The Surge in Bond Yields—Big Deal or Not?

The recent surge in long term yields may signal a big change in the outlook for the US and global economies.

Normally moves in long-term interest rates are not center stage for portfolio managers who manage cash pools, money market funds and short-term portfolios. But this is different, as it may signal shifts in the factors that are behind the usual focus on Federal Reserve policy, the latest jobs report and the outlook for inflation over the next year or two.

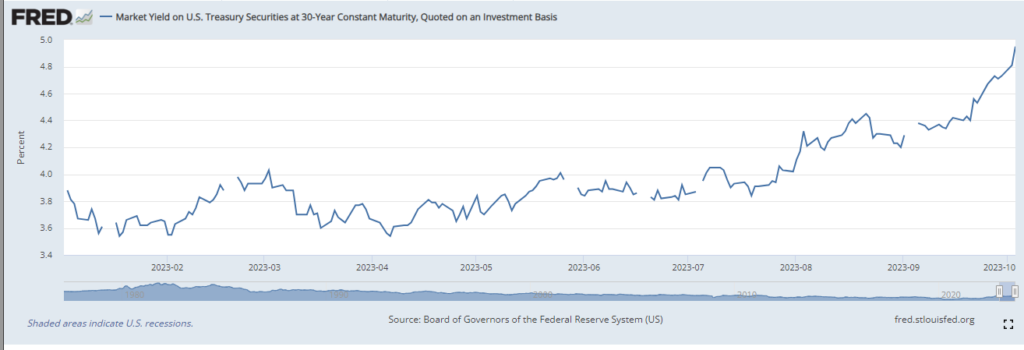

In the past two months the 30-year Treasury yield has risen by about 80 basis points. (It is up 90 basis points this year, as the following chart shows.)

A move of this magnitude over two months is not so unusual for short term yields.The two-year Treasury note, the bell weather for many short-term portfolio managers, gained 90 basis points in a short period this spring. But the move in long term rates is another story. The move in the 30-year bond yield, not just in the last month, but since the Covid-19 recession in 2020 is remarkable, and the economic impact on a long-term investor is real. If you bought the long Treasury at the low point in rates in February 2020 (or marked your holdings to market then) you would have suffered a loss of nearly 57% of its value. The same holds true for long-term corporate bonds, fixed rate mortgages and other instruments whose value is tied, either directly or generally, to the level of long-term Treasury yields. The level of losses embedded in the financial assets of the US economy is huge!

So, let’s unpack this by sorting through the possible causes.

Federal reserve monetary policy headlines focus on the Federal Funds rate, currently set at 5.25%-5.50, up from 0%-.25% in early 2022. Until July long term Treasury rates traced only part of this increase, rising from roughly 2.25% in March, 2022 to 4% this July. Most economists see the Fed nearly done raising rates and the Fed’s policy makers have generally promoted the idea that their job is nearly done—for now. The Fed’s own quarterly economic projections released September 20 had the median forecast for Federal funds at 5.25% next year and 3.75% in 2025. If long term rates resisted the Fed’s aggressive tightening and if indeed the tightening is nearly ended, why the recent surge?

Higher for longer. This is the second element of current Fed speak: The central bank may be nearly done with raising rates but will keep them high for an extended period of time. Some market commentators think it’s not just longer, but higher is in the cards, with JP Morgan’s Jamie Dimon making headlines early this week when he warned that the Fed would have to raise rates to 7%. OK, maybe higher for longer is here, but if the mid-term outlook for rates is bearish why are shorter-term Treasuries largely lower than the overnight money market rate? Two-year Treasury rates are around 5.55% and the five-year rate is under 5%.

Inflation. Like a lot of things these days the inflation outlook has a political element to it, but the numbers generally suggest that the outlook for inflation has improved. The Fed’s goal of returning the economy to an inflation rate of 2% may or may not be realistic, but recent prints of a host of inflation measures suggest that it is now in the range of 3.7% to 4%–a big improvement over the 6%-7% rate a year ago. Inflation is very much on the minds of American consumers but the Atlanta Fed’s business inflation outlook index in September was for a level of 2.5% over the next year and 2.9% over the next five to 10 years. The New York Fed’s inflation survey in August put consumer inflation expectations over the next five years at 3.6% and the University of Michigan consumer sentiment survey put long run consumer expectations at 3.0%. This challenges the likelihood that the Fed will achieve a 2% goal, but is the goal so far from realization that something drastic may happen that will lead to a sharp rise in inflation pressures?

Supply. Treasury borrowing needs are large and growing. Maybe Washington will be successful in stemming the rate of growth but it’s not likely that increased borrowing by Uncle Sam will end any time soon. At the same time the Fed is gradually liquidating its portfolio of Treasury and agency mortgage-backed securities. In the past year balances have declined from $8.5 trillion to $7.3 trillion. This reversal of quantitative easing will likely go on for another year until it too ends with the Fed still holding a large portfolio of assets. Borrowing has a cost, and for those consumers who have discretionary income higher bond rates are an incentive to shift some income from consumption to saving/investing.

Recession. Talk of a recession later this year or early in 2024 has recently increased and the stock market, seemingly in response to this chatter and to weaker equity earnings, has given up about 7% of its 2023 gains since the highs in July. (It is still ahead by nearly 12% since the start of the year.) But the below chart shows that rises in long term yields are not closely correlated with economic downturns with one exception: The deep recession of 1981-82 and related period of economic stagflation. So perhaps the talk of a mild recession is a bit Polyannish.

Financial stress. The bank crisis of the spring, problems in the commercial mortgage market, and/or political dysfunction in Washington could elevate financial stress and depress the value of bonds. The Treasury’s Office of Financial Research seeks to track the level of financial stress (see the below chart). With the caveat that this is, perhaps, an imperfect science, stress is not notably high. That said, there is always the risk that something will break. (When was the last time you found a black swan?) Perhaps the high yield on long-term Treasuries reflects, in part, this risk.

So, what’s up? Sometimes the answer is not immediately apparent. But the point is that the sharp rise in long-term yields is real. It suggests that the 15-year trend of very low interest rates, including two periods (2010-2015 and 2020-2021) when cash earned nearly zero, is now history. And it reminds that complacency is the enemy of portfolio managers.