Illinois LGIP Could Open a Pool for Non-Profits

Illinois by Nick Youngson CC BY-SA 3.0 Pix4free

The Illinois Treasurer is seeking authority to create a local government investment pool for non-profit organizations. Senate Bill 3157 (and an identical bill in the House) would authorize a Non-Profit Investment Pool to operate in a manner similar to the Illinois Public Treasurer’s Pool (Illinois Funds), the $19 billion state-sponsored LGIP.

A background memo in support of the legislation notes that the proposed fund would be “identical” to the Illinois Funds pool which operates like a Securities and Exchange Commission Rule 2a-7 money fund, although it is not registered as a mutual fund under Federal securities laws.

According to the memo the pool would “fill a gap for medium sized non-profit organizations and would provide an investment option for hundreds of Illinois organizations.”

LGIPs have generally not sought investors other than government entities, but there are at least two that are focused on the non-profit market. The Pennsylvania Invest Community Fund is managed by the Pennsylvania State Treasurer as a component of the state’s Invest Program. It had 176 shareholders that are non-profit organizations and about $80 million in assets as of December 31, 2023. It operates as a stable net asset value fund. The Invest Program also offers a daily pool to local governments with $1.3 billion of assets and 261 local government shareholders.

The Massachusetts Development Finance Agency sponsors the STAR Fund, managed by PFM Asset Management LLC. It is offered to non-profit institutions within the state that are exempt from Federal income tax and is designed for the investment of bond proceeds. It operates as a stable net asset value fund and also offers borrowers an individual portfolio option. It had about $195 million in assets as of December 31, 2023.

The opportunity for LGIPs to expand their markets to include non-profits may be based on two elements:

• Regulatory flexibility (or, as some might characterize it, regulatory arbitrage). Unlike money funds, which are bound by the ever-tightening Rule 2a-7 requirements, LGIPs operate with some flexibility. For example, institutional prime money funds are prevented from offering shares at a stable net asset value; their shares must float based on the underlying value of portfolio holdings. Later this year institutional prime funds will be required to impose liquidity fees when daily redemptions exceed 5% of a fund’s net assets and all money funds will be required to maintain a larger portion of their assets in liquid investments.

LGIPs are not required to follow these limits, and it doesn’t seem as if they will volunteer, so investors, including potentially non-profit or other organizations, would be free from them. Whether funds that do not have these requirements are riskier remains to be seen, but flexibility to tailor requirements to the needs of one’s investors could be an advantage to LGIPs that want to expand their business.

• Investment costs. State-treasurer sponsored LGIPs generally operate at much lower costs than institutional money market funds. The Illinois Funds has an expense ratio of 5.5 basis points, while the Invest Program operates at a cost of 11 basis points. Cranedata reports that institutional money funds generally charge 15-20 basis points (though some share classes with minimum balance requirements of $10 million or more charge about 10 basis points). Lower fees may translate into higher net yields for investors.

Bottom line: LGIPs will have to be careful that expanding their business into these segments doesn’t run afoul of state laws or trigger loss of exemption from registration under the Federal securities laws. “Grassroots” LGIPs that rely on intergovernmental cooperation authority may be challenged in this respect, while initiatives by state treasurers or other state agencies could offer the best means to accomplish this.

Cash Remains on Top

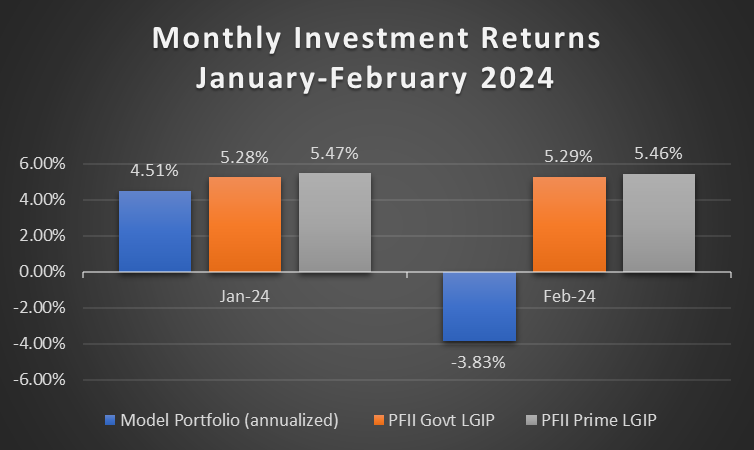

Cash is king again so far this year. Two months of bond market volatility—and realization that the Federal Reserve is not on the cusp of reducing its main policy rate—depressed returns for most fixed income strategies so far in 2024, putting LGIP and money fund returns in the lead. (See the Investment Dashboard for details.)

The PFII model portfolio, which represents an investment strategy commonly employed by public funds investment managers, is invested in ETFs that contain Treasury and investment grade corporate bonds with maturities of three years or less. This portfolio had a miserable February, with a return of -0.31% for the month (annualized to a loss of 3.83%) as bond yields—measured by the performance of the two year Treasury Note—rose nearly 0.50% in the first two months. The annualized year-to-date return of the model portfolio was 1.59%. Longer-maturity separate accounts had even lower returns. Compare this with LGIP and money fund returns of between 5.25% and 5.50% for the two month period. So far, cash is the place to be.

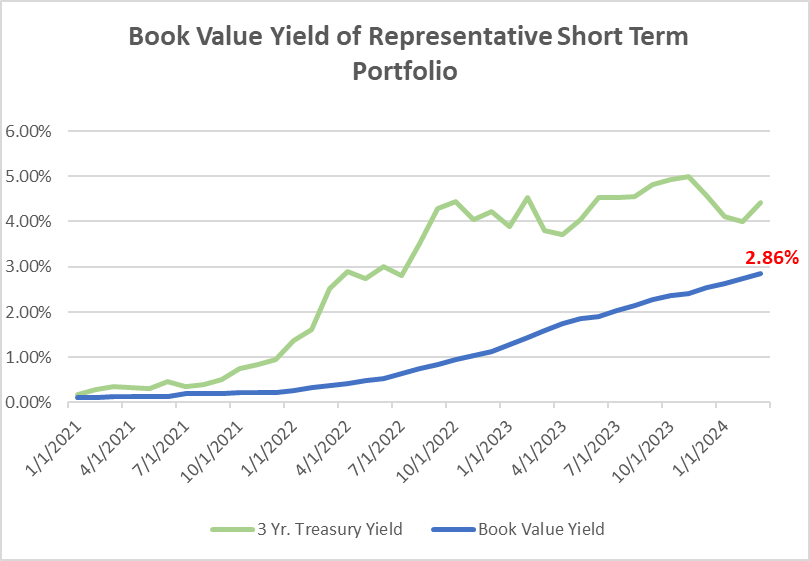

While total return is a good measure of investment performance, it does not necessarily represent the contribution that public funds portfolios make to an organization’s budget. For those who keep score using book value accounting, the conclusion is similar: these portfolios are lagging the cash market. The below chart shows the monthly book value yield of a portfolio with maturities laddered evenly over a three year period.

We modeled the results from this portfolio beginning on January 1, 2021. In the simulation, each month the maturity was re-invested at the then-current three year Treasury yield. As expected the book value yield lags the current market rate. At the end of last month the book value yield was 2.86%. To be fair, when rates do fall the longer-maturity portfolio will maintain its yield and could out-perform cash. But for now. . . .