Sometimes No News Is News

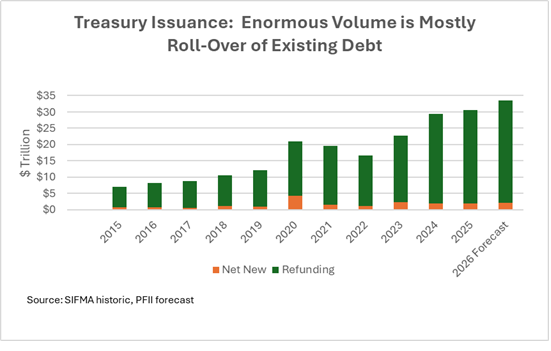

The numbers are staggering. Last year Treasury issued $30.5 trillion of securities to fund the national debt. That’s nearly $600 billion a week. This year, through April issuance was $10.8 trillion, 10% ahead of the 2025 pace. Most of this is to refund/rollover existing debt but some is for new debt that will be required to fund the $2 trillion budget deficit that is forecast for this year.

The numbers are staggering. Last year Treasury issued $30.5 trillion of securities to fund the national debt. That’s nearly $600 billion a week. This year, through April issuance was $10.8 trillion, 10% ahead of the 2025 pace. Most of this is to refund/rollover existing debt but some is for new debt that will be required to fund the $2 trillion budget deficit that is forecast for this year.

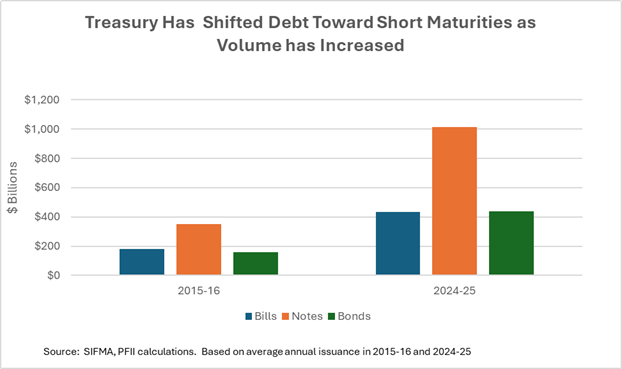

The guide for all of this is a schedule that Treasury refreshes quarterly as it undertakes to issue a new round of notes and bonds. Treasury forecasts its issuance of securities with maturities of greater than a year through these quarterly announcements, then it fills the balance of its needs by issuing bills (maturing in 12 months or less) on a much more flexible plan.

The schedule that Treasury announced this week was notable in that it contained no news. That means Treasury will continue to finance the major portion of its debt in the Treasury bill and note market relying on short-term investors (Treasury notes mature in 10 years or less).

It will not seek to increase the size of its recent issuances of securities. This was surprising to some in the face of a need to refund $150 billion or more of tariffs declared illegal by the Supreme Court in February, fund billions in unbudgeted expenses related to the Iran war and pay for the pending reconciliation appropriation for the Department of Homeland Security.

Public funds investors, who collectively hold $1.7 trillion or about 40% of their investment portfolios in Treasuries, the majority of it in bills and short-term notes, can breathe a sigh of relief perhaps, that markets will not be disrupted by changed issuance plans by Treasury.

At some point existing buyers may say “enough” and demand better terms/higher rates to remain buyers, but Treasury, and its primary dealer advisers, believe the market can continue to accommodate this schedule for the next several quarters without adjustment. It means Treasury will continue to depend on short term interest rates but will avoid tapping the long-term market where it competes more directly with corporate bond issuers and mortgages. With long term rates higher than the Trump administration would like, this is understandable as long as it can be carried forward.

Treasury and market makers keep a close eye on market health and liquidity by observing the bid to cover ratio of auctions—that is the extent to which demand exceeds supply. Recent data show that there is around three dollars of demand for each dollar of new issuance, a level that assures all securities will be bought at the auction price.

Market liquidity is also a factor. Treasury market efficiency is reflected in the (usually) small differences between bid and offered prices on bills and notes. These days an investor would pay about $100 to sell a $1 million one-year Treasury bill and about $75 to sell the actively traded two-year note. They might pay about $300 to sell a less actively traded note. These bid/offered spreads indicate a highly liquid market.

