Why the Yield on the 10-Year Treasury Matters

There are several reasons to keep a close eye on the yield of the 10-year Treasury note even though investing out 10 years is far beyond the horizon for most public funds portfolios.

- Ten-year Treasuries make up less than one percent of Treasury’s $37 trillion of outstanding debt. Yet the yield on this maturity has an outsized effect on overall market sentiment because it is a key rate behind interest rates on home mortgages, corporate borrowing and, on a tax-adjusted basis, tax exempt borrowing by states and local governments.

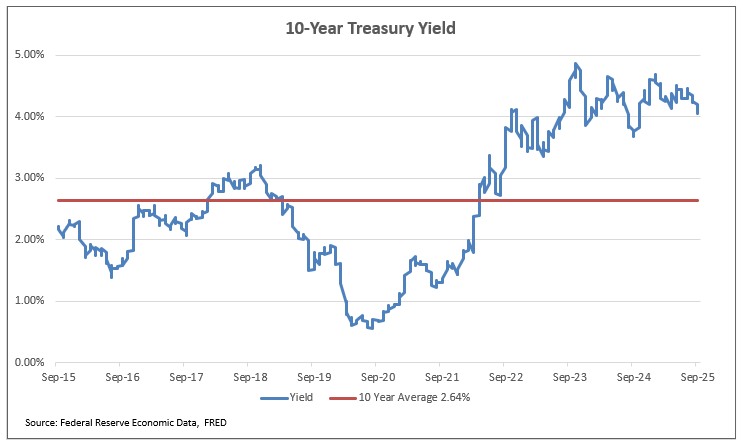

- The yield on the 10-year Treasury note has ranged over 80 basis points so far this year. It is lower now than it was at the beginning of January by about 46 basis points (4.56% to 4.10% at this writing) and if you bought the note on January 2, you would have earned an annualized return of about 9.30%. Not bad for a fixed income investment with no credit risk.

- That return assumes you had US dollars to invest. A foreign investor whose initial or ultimate requirement is for a local currency would most likely have suffered a loss in the investment because the income and appreciation received from investing in the 10 year Treasury for nine months would have totaled about 6.50% while the dollar likely would have lost money compared with the local currency—about 12% based on a trade weighted basket of currencies. Back of the envelope—never mind bond math—earning 6.50%, losing 12% is not a profitable investment.

- Foreign investors, particularly sophisticated foreign investors like central banks, understand this. They may not love Treasuries, but they end up with dollars because of a trade surplus with the US. (Capital flows balance the surplus.) Their only other alternative would be to sell dollars and buy their own currencies, but this would have the effect of raising the value of their country’s money, thus hurting the competitive position of their exports in the global economy. So buying Treasuries would be a lesser evil.

- Not to say that their purchases are confined to 10-year Treasuries. In fact, foreign investors have shortened the duration of their Treasury holdings in the recent period and are now buying more Treasury bills, but this adds volatility to their holdings complicating their management of their currency’s value.

A measure of inflation expectations?

Popular perception is that the yield on the 10-year Treasury tracks investor perceptions of the future rate of inflation. If so, the yield on the 10-year Treasury should move in step with inflation expectations. But the linkage is not apparent.

For example, the chart below compares the 10-year Treasury yield with an index of inflation expectations over a 10 year time horizon compiled by the Cleveland Federal Reserve Bank. Comparisons with other indicators of inflation tell a similar story: 10-year Treasury yields and inflation expectations live in somewhat separated worlds.

One way to think about the yield on the 10-year Treasury is to look at it as a measure of the minimum yield required on a risk-free overnight investment adjusted to compensate the investor for the cost of liquidating the investment over its term. If you are certain that federal funds would average 3% over this period, you might be content to invest in a 10-year Treasury at a rate slightly higher than 3%, with the premium reflecting the cost to obtain liquidity in the event you needed money sooner than 10 years. The current 10-year Treasury note is highly liquid, and you can sell it at a cost of less than one basis point of yield. Once the 10-year ages and becomes a nine year or eight-year security the cost of liquidity rises, but not by very much.

In this analysis you might be satisfied investing money for 10 years at a yield that is only few basis points more than the expected future overnight rate. Thus, you could look at the current yield on the 10-year Treasury, let’s say 4.10%,and deduce from this that investors perceive short-term rates will be around 4.00% for the next ten years. (I know, this analysis is a bit simple minded because it ignores the time value of money; if you insist on the rigorous version you can reach a similar conclusion.)

But if you deduced that short term rates were going to average 4.00% over the next decade you would be ignoring other important factors in the valuation: the requirement that many investors have to mark their holdings to market, thus reflecting unrealized gains/losses, or the possibility that you would need to sell your holding prior to maturity at an unfavorable rate and/or a wider bid/offered spread, thus incurring an unexpected loss.

You might expect that investors will demand some added compensation to assume these risks. Economists have dubbed this the “term premium” to describe additional yield required to induce investors to invest for a term that is longer than overnight. The term premium cannot be calculated or observed directly. In this way it is a concept rather than a specific figure like the spread between two securities. The premium represents added compensation for uncertainty related to liquidity and price volatility (aka “risk”) during the holding period.

Since the term premium is not directly observable it is not useful for adjusting the 10 year Treasury yield over time to isolate the forecast for short term rates. Maybe these rates will average 4% with little volatility over time, or maybe they will average 3% with a lot more volatility.

Both could explain the current yield on 10-year Treasuries. We may not be able to quantify the term premium and its changes over time; nevertheless the 10-year Treasury yield speaks to market perceptions of future volatility and liquidity. The term premium feels higher today than it was a couple of years ago, a sign of caution with regard to the outlook for volatility, liquidity Treasury risk.

(It might surprise that while Treasuries are often characterized as risk-free that doesn’t mean they enjoy the lowest yield for a fixed income investment with a specific tenor. These days the rate on a 10-year Overnight Indexed Swap is about 50 basis points lower than the yield of a 10-year Treasury. But that’s a story for another day.)

10-Year Treasuries and the Short-Term Funding Market

There is another element to the yield of the 10-year Treasury and that relates to the ability to finance ownership with borrowed funds. If the Treasury is risk free one should be able to finance ownership of a Treasury bond or note over its life by paying a lender at a rate close to the risk-free short-term rate (the Secured Overnight Financing Rate). Of course, the lender will be unlikely to finance 100% of its value, so you would have to put up some of your own money (Let’s call it “margin.”)

This strategy depends not just on the yield of the 10-year Treasury but also on the financing rate which can be fixed in the futures market for at least a portion of the 10- year term (think SOFR futures). In that sense the yield on the 10-year Treasury partly reflects the outlook for short-term rates. Ten-year Treasuries would tend to appreciate in price if/as financing rates decline. So, the 10-year Treasury provides signals about interest rate levels and functioning of the short-term repurchase agreement market.

Bottom line

The 10 year Treasury yield contains important signals for investors in short-term securities and currently it signals “caution.”

The Federal Reserve’s Summary of Economic Projections, (including the dot plot), updated earlier this week, forecasts slow but steady economic expansion, inflation gradually returning to two percent and an overnight rate of around three percent in 2027. The futures for federal funds and SOFR derivatives indicate the federal funds rate will decline to three percent next summer. And the Trump Administration claims that Federal borrowing needs will decline notably as growth and tariff revenues reduce the budget deficit.

Yet the ten-year Treasury yield is stuck at a level above 4%, well above its average over the past 10 and 20 years. It is a signal to public funds investors that the risk of a miss in this outlook is real.