Is It Time to Go Long?

With all the talk of higher interest rates, unexpected strength in the US economy and an unsettled political situation here and globally, is now the time to go long? For the past two years cash-like investments (especially stable value LGIPs) have been the winners as rising interest rates produced losses in bond portfolios, but at some point the tide will change. For public funds investors, where “long” means two- or three-year maturities now may be that time.

`

Consider these factors:

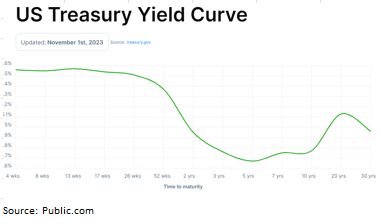

Interest rates. They have risen at an historic pace, from near zero at the beginning of 2022 to 5-6% today. The main driver has been the Federal Reserve’s monetary policy. The Federal Open Market Committee has signaled for several months now that its progressive tightening program is at or near its end point unless inflation accelerates. Moreover, the recent moves in rates have been in longer-maturities, which may be a signal of the long-term outlook but are not a central factor for short-term portfolios.

Inflation. The rapid rise in inflation in the first half of last year is what spurred the Fed to act. Inflation unmistakably has slowed from the 8% plus level in mid-2022 to the current pace. Most measures have it in the range of 3.5-4% and though this is above the Fed’s goal of 2%, things are moving (slowly) toward the goal.

The labor market. The job market is strong—so strong that some fear it will ignite inflation again. But the connection between labor market strength and broad economic price pressures is not certain. Indeed a recent Federal Reserve research paper concluded that rapid wage growth was not an important driver of post-pandemic inflation.

Re-pricing the cost of capital. Expanding Federal budget deficits, changes in savings patterns related to the aging US population and a new emphasis on investment to power GDP growth are forces that push up the cost of capital through higher interest rates. This could be a potent force in maintaining “higher for longer” rates but it is likely to be most impactful on long-term rates.

Investing is not without risk. Lengthening portfolio maturities subjects a portfolio to increased interest rate risk if rates rise. But maintaining a portfolio in cash-like investments has risk as well, because if rates decline the income stream from the portfolio will drop quickly. High quality risk-free government bonds currently yield around 5%, the highest rate in nearly 20 years, and for those public agencies with reserves this can be a very meaningful source of revenue that could be “locked-in” for several years.

But but. . .When considering risk, note the following:

Recession. If the economy slips into recession or the financial markets seize up, rates associated with high-quality short-term securities (e.g., Treasuries that mature in less than 3 years) are more likely to move lower than higher. This would reduce income from reinvestment of maturities but also raise the value of high-quality securities in this maturity range.

Time is your friend. If you hold a two-year bond today and rates are higher tomorrow by 1.00% you stand to lose about 1.8%. But if the rise in rates—or the point at which you have to mark to market—is a year from now the unrealized loss would be reduced to .9% by the passage of time. Meanwhile, the two-year bond, if it is a Treasury, would earn about 5% and it would earn another 5% the following year, as the unrealized market value loss gradually diminishes to zero at maturity. (Note as well that accounting principles applicable to public agencies generally do not require that unrealized changes in the value of a security be recognized as a revenue item.)

What if you are not completely confident of liquidity requirements? Can you justify locking in an attractive income stream for several years by buying an investment that is highly liquid but has a somewhat longer maturity? This is not without risk but let’s look at the numbers. Say that cash flow analysis indicates you have a surplus to invest for the next 12 months. After that, you are not certain but there is a good chance you would not need the surplus for at least another 12 months. If you buy a two-year Treasury at five percent today, and you have to sell it in 15 months for a cash need, here is the math: If rates are unchanged, you would sell it at 5.40% (the yield curve in this segment of the market is inverted). You would realize a loss of about .75%, but you would have earned income of 6.25% (1/14 years at 5%). The income minus the loss would result in an annualized holding period return of 4.40%*. If rates at the time of sale were 7.40% the sale price would be about 1.75% below cost and the holding period return would be an annualized rate of 3.60%*.

One more caveat: The examples here are based on Treasury rates because these securities are highly liquid and without risk. Investment grade corporate obligations would generate more income (about 6% for 2-3 years) but are subject to heightened default risk if the economy turns south and can quickly become illiquid if the financial markets seize up.

Bottom line: cash has been the winner for the past two years but may not be for the next round. What was right yesterday may not be tomorrow.

___________

* Simple math, not compounded or time weighted.

Treasury Supply: Good News, Bad News

Treasury’s announcement Wednesday of its borrowing plans for the rest of 2023 and early 2024 surprised market participants who had expected to see a big jump in supply. Instead, the Department forecast a more modest increase in the supply of notes and bonds and “modest reductions” through January in Bill auctions.

Public agencies are big buyers of Treasury securities. The most recent Federal Reserve estimate of financial assets estimated that state and local governments held 44% of their financial assets in Treasuries at the end of June. That is about $1.6 trillion worth. These holdings are largely in maturities of less than three years.

So let’s focus on Bills and short maturity notes. Bill supply expanded rapidly so far this year, with the total outstanding growing by $1.8 trillion to $5.3 trillion on September 30. This was a boon to public agencies. Prior to Wednesday’s announcement, the Treasury suggested that it might increase issuance even more by regular issuance of 42-day Bills. This would suit those who manage stable value LGIPs, money funds and short-term public agencies just fine, since increased supply should push up the interest rate on these high quality very liquid securities. More supply would provide an alternative to Federal agency debt and the Federal Reserve’s reverse repurchase agreement facility, both of which are shrinking.

Wednesday’s announcement deferred a decision on regular issuance of the new Bill tenor. Instead, the Treasury expects to implement “modest reductions to short -dated bill auction sizes. . . through mid to late January.” After that Bill issuance is likely to increase because of seasonal factors.

Treasury expects to issue $17 billion more in two ands three-year notes through January. This would represent an increase of about 17% from recent auction levels and it would probably result in a small concession (aka somewhat higher rate) to do so. For accounts that buy and hold, the value is likely to be in the secondary market rather than new issue notes.