LGIP Trends: Higher Yields, Plateauing Assets, a Bit More Risk

Moderating asset growth, higher yields, and a move to a somewhat less defensive market risk position sum up local government investment pool fundamentals in the second quarter.

Let’s look at the numbers: :LGIP assets grew modestly, and yields rose apace with rising short-term interest rates according to tracking reports recently published by FitchRatings and S&P Global.

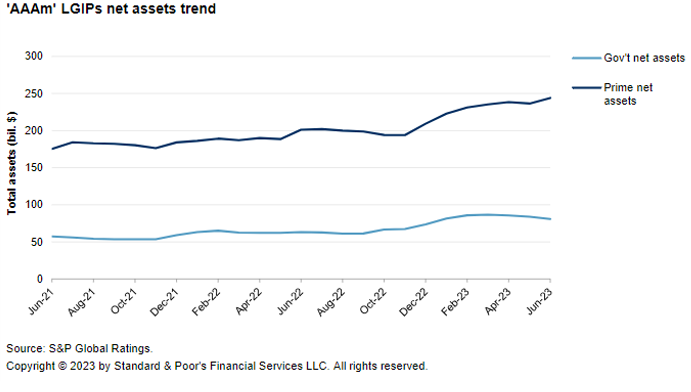

Fitch reported growth in liquidity pools (those that offer a stable net asset value) of 2.2% in the quarter. This was lower than the 5.9% quarterly growth rate Fitch observed in the prior three years. S&P reported assets in stable net asset pools that it rates were up 0.9% in the quarter. Assets in prime pools in the S&P universe were up 3.8% while government pools lost 6.9%.

By comparison, assets of money funds regulated by the Securities and Exchange Commission (SEC) grew by 4.0% or $226 million in the quarter with government funds seeing most of the inflow.

The following chart from S&P illustrates the trend of moderating LGIP asset growth after a post-COVID-19 period of strength.

Several factors are behind the trend in LGIP assets:

- The sharp rise in short-term rates beginning 18 months ago encouraged investors to pay more attention to reducing uninvested balances. With pool rates now above 5%, $10 million invested will earn $500,000 a year today vs. barely $20,000 at 2021 rates.

- The inflow of COVID-19 relief funds boosted state and local government financial assets in 2021. The flow is now reversed, with state and local governments required to spend Federal relief funds by 2026.

- The growth of state and local government tax revenue, which responds to the overfall pace of economic growth. Gross domestic product (before adjusting for inflation) expanded at a rate of 9.4% from 2021 to 2022. It has grown by about 5% in the first half of this year.

- The level of bank deposits, which are the main alternative to LGIP investments for many governments. Deposits grew strongly beginning in 2020–from $13.7 trillion to $18.1 trillion in May 2022 when they peaked. They have since declined modestly to the current level of $17.3 trillion.

To sum it up LGIP asset trends could weaken modestly in coming quarters as local government spending accelerates and banks compete vigorously to attract and hold deposits.

Good news on the yield front. LGIP yields topped 5% at quarter-end for the first time in nearly 20 years. Interest earnings are now a meaningful contributor to state and local government revenues, especially for those entities that have significant investment balances.

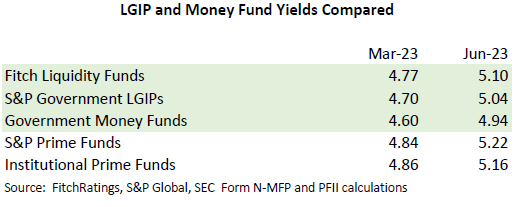

Fitch reported that the average yield of liquidity funds it tracks as of June 30 was 5.10%, up 33 basis points in the quarter. S&P reported similar results for its rated LGIP universe. Its index of yields on government LGIPs was 5.04% in June, up 34 basis points in the quarter. Its yield on prime LGIPs was 5.22%, up 38 basis points.

The yield advantage for prime over government LGIPs in the S&P universe increased in the quarter by 4 basis points as fund managers extended maturities to invest in credit-backed instruments.

Net yields of SEC-regulated money funds rose by a comparable 34 basis points for government funds and 30 basis points for institutional prime funds.

The increase in yields in LGIPs and SEC-regulated funds tracked closely the rise in the Federal Reserve’s policy rate, which rose 25 basis points to 5.25% in the quarter.

We have incomplete information on the market risk for LGIPS. Government LGIPs tracked by S&P ended the quarter with an average maturity (“WAM”) of 24 days, a level matched by SEC-regulated government money funds. Prime LGIPs tracked by S&P had average WAMs of 36 days as of June. This was up from 30 days in March. The SEC reported WAMs for institutional prime funds of 23 days in June. It appears that managers of institutional prime funds were far more defensive than those of prime LGIPs.

A second measure of market risk—how much a fund maintains in liquid securities—is not uniformly disclosed by LGIPs. SEC-regulated institutional prime funds reported 51% invested in daily liquid assets and government funds reported 80%. Only a few LGIPs disclose this information so broad comparisons are not available but from spotty information available it appears that LGIPs maintain less liquidity than their SEC-regulated counterparts.

Another measure of market risk is exposure to credit instruments (commercial paper, negotiable CDs, and other credit obligations). Prime LGIPs tracked by S&P had 58% of their assets invested in credit instruments at quarter-end. Institutional prime funds had lower aggregate credit risk as of June with 52% of their portfolios in credit instruments.

The bottom line. The universe of LGIPs tracked by the rating agencies performed in line with the larger universe of SEC-regulated money market funds. Average yields of LGIPs in the reported universe were somewhat higher than those of all SEC-regulated money funds, but how much of this is due to investment results and how much to fees we do not know because we have no uniform information on LGIP fees. The market risk of LGIPs seems to be broadly in line with that of SEC-regulated funds, but here an important missing link is information on LGIP liquidity.