LGIPs Shun New Money Fund Liquidity Rule: What it Means for the Industry

The big picture. A requirement that raises the liquidity threshold for money market funds under the Securities and Exchange Commission’s Rule 2a-7 is effective in early April. Local government investment pools are exempt from the rule and those that advertise they are “Rule 2a-7 like” have given no sign that they will follow this new requirement.

This puts further distance between the operations of regulated money market funds and LGIPs. It should improve the competitive position of some LGIPs vs. their money fund analogues, but also changes their liquidity risk profile when compared with regulated funds and puts greater burden on boards and management to control risk.

The details. The SEC adopted a new round of money market reform in July 2023, responding to the Covid-19 related financial market volatility that impacted the money fund industry in the spring of 2020. One significant change will require that all money funds maintain at least 25% of their assets in daily liquid securities and 50% in weekly liquid securities. This requirement, which raises the minimums from 10% and 30% currently, is aimed at further buffering liquidity to meet investor redemptions in times of stress.

Many LGIPs that seek to maintain a stable value advertise that they operate in a manner that is consistent with Rule 2a 7 but that does not mean they conform with all the limits of the rule. Complying with the SEC’s original liquidity minimums, put into place in 2016, was a point of departure for some LGIPs who shunned the 10%/30% requirement while others adopted it. But it does not appear that any LGIPs, other than those which are registered with the SEC, will adopt the new, higher standard.

Why it matters. Money funds were at the center of the publicity about volatility that swept the financial markets in March 2023, though whether they were a cause or merely an expression of the volatility is not clear. What we know is that the Covid-related crisis drained liquidity from the short-term money markets and that investors in prime money market funds sought to redeem shares, leading to fears that these funds would run short of liquidity. This fueled selling by the funds that further fueled the market instability. A similar pattern played out following the Lehman bankruptcy in 2008.

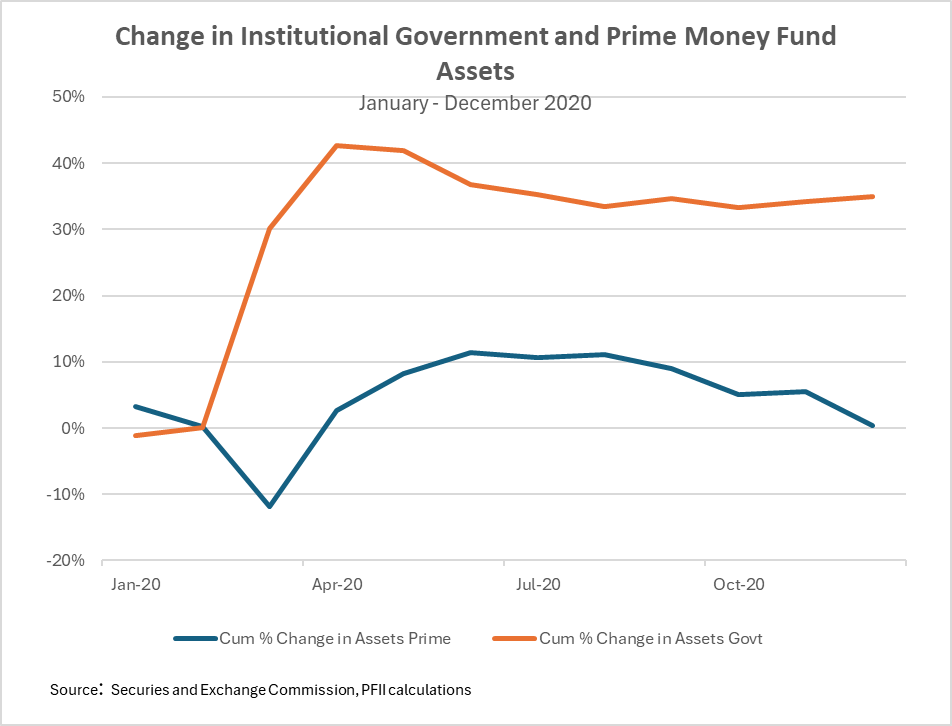

The chart above, from an Investment Company Institute analysis of the impact of Covid-19 on the operation of money market funds, illustrates the fund flows. In both 2008 and 2020 sudden drawdowns of assets panicked the markets. In response to the 2008 crisis the SEC mandated that funds maintain 10% daily/30% weekly liquidity; the 2020 drawdowns suggested this was not enough.

