What Treasury’s Borrowing Plans Mean for State and Local Government Investors

A shortage of short-term Treasuries? Perhaps not, but after a rapid expansion of issuance that dominated the market in the past two years, three developments could make it feel like there aren’t enough short-term Treasuries to go around.

Why it matters. State and local governments rely on Treasuries as the foundation for their portfolios, with public units holding $1.6 trillion of Treasury Bills, notes, and bonds at the end of 2023, in the aggregate the largest component of public sector investment portfolios. So, these developments could set the tone for the market for the rest of the year and into 2025:

- Supply. After rapid growth in the supply of Treasury bills (debt that is issued for 12 months or less) and short-term notes (we’re considering debt issued for two to five years), issuance should moderate for the rest of 2024 then decline modestly in 2025. This could mean modestly lower yields vs. other alternatives.

- The growth of government money market funds. They are the largest buyers of short term Treasuries and have increased their share of the market in recent years. Their appetite is likely to grow further as money market reform leads to the conversion of institutional prime funds to government funds. This too should keep downward pressure on short-term Treasury yields.

- The Fed’s monetary policy. Recent actions by the Federal Reserve to slow the pace at which it is reversing its quantitative easing will reduce the need for Treasury to issue debt to the public and improve market liquidity. Meanwhile reductions in the Fed’s reverse repurchase agreement program are pushing money funds to buy more short-term Treasuries. These too will put downward pressure on Treasury yields.

- tab

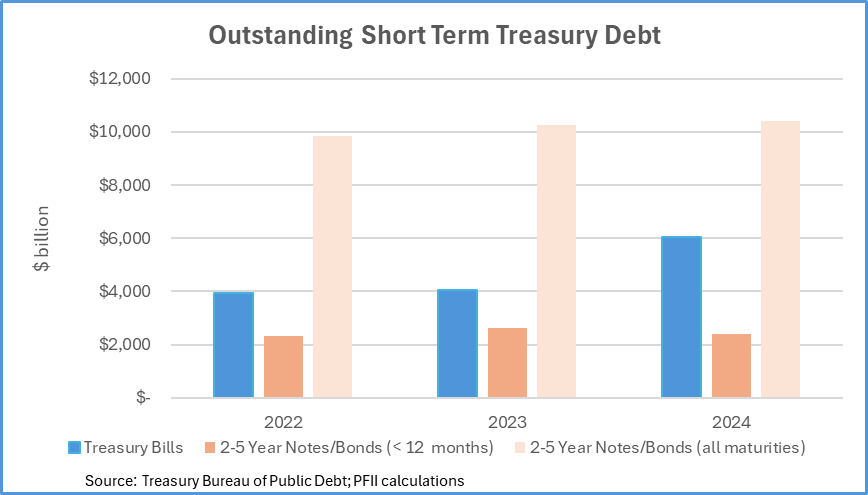

The details. Treasuries have been a buyer’s dream of late with a huge increase in supply of Treasury Bills. Outstandings increased from $3.9 trillion two years ago to $6.1 trillion as of April 30.

Net issuance of Bills through the first half of the fiscal year has been $846 billion. [Caution: these are VERY large numbers, but keep in mind that the total of Treasury debt that is publicly outstanding was $27.5 trillion at the end of March!] The increase in Bill supply in particular has been a boon to buyers who focus on short-term high quality liquid investments. There is also outstanding about $2.4 trillion of notes and bonds that mature within 12 months. They offer yields that are comparable to those of Bills, but are somewhat less liquid.

As part of its recent quarterly refunding announcement, Treasury forecasts its overall borrowing needs for the next two quarters will be much lower than in comparable periods over the last two years. As the following chart shows, Treasury plans for net borrowing of $243 billion this fiscal quarter and $847 billion next quarter. These are much lower in total than borrowing over the past two years.

On a net basis its Bill issuance will be close to zero for the remainder of the fiscal year: down by about $300 billion this quarter but up by an equal amount in the July-September period. And Bloomberg economists forecast that in the next year Treasury will increase its issuance by about $200 billion—much below the growth so far this year of $651 billion.

The forecast—an increase of slightly more than 3% in outstandings—is about the same as the expected increase in U.S. financial assets. So don’t expect supply to pressure rates higher in coming months as it did at times over the past year.

The demand for short-term Treasuries is robust. Money market funds are collectively the largest holders of short-term debt, and government money market funds, which hold only government debt, are somewhat insensitive to price, since their only realistic alternative is repo. Their assets grew by $459 billion in the 12 months ending March 2024, fueling demand for short-term Treasuries.

Recent growth is likely to continue, in part through the conversion of institutional prime money market funds to government funds to avoid new liquidity fees that will affect these prime funds when they go into effect later this year. The institutional prime segment currently totals about $650 billion and managers of about 30% of the assets have already moved to convert or shut down their funds.

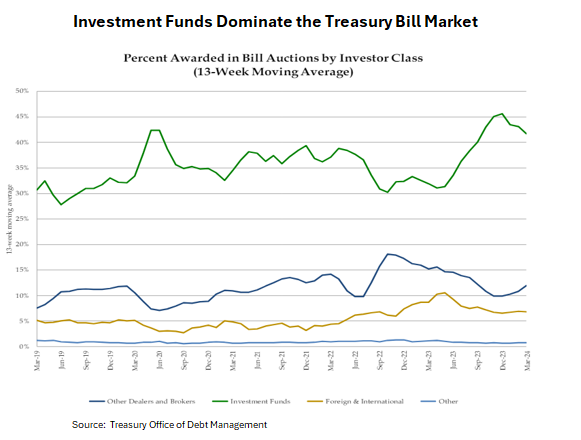

Treasury data show that funds—likely government money funds—already buy about 40% of new issue Bills directly, up from 30% two years ago.

Expect the demand from these funds to increase in coming months.

The Fed’s quantitative easing policy is an important factor in the Treasury’s debt issuance plans. Remember that the Fed holds about $4.5 trillion of Treasury debt, a balance built up as part of the central bank’s quantitative easing policy to buy open market debt to support the economy through the Covid-related recession. Treasury has begun to unwind this program, and the balance is down from a peak of $5.7 trillion in mid-2022. In May the Federal Open Market Committee announced it would slow the run-off of its open market Treasury portfolio to $25 billion a month. The Fed publishes this graphic of its Treasury holdings:

This will lead to Treasury issuing more securities to the Fed to replace some of those that mature, and it will reduce the Treasuriy’s need to issue debt to the public. Analysts forecast that the May decision to slow will reduce the need for Treasury to borrow from the public by $400 to $450 billion over the next two years.

The Fed’s reverse repurchase agreement facility also impacts the short-term Treasury market. The central bank activated this program in early 2021. Money funds are by far the largest users, and at the peak they had $2.2 trillion parked at the Fed.

As use has declined, government money market funds replaced their repo balances with short term Treasuries, adding to demand. There is further room for this program to decline toward zero.

The bottom line. Don’t expect that short-term Treasuries will suddenly become a scarce commodity. But the strong wave of issuance that has dominated the markets for the past two years is likely behind us—for now. There will be plenty of Treasuries to go around, but demand will be high and yields could be a bit lower when compared to other market measures. Will Treasury Bills soon yield two percent when the central bank’s policy rate is above five percent? Of course not, but investors whose investment policies limit them to government obligations may feel a pinch as they compete with other “price insensitive” buyers—particularly the Fed and government money funds—in this space.