Calm or Complacent: Short Term Markets Are Uncertain

You might think that the recent news on the economy would lead to big market moves. Tariffs—on, off or . . ., a partial government shutdown (again), a 20% swing in oil prices since September, the sharp rise in the price of gold, a new Federal Reserve chair in waiting. And President Trump continues to attack the current Fed chair. And remember the case pending before the Supreme Court that could validate the President’s authority to fire a Federal Reserve governor? Not to mention the recent crash in crypto that has wiped out around $2 trillion, the stress in the private credit markets, and the significant rotation in equities that have turned winners (software companies) into losers.

You might think that the recent news on the economy would lead to big market moves. Tariffs—on, off or . . ., a partial government shutdown (again), a 20% swing in oil prices since September, the sharp rise in the price of gold, a new Federal Reserve chair in waiting. And President Trump continues to attack the current Fed chair. And remember the case pending before the Supreme Court that could validate the President’s authority to fire a Federal Reserve governor? Not to mention the recent crash in crypto that has wiped out around $2 trillion, the stress in the private credit markets, and the significant rotation in equities that have turned winners (software companies) into losers.

Before heading for the fallout shelter, check here:

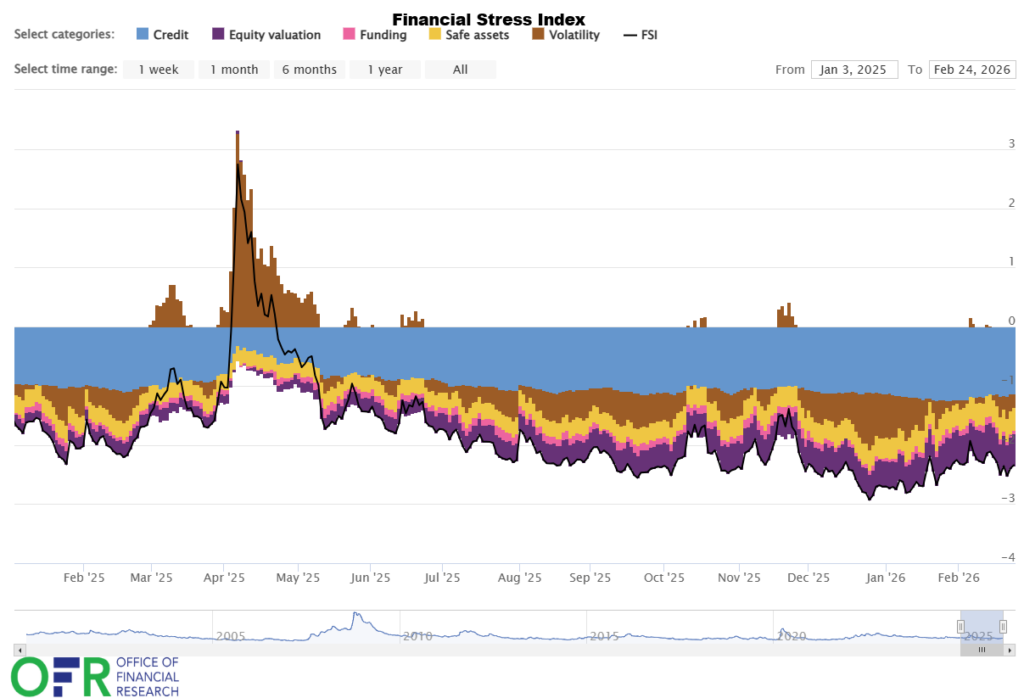

- The Office of Financial Research, which monitors markets for the Treasury, publishes a Financial Stress Index daily. Here is what it looks like.

The last spike in April 2025 was around the (now voided) tariff announcement.

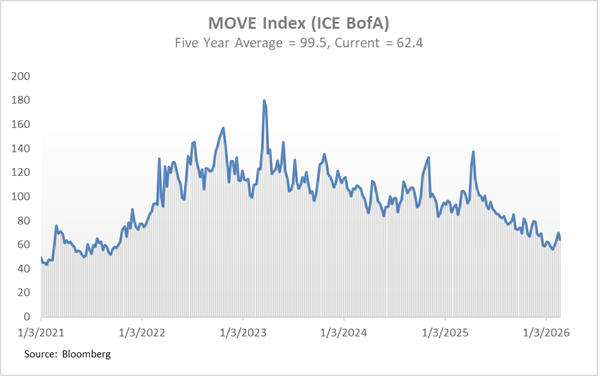

The last spike in April 2025 was around the (now voided) tariff announcement. - Market stress indicators remain at modest levels. The MOVE Index, a good indicator of bond market volatility, is now at 62.4; its average over the past five years was 99.5.

VIX, which measures stock market volatility, is at 19.3, about the average over this five-year period.

VIX, which measures stock market volatility, is at 19.3, about the average over this five-year period. - In the corporate market, despite cracks that have appeared in credit (see our November 19, 2025 post) the three major ratings agencies have continued to upgrade more credits than they downgrade. Year-to-date the ratio is 2.75 upgrades for every downgrade, about the same ratio as in the past several years.

There are cautions as well

- Credit spreads—the premium that investors demand to hold corporate bonds instead of Treasuries—have widened from very tight in January to near their one-year average. (They’ve widened but not blown out.)

- High yield bonds (FKA junk bonds) have underperformed those that are investment grade. Their returns since January 2 are in the range of 0.7% (annualized to 5%) compared to returns on broad measures of investment grade bonds that are about double that. (That’s not good, but hardly a four-alarm fire.)

- Consumer debt loads are high by historic standards, and delinquencies have risen. (Higher than recently but not rocketing up.)

Head in the Sand?

The short-term markets, which are the focus of public funds investors, seem indifferent to latest news. Head in the sand? Complacency? Or maybe they’ve got it right: the scare headlines will attract eyeballs but that’s about it.