In fact, the drawdowns in 2020 were quite modest in amount. SEC data show that prime funds lost about $76 billion in assets in March 2020. This represented 12% of prime assets. In the same period assets of government money market funds surged $839 billion. (Note the Investment Company Institute study, which showed a larger loss for prime funds, tracked only those that are publicly offered. Gains in privately offered institutional prime funds offset some of the losses in this period.)

Are LGIPs Different? Managers of LGIPs note that their funds did not experience market-driven outflows in March 2020. While we do not have data on all LGIPs to explore this—there is no uniform reporting or transparency for LGIPs—the fund flows for the group of prime LGIPs rated AAA and AA by S&P Global show a drawdown of $6 billion or 4% in assets from peak to low point in the spring of 2020.

One explanation for the difference in money fund vs. LGIP investor behavior is that LGIP investors have no alternative to their state-specific fund (other than a bank deposit vehicle). While institutional money fund investors can easily switch assets to government funds in times of stress—and seem to have made this move in the spring of 2020—for the most part LGIP investors do not have this option, as few LGIPs offer both government and prime stable value funds.

One LGIP that offers both is Texpool. Its comprehensive website disclosures show its prime portfolio declined from about $8 billion in early March 2020 to $6.95 billion on April 1, an outflow of about 19%. Its government portfolio gained $4.5 billion to $28 billion in this period.

Another possible explanation is that LGIPs are “closer to home” as it were, and their investors have more confidence in them. In this sense they are less a commodity than institutional money funds and their investors are more likely to rely on them without question.

Without any easy alternative, and with greater familiarity/confidence in their LGIP investment vehicle, state and local government investors may be inclined to “ride it out.”

Finally, some state sponsored LGIPs have a large base of non-voluntary participants that provide stability and can buffer individual participant actions. The California Local Agency Investment Fund is the standout example, where the state and state-related entities accounted for more than 75% of its assets in 2020. These investors would/could not withdraw funds, so any liquidity demands by others were buffered.

The competitive landscape. In many respects we’re already in the post-April period where the new rule applies so the new rule may not change the relative performance of money funds and LGIPs.

The performance of government money market funds and government oriented LGIPs is not likely to change because of the new liquidity requirements. This is because the SEC rule counts as liquid direct obligations of the United States regardless of maturity. So managers of these funds should need to alter their strategies on account of the new liquidity requirements.

Institutional prime money market funds have been operating for at least the past year in a manner that is consistent with the 25%/50% liquidity standard. The following chart shows that institutional prime funds (red dashes) more than met the 50% weekly requirement in the period before the new rule was adopted. So no changes are needed in the management of institutional prime funds to meet the 25%/50% liquidity requirement.

For them, the requirements are mostly a matter of formalizing recent practice rather than adapting to new constraints.

Institutional prime LGIPs as a class likely do not meet the new 25%/50% liquidity thresholds–though absence of uniform reporting makes this conclusion somewhat speculative. They could continue to operate without the higher liquidity minimums constraining them.

