paper yields by four to eight basis points.

This would be a modest benefit to public funds investors. But the closures also have implications for the depth and stability of the short-term markets; it will take time to see how this plays out.

The details. By October institutional prime money market funds will have to implement a liquidity fee regime mandated by the Securities and Exchange Commission. Two large fund with more than $200 billion in assets, and that are offered privately, have announced they will close and convert to government funds to avoid the fee regime. Other funds could follow suit. These two funds, and a third smaller fund that announced it is closing, represent about 34% of the $660 billion intuitional prime universe. They also represent 16% of the combined institutional and prime fund assets. Over the next six months, the institutional fund space could shrink by half or more.

Prime money market funds are large and (usually) steady buyers of commercial paper. If this source of demand shrinks, relative rates should rise to entice others into the market. Bank of America estimates the “cost” will be the aforesaid four to eight basis points.

There is another dimension to this: reduced size could reduce market depth and secondary market liquidity for commercial paper, making it harder and more expensive to sell these securities prior to maturity.

On the other hand, the SEC and other market regulators seem to believe that institutional prime funds contain “hot” money that is quick to flee the market in times of stress, and the behavior of these funds exacerbated the market disruptions around the Covid lockdowns in the spring of 2020.

If that is the case, their exit will not be a true loss for remaining market participants who could experience a smaller, but more stable secondary market and modestly higher rates to boot.