Iran and Interest Rates

What impact will the Iran war have on short-term markets? The headlines have been all about oil prices. They are up, and that’s important, but it is not the whole story.

What impact will the Iran war have on short-term markets? The headlines have been all about oil prices. They are up, and that’s important, but it is not the whole story.

• Oil prices will affect inflation, though the effect is not straightforward.

• The biggest impact on the markets is that the war heightens political and economic uncertainty. We’re already in the throes of a period of elevated uncertainty and fighting in the Middle East has raised the level.

• Uncertainty is likely to delay Federal Reserve moves to cut interest rates. There is also an outside possibility that the next Fed move will be to boost rates.

• Let’s just say that short-term rates are in a holding pattern until the sky clears.

Oil Prices

This is the obvious lead for any discussion of the effect of the war on the economy and markets. The initial spike in oil prices was sharp but contained. At this writing oil is up about 16% percent from last week. Perhaps prices will go higher, particularly if Iran inflicts major damage to production by the Gulf States or is able to restrict shipping through the Gulf of Hormuz. Some fear $100 plus oil, but this may be a bit exaggerated at this point.

Dependence on foreign petroleum is muted in the U.S. because we’re net exporters of petroleum so domestic production can absorb some of the shock that might occur to supply. This is far different than it was during past events that disrupted Middle East oil production/flow in the 1970s and 1990.

Fuel is only about three percent of the Consumer Price Index, so its direct effect is modest. It’s also a part of the cost of most other goods and services that we purchase. (Transportation accounts for about 6.5% of gross domestic product.) Nevertheless, U.S. consumers felt the rise in prices for oil and gas almost immediately. You don’t need a Bloomberg terminal to chart this. Drive by your local gas station and you’ll likely see prices are higher by 30-40 cents this week.

A longer view is that prices have been rising for several months as have tensions in the Middle East. The increase since mid-December has been about 40%,more than double this week’s move. When we think about the impact of oil prices on the overall economy and, importantly, on consumer spending and sentiment, it’s the longer view that may matter.

Inflation

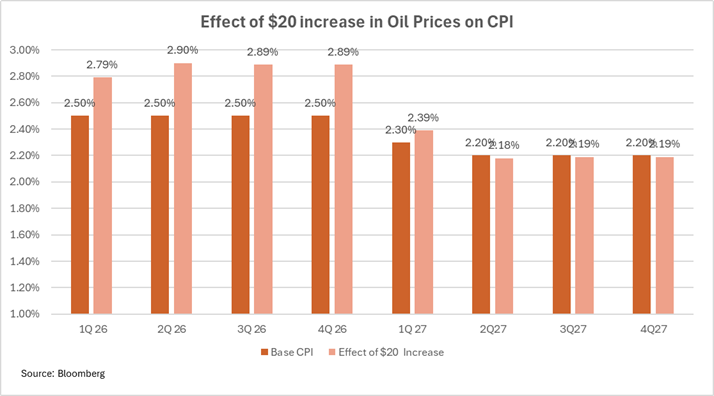

Oil prices factor into inflation but the relationship is not one- to-one. The direct impact on consumer prices, as measured by the Bureau of Labor Statistics, is limited. Using a macro model provided by Bloomberg we calculated that a $20 increase in oil prices would boost CPI by about 0.40% for several quarters (say from 2.80% to 3.20% on an annual basis) as it diffuses through the economy. The graphic below shows the timing and magnitude of a $20 increase over the next two years. The effect is somewhat proportional to the increase so a $40 increase would elevate CPI by about .80%.

Inflation would elevate but over time the economy will adjust, and inflation would return to its trend.

Americans, already sour on the pace of inflation, will not be pleased by this, but it’s unlikely to trigger a breakout and a sharp rise in interest rates.

Fiscal Stimulus

It seems inhumane to suggest that the war will lead to an increase in government spending and fiscal stimulus, but that is the case. It feels like $50 to $100 billion is the starting place for a spending increase that will be proposed by the Trump administration. That’s a big number until you consider the overall size of the federal budget: $7 trillion.

Whatever spending is approved will affect the budget deficit and Treasury borrowing in coming months. Spending could produce a modest boost to GDP; the Bloomberg model we use estimates a $100 billion expenditure could raise real GDP by about .03% (that is, from say 2.3% to 2.33%) over each of the next several quarters.

