When the Tail Wags the Dog: A Word of Caution Related to Investing in CP and CDs

Commercial paper and negotiable certificates of deposit make up a minor portion of the universe of short-term securities held by public agencies, money market funds and other institutional investors. But because the market for CP/CDs has suffered from disruption during periods of market stress, it has the continued focus of prudential regulators. This is highlighted by a recent report of the Financial Stability Board (FSB) on the vulnerability of the CP/CD market and should serve as a caution for investors.

• The good news: A well-diversified portfolio of CP/CDs should not add notable principal risk to a portfolio. High grade commercial paper has an excellent credit track record and investors can expect to receive a dollar at maturity (plus interest, of course) for every dollar invested.

• Liquidity is another matter. Ordinarily liquidity is available to sell CP/CDs prior to maturity and this liquidity supports active management of CP/CDs by permitting swaps, both between issuers and to extend maturities. But as we learned in 2008 and again in 2020, liquidity can disappear suddenly in a stressed market, leaving no ability to cash out CP/CD holdings prior to maturity. If you expect to sell CP/CD holdings to meet cash needs or fund liquidity requirements you could end up in a bad place.

• Another yellow caution flag: The 2023 money fund reforms imposed new a liquidity requirement on prime money market funds. It becomes effective later this year and the $650 billion institutional prime segment of the industry has already seen managers of more than $200 billion announce they plan to close or convert their funds. Some analysts think as much as 70% of the assets in this product may move in coming months. This will reduce demand, and at least temporarily, result in greater uncertainty around prices and liquidity for CP and CDs.

• Limiting exposure to very strong credits and carefully diversifying counter-party credits can be successful in managing credit risk. Avoiding the possible need to liquidate holdings prior to maturity—especially in stress situations such as a financial crisis or natural disaster—can limit liquidity risk.

The details. The FSB is not a well-known organization but is an important source of insight into the concerns of financial regulators globally. While it has no legal authority as a regulatory authority its membership, including from the United States Michael Barr, vice chair of the Federal Reserve for Supervision and Gary Gensler, chair of the Securities and Exchange Commission, illustrates its importance as a leader in developing regulatory policies across jurisdictions. It has, for example, been a leader in thinking about money market risks which has preceded several rounds of money fund industry reforms (notably 2014 and 2023.)

The $4.7 trillion global US dollar denominated CP/CD market is dominated by the United States. Domestically outstandings are about $1.2 trillion of CP and $2 trillion of negotiable CDs. ($800 billion of CDs are short term, with the balance maturing out to five years.) In the US, prime money funds are the largest buyers/holders of CP/CDs, but State and local governments hold a significant portion of these securities as well.

We estimate public units hold $290 billion of CP and $103 billion of negotiable short-term CDs. This compares with $756 billion of these securities in prime money funds. The combined total represents 57% of the outstandings in the short-term market, evidence that the market is dominated by a small number of like-motivated investors. (The overall short-term market, which is dominated by Treasuries, totals about $20 trillion.)

The CP/CD market is normally reasonably efficient. Most volume is driven by investors who are direct buyers of offerings by the major issuers—a group that is dominated by the major global banks. This is different than the market before the 2008 global financial crisis when nonfinancial corporations were more prominent issuers and dealers were more involved in the placement of these securities.

The good news around these changes is that buyers interact directly with issuers, so they save on brokerage costs. The concentration of issuance in a smaller group of systemically important financial institutions probably makes failure less likely (“too big to fail” is denied by the regulators but in reality, size means that an issuer’s stability will be protected.)

The bad news, as the FSB report highlighted, is that the market structure means liquidity is vulnerable in times of stress. Bypassing intermediary brokers and dealing directly with issuers has discouraged the operation of a secondary market to facilitate sales, including sales prior to maturity. The concentration of investors around a small group of large money fund sponsors means the market is dominated by institutions subject similar market and investor forces. When these investors step back from the market to shore up their liquidity there is no one to step in. And the absence of robust information on trading prices and flows means that opportunistic buyers are loath to participate.

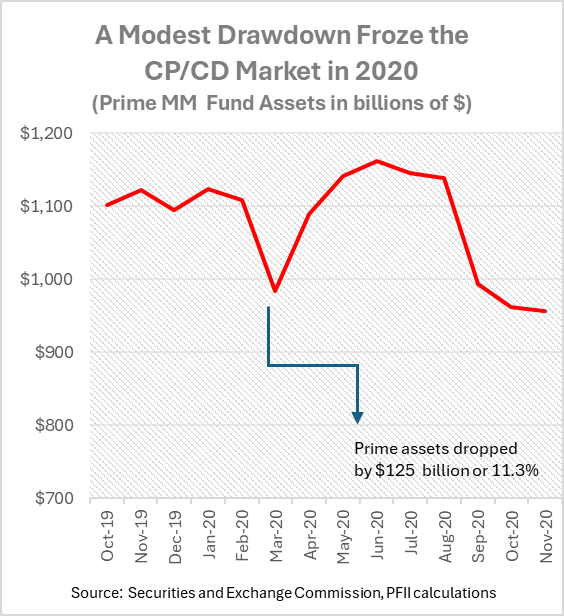

All of this means that even small disruptions in the normal pattern of buying can freeze the markets. There is no better demonstration of this than the market events of 2020 where money fund redemptions that totaled roughly $125 billion in March caused what was then nearly a $20 trillion short term money market to freeze. The outflows were not large in the overall scheme of things, representing about 11% of prime money fund holdings and only about three percent of overall money fund assets. That market activity—selling securities that represented at most a few percent of the short-term market—can be so disruptive is a warning/wake-up call.

What to do? There is a straightforward way to protect against liquidity risk: Don’t count on selling CP/CD holdings to meet cash flow requirements. Matching holdings of these securities with cash flow needs means that an investor need not count on liquidity. In the LGIP world, managers/trustees should consider what limits to apply to overall holdings of CP/ CDs. Where LGIPs have minimum standards for liquidity and conduct stress tests to maintain these limits, it is prudent to avoid relying on sales of CP/CDs to meet possible outflows. The way to avoid losing liquidity in these instruments is simply not to count on them for cash prior to their maturity.