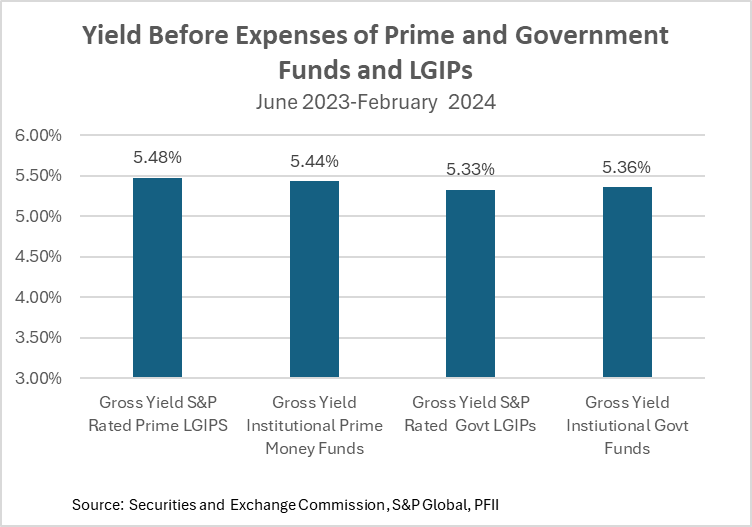

The following chart compares the gross (before fees) yield on institutional prime money funds and prime LGIPs for the prior since June, 2023.

Individual manager styles may produce differences that are more or less than the averages shown, but we might look at these differences as the cost of complying with the SEC’s new liquidity requirement. Prime LGIPs out-performed government LGIPs by 15 basis points in this period. But they out-performed institutional prime money funds—which already appear to be in compliance with the new liquidity rule—by only four basis points. (The difference shown in the chart between prime and government funds is likely attributable to the use of credit in prime funds and LGIPs and, in the case of government funds, the fact that money funds have access to the Federal Reserve’s reverse repurchase facility.)

Why not conform to the new SEC Liquidity Rule? As previously noted, LGIPs will likely be in compliance with the 25/50% liquidity requirement whether or not they formally incorporate the requirement into their investment policies. This is because the SEC rule counts direct obligations of the United States regardless of maturity as being liquid. As of the beginning of March, government-oriented LGIPs rated by S&P had about 88% of their assets in government securities—the vast majority in Treasuries.

Some fund manager representatives and some board members, seeking guidance or perspective on the matter of liquidity standards, have looked to the Government Accounting Standards Board (GASB) or the rating agencies.

GASB Statement 79, adopted in 2015, included the SEC’s 10%/30% liquidity limits. But GASB Statement 79 eliminated its ties to Rule 2a-7 and GASB has not revised its standard to adopt the SEC’s new requirements.

The rating agencies have a similar focus on principal stability and not on liquidity. S&P has commented that “We have opted not to establish minimum daily and weekly liquidity metrics as part of our … criteria because we assess funds management’s approach to maintaining adequate liquidity given their unique shareholder needs.”

FitchRatings has a 10%/30% requirement for its AAA LGIP designation and has indicated it is unlikely to change this.

Although a liquidity event could overtake an individual LGIP, there is the view that the “local” nature of these funds and their relatively small size within the larger financial markets universe would limit contagion or destabilize the financial system. In total, stable value LGIPs are only 10-15% of the size of money market funds (whose assets are now about $6.5 trillion). That is not to say that a problem involving an LGIP would not be serios for its investors, but prudential regulators would not see it as a threat.

That said, LGIPs are not immune from market forces. In the spring of 2020, the freeze in financial markets made it nearly impossible for LGIPs to create liquidity by selling securities. Minimum liquidity requirements are designed to protect against these possibilities even if they have low probability of happening because if a fund were unable to honor sudden liquidity demands by its investors the damage to the local investor community and to the LGIP industry could be immense.

The bottom line. LGIPs do not have a regulator to set common standards for operations. Rather, the details of operating are left to the discretion of the treasurer or board who is the fiduciary. This may be seen as providing flexibility, but it also increases the burden on the fiduciary to “get it right” when it comes to operating rules like minimum liquidity. A regulatory requirement can be viewed as a “best practice” in case something goes awry. Without this safe harbor there is a greater responsibility put on management—whether that is the sponsor, the board or the company that manages a pool.