The government will also have to issue more Treasuries to pay for this. When added to the unfunded requirement to refund tariffs collected under the Trump tariff plan, it means Treasury may have to issue $200-$300 billion more in the next year than currently expected. Issuance is likely to be concentrated in Treasury bills where the Treasury has signaled it plans to increase borrowing to fund the $1.6 trillion (or perhaps $1.9 trillion with tariff and war spending) it will need.

The short term markets have been resilient as supply has increased, and there is always the Fed standing ready to purchase in the name of market stability. So Increased supply might push up short term yields by a few basis points, but the effect will be modest.

The Fed

Which brings us to the Fed. The driver of investment returns for most public funds investors is monetary policy. Local government investment pools which contain about one in four dollars of state and local government investment assets have yields that closely align with federal funds. Investment opportunities in bank deposits, short-term high-quality credit instruments and short-term Treasuries also align, though not as closely.

The Fed is likely to tread carefully until the impact of the war on the U.S. economy becomes known. The war (and uncertainty around tariffs following the Supreme Court ruling invalidating Trump Liberation Day tariff plan) are likely to further complicate, and retard, Fed moves. Trump has made it clear he wants lower short-term rates NOW; it’s somewhat ironic perhaps that the war will provide further justification to those who have argued otherwise.

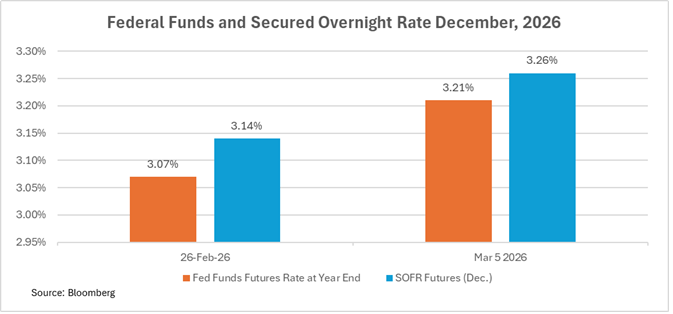

The futures market has adjusted to reflect this new outlook, with both federal funds futures and an index of repurchase agreement rates now suggesting a higher year-end rate than they implied a week ago.

Polymarket handicaps a 32% chance that federal funds will be unchanged at 3.50% at year end, and a 35% chance that the Fed will cut once (to 3.25. (Yes, it’s come to that. We’re looking at the betting markets to provide insight into investment opportunities.)

Then there is the possibility that the Fed’s next move might be to raise rates. A month ago, a small minority of monetary economists were forecasting this based on an outlook for sticky inflation and solid economic growth in 2026. Their position, while still in a minority, has a bit more behind it today than it was a month ago. Meanwhile Polymarket ascribes a 17% chance for a rate hike by the end of the year.

Bottom line

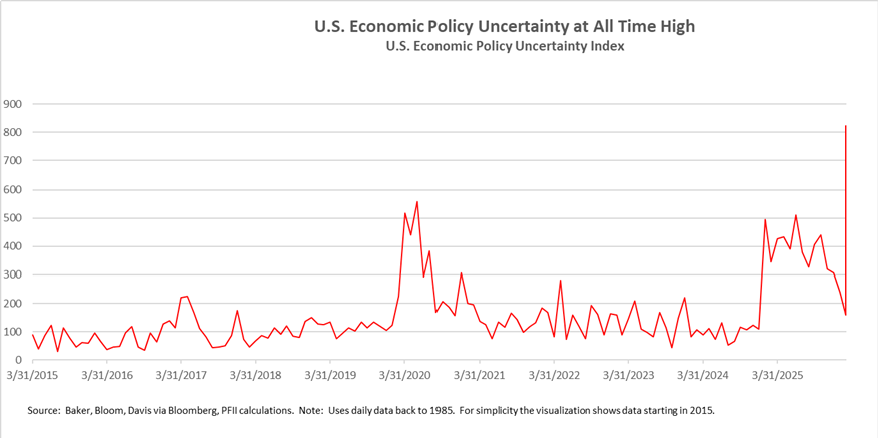

Uncertainty is high on all fronts. The measures used by market commentators and many investors are VIX, a measure of stock market volatility, and MOVE a measure of volatility in the fixed income markets. They are not particularly elevated. But a more comprehensive measure of political and economic uncertainty, the Economic Policy Uncertainty Index, is showing the highest level in its 40 plus years of history.

This is consistent with polling that indicates Americans are sour on the economy, even though current data are not bad, and that they are very concerned about the direction of the country. The war is not the cause of this, but it surely reinforces the outlook.