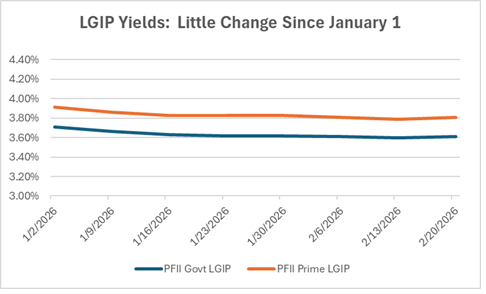

In the public funds world stable value local government investment pool yields have barely moved so far this year, after tracking the federal funds rate lower when the Fed cut in early December.  They are the highest number on the board, though whether they will keep producing at current rates depends on whether/when the Fed cuts rates. If it is soon, you’ll regret not locking in a fixed rate now. If not before fall, or maybe not even then, the current LGIP advantage will persist.

They are the highest number on the board, though whether they will keep producing at current rates depends on whether/when the Fed cuts rates. If it is soon, you’ll regret not locking in a fixed rate now. If not before fall, or maybe not even then, the current LGIP advantage will persist.

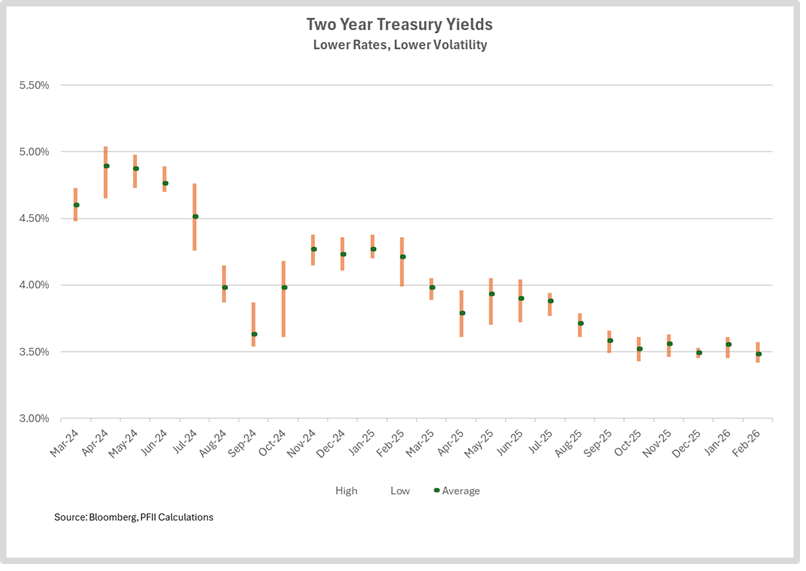

For a longer view of market volatility, look at the trading range of two-year Treasuries, for many a bellweather of the short-term markets. The chart below plots the high, low, and average rates for each month over the past two years. Rates are down, of course, but what’s also notable is that rate volatility, the difference between highs and lows, has compressed remarkably in recent months. Rates are traveling over shorter ranges these days. That’s a benefit for fixed term portfolios that produce steady income and have had smaller swings in mark to market adjustments in recent months.

Rates are down, of course, but what’s also notable is that rate volatility, the difference between highs and lows, has compressed remarkably in recent months. Rates are traveling over shorter ranges these days. That’s a benefit for fixed term portfolios that produce steady income and have had smaller swings in mark to market adjustments in recent months.

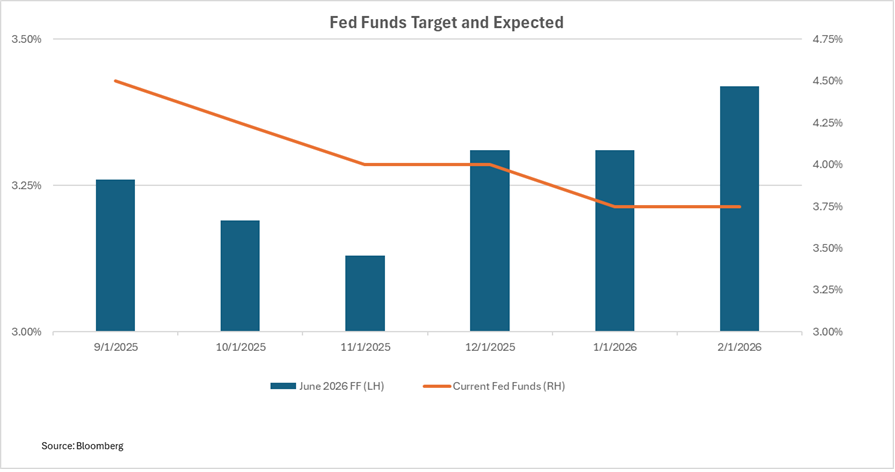

Could it be that investors have gained confidence in the future direction of rates? Perhaps but that’s not what tracking the futures market suggests. We looked at the changes in market expectations for the level of fed funds in June 2026 starting last September. It’s moved from 3.26%, down to 3.13% in November, but more recently up to 3.42%, even as the current federal funds rate has declined from 4.50% to about 3.65%.

So central bank policy has eased by 75 basis points while expectations for the near-term future have moved up! Seems as if the goal posts are moving.

Clouding all are questions on the economy. The government shutdown in October/November distorted economic activity but also delayed, distorted, or eliminated some of the key data that measures the state of the economy. Then there is the disconnect between the strongly asserted views of the Trump administration that the economy is bursting ahead and the angst of American consumers.

Not to mention the potential for conflict in the Middle East, the possibility for wholesale economic disruption around the rise of artificial intelligence, and highly contentious immigration issues.

Fixed income investors are betting that we’ll get from here to there without stress. Time will tell.