Ya Wanna Bet? The Rising Place of Prediction Markets in Investing

Would you go to a betting parlor to invest? Before you answer, consider:

- Betting on predictions and investing have a lot in common. Investors regularly use the vernacular of betting to describe market activities. We make “bets” on relative value, the future direction of interest rates and the likelihood that an investment we make might be impaired. We might describe the “chance” that the Federal Reserve will raise or lower its central policy rate at an upcoming meeting. And we may characterize portfolio diversification as an attempt to make many small bets.

- Economists say that prediction markets are better at identifying outcomes than data driven models and forecasts. If so, at a minimum you may want to check Kalshi or Polymarket for the value of an interest rate product before you buy a Treasury or move money into or out of an LGIP.

But also consider this:

- As prediction markets grow and expand in the financial mainstream they create new sources of financial instability. Trouble in the prediction markets could metastasize into a general financial market problem, stressing conventional investment markets and requiring market intervention that could affect all investors.

Deep Dive

Investing and betting have a lot in common.

Investing represents an action that attaches a consequence (committing money) to an outlook. Betting does the same, though in common usage the term “bet” may imply characteristics that seem inappropriate, particularly for public funds investors. Investment professionals are viewed differently than bettors or—heaven forbid—professional gamblers.

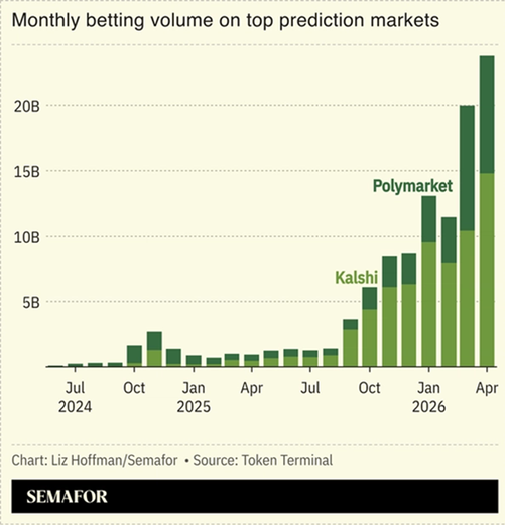

Yet the sharp rise in the volume of prediction market activities and moves by start-ups like Kalshi and Polymarket to bring them into the financial mainstream raise interesting possibilities for investors.

For example, if you think the Federal Reserve will maintain its target rate of 3.50%-3.75% through December you might express this view by investing funds in a prime local government investment pool (or money fund) currently yielding 3.75%. As of this writing, that would give you more income than buying a Treasury bill that matures in early December because the floor on the LGIP yield is almost certainly to be higher than the federal funds target rate.

To make this investment decision you might analyze the most recent announcements of the Federal Reserve, consider the most recent forecast of your favorite market economist(s) or build a forecasting model that uses some or a vast amount of economic and market information. (You might ask Claude to do this for you!). If you have access to a Bloomberg terminal you might run their WIRP model, or consider the target fed funds forecast available on the CME Exchange website.

But you also could look at Kalshi. At the close of business yesterday both the Bloomberg and CME models ascribed a 75% chance to an unchanged fed funds rate in December. Kalshi bettors put it at 69%.

You might consider taking some of the funds you have to invest and using them to “bet” on a lower federal funds rate to provide a hedge in case your main bet of investing in the LGIP is wrong and the Fed reduces rates by December. Kalshi and federal funds futures prices imply different costs for this hedge, one approach may be easier than another to execute and one may or may not be legal, but these (important) details should not obscure the point.

Or look at the market for Treasuries. You can buy the 10-year Treasury now at a yield of 4.60%. You can also “bet” on its yield at the end of the day or by the end of the year by using an interest rate option to hedge will be at a certain level in the future. Or you can “bet” on Polymarket that the yield will go to 5% by year-end. If so the loss of value in the Treasury you buy today could be offset by the gain in the bet.

Put aside for the moment the details that Polymarket doesn’t operate in the U.S. and that states and locality investment policies are unlikely to be friendly to betting. But still. . ..

The Common Thread

The common thread is that the conventional investment market and the prediction market provide an outlook with a consequence (make an investment or a bet, receive a return if you are correct) for a similar event.

This similarity has intrigued economists for a long time. And their analysis has concluded that prediction markets are somewhat better at forecasting future events/outcomes than the alternatives–economists’ forecasts, statistical models and polling. The reasons relate to the fact that betting incorporates not just information but also psychology, that prediction outcomes are continuously and quickly updated/calibrated by new bets, and that they incorporate the wisdom of crowds.

Finally, what should be an obvious point: you don’t have to bet on the prediction markets to incorporate its information into your thinking about the direction of rates, or about the forward path of political or economic factors that you think are important to your investment plans.

New Market Risks

The rising presence of prediction markets also creates new risks for investors. This is particularly true because we are at a time when innovation is “in” and regulation is “out,” so to speak.

History is instructive here. Prediction markets trace their origins to the unregulated gambling business. Their largest volumes, by far, are sports betting, followed by betting on election outcomes. As long as they were confined to these areas they presented little risk to vital financial systems or the economy, though the periodic bouts of a sports star acting at an event to benefit their stake in a prediction market contract seemed so unfair that various rules/laws have been promulgated to try to prevent this.

In an odd way the effort to improve reliability of predicting outcomes through unfettered betting is opposed to the idea of “fair” betting. The accuracy and speed with which the betting markets can make a prediction are improved if the people with first knowledge can place a bet without delay. But when anonymous bettors learned of events related to the Iran war that were going to affect oil prices and bet accordingly, this triggered calls for investigations because they seemed to have some knowledge advantage over other bettors in the regulated commodities markets.

The potential for damage is amplified when prediction markets grow and when their events overlap with financial instruments. A bad actor in the sports betting arena may harm the reputation of the betting venue, but if/when the venue is integrated into the overall financial system and the volume of prediction-based bets is large the damage can be magnified.

The federal government and some states have jumped on this. Some of the initiatives are motivated by consumer protection interests while others might be turf protection efforts. The casino companies are aghast at the idea that CME Group, the operator of the Chicago Mercantile Exchange, is going to invest in FanDuel. CME Group seems to have something in mind beyond owning an online casino venue.

Bottom Line

It seems that we are headed to a world where betting and investing activities converge. It would be one of the odd consequences of the financialization of most everything we know.