As long as Treasury can maintain these levels things are good.

What could change?

Treasury’s borrowing requirements could change, and probably will, at some point soon. There are these factors:

Federal spending continues to outpace revenue. In round numbers the budget deficit is growing by about $2 trillion a year, and its share of both financial assets and gross domestic product are increasing. Deficit hawks warn that at some point the market could rebel and demand better terms—aka higher rates—to function.

New sources of spending could require borrowing. In addition to the tariff refunds and cost of the Iran war, which some have estimated to be between $50 and $200 billion, there is the possibility that Congress will pass another budget reconciliation measure this year to raise spending or cut taxes for a variety of programs.

How fast the economy grows has a direct impact on federal revenue. The Trump administration (Office of Management and Budget) expects GDP to expand at 3.5% this year and 3.1% in the next two years. Other forecasters, including the Congressional Budget Office, the consensus of Bloomberg economists and International Monetary Fund expect growth to be about one percent lower. Treasury’s debt issuance plans are based on the higher GDP forecast. The difference could require $150 to $200 billion of added debt financing each year.

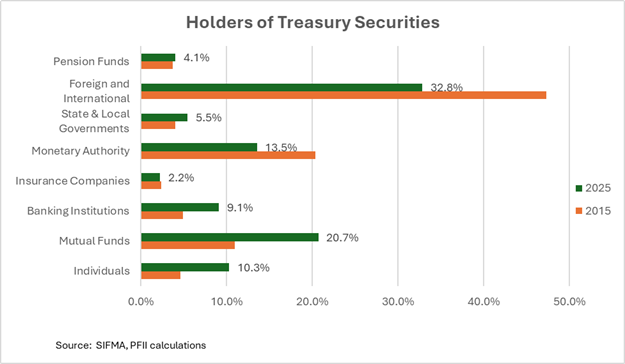

Who Buys Treasuries?

Changes to the buyer community matter. Here is a chart on holdings of Treasuries by holder type. Foreign holders accounted for nearly half of outstandings in 2015; Last year they were about one third. So, while their total holdings increased from $6.2 to $9.3 trillion, they make up a smaller share of the current borrower community. Moreover, foreign buyers have shifted their holdings in the past decade in favor of bills, giving them less exposure to the long-term Treasury market.

Much is made of the role of the Fed in the Treasury market, and it is substantial, with their holdings of about $4 trillion, but the Fed holds a smaller share of outstanding Treasuries than it did a decade ago. About 12% of its portfolio is in Treasury bills. This compares with nearly 25% of Treasury’s total debt in bills. There is speculation that the central bank will move to increase its holdings of bills to match more closely the issuance profile of Treasury. How it might accomplish this in a reasonable period without selling longer-maturity holdings—something the market would not like to see—is unknown, but a change like this could depress demand for notes and increase demand for bills.

Individuals, mutual funds, including money market funds and banks all have increased their holdings of Treasuries in recent years and Treasury recognizes that they are critical to the Treasury’s ability to place its debt. Treasury Secretary Scott Bessent has made a big deal about the potential for these buyers to step up to buy the increasing amounts of Treasuries that will be issued in coming years. Continuing to emphasize issuance of bills seems designed to anticipate these buyers, particularly government money market mutual funds whose assets have expanded from $3.7 trillion to $6.7 trillion since 2020.

Relaxed capital requirements for banks are touted as incenting them to hold Treasuries, and crypto promoters point to the Genius Act legitimizing the stablecoin business which they see as providing demand for trillions of dollars of Treasuries to back their coins.

We’ll see.

A skeptic would ask why banks would invest in Treasuries, even with no capital required, when they pay barely more than the rates the banks pay for deposits. Lending would seem to be a better deal, even with its associated capital requirement.

And money to buy stable coins must come from somewhere. Perhaps the underground economy, but otherwise it’s likely to come from mutual funds or individual accounts—a zero sum game. Or, like so much in the market these days, it might just be imagined.

Bottom Line

The market reaction to the Treasury’s announcement provides validation of its current strategy. Market expectations/fears are a strong force, and Treasury is a price insensitive seller. Investors/market makers were not begging for change. For them, no news is fine.