Kevin Warsh: Behind the Senate Testimony of the Federal Reserve Nominee

Beyond the sound bites from this week’s Senate Banking Committee hearing on the nomination of Kevin Warsh to chair the Federal Reserve are three issues that are much more important for the markets and economy than whether President Trump or his political adversaries “win” or “lose” this latest contest of political will.

They are shrouded in the complexity and uncertainty of economic theory but consider these factors.

The Fed’s balance sheet.

Warsh is a proponent of reducing the Fed’s balance sheet. The question is “How?”

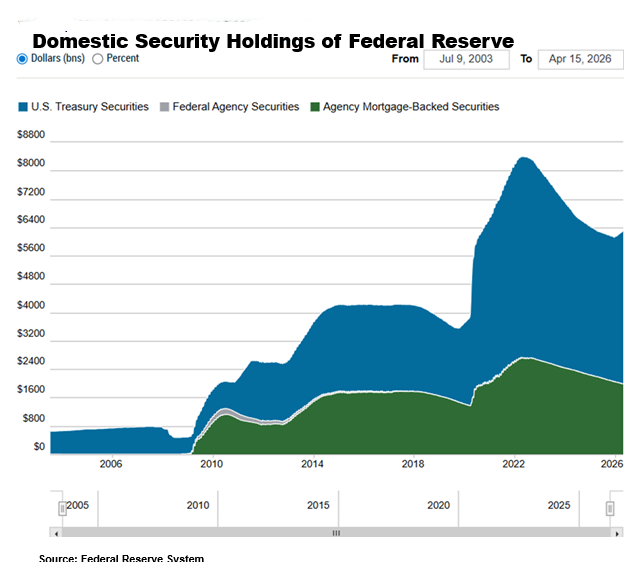

As the accompanying chart shows, the central bank owns $6.4 trillion Treasury and mortgage-backed securities, bought in the 2008-9 and  2020-21 financial crises to stabilize the financial markets. This makes it a major player in the fixed income markets. Its holdings represent ten percent of all outstanding Treasury securities and 18% percent of outstanding mortgage-backed obligations. Without that ownership, which is insensitive to yield/price, other buyers would have to be found by raising offered yields or perhaps compelling ownership though capital controls.

2020-21 financial crises to stabilize the financial markets. This makes it a major player in the fixed income markets. Its holdings represent ten percent of all outstanding Treasury securities and 18% percent of outstanding mortgage-backed obligations. Without that ownership, which is insensitive to yield/price, other buyers would have to be found by raising offered yields or perhaps compelling ownership though capital controls.

The Fed has tried to reduce its market presence in recent years but even the modest steps it took to allow securities to run off created volatility and liquidity challenges in the Treasury market. This disruption led the Fed to begin buying Treasuries again, though in modest amounts, in December 2025.

With Treasury expected to issue $2 trillion(!) of new debt in each of the next several years to fund the federal deficit this challenge is likely to get bigger, not smaller.

If not the central bank, who would step in to buy? Foreign accounts (whose presence is both wooed and dissed depending on the whims of international politics)? Banks (whose shareholders expect the level of returns supported by commercial lending, M&A and trading profits)? Consumers (who have reduced their savings rate to maintain current consumption levels in the face of rising prices)?

Likely none of the above. Rather, behind the arcane analytics of monetary economists there appear to be these possibilities: Higher rates on Treasuries would be needed to draw money into the market, or the Fed could substitute outright holdings of Treasuries with a program to finance them through a lending or repurchase agreement program. Of course, the Fed would have to pay lenders a premium over the rate they earned on the Treasuries to make a lending program viable. So, the composition of the Fed’s balance sheet might change but the Fed would remain a major presence in the market.

Economists characterize these efforts to finance government debt as “fiscal dominance” or “fiscal repression” because they distort economic and market activity in favor of financing the national debt.

In short, more Treasury issuance and an active Fed will be forces to keep short term interest rates elevated, not to reduce them. So, unless the economy crashes, don’t expect Trump’s touted one percent interest rates soon.

Foreword guidance.

Warsh has been critical of the use of “forward guidance” to indicate the future direction of the Fed’s policy, characterizing it as “unhelpful.” But be aware of its heritage. The concept stems from the tenure of former Fed chair Alan Greenspan who Warsh has said he looked to for inspiration, and Ben Bernanke, the Fed chair with whom Warsh served when he was first a Fed governor.

It was their version of jawboning to keep from having to take drastic action (remember negative interest rates?). And it gives investors an opportunity to adjust portfolios over time. (Think of the result in 2022 if the Fed had raised rates from one percent to four percent in one move.)

Investors have come to expect clarity and transparency of purpose around the central bank’s actions, and I’d bet that Warsh’s effort here will not eliminate forward guidance but will lead to a move—over time—to speak with one voice rather than many.

Perhaps say goodbye to the dot plot and Summary of Economic Projections because these dilute the unitary expression of the central bank’s intentions. And set some informal limits on what other members of the Federal Open Market Committee talk about in public comments.

That could also result in a more flexible FOMC. Members might be more likely to move from their positions if they are less public. It may drive the talking heads, and radical transparency advocates a bit crazy; whether it will lead to better Fed policy is hard to know.

Fed independence.

Some have characterized this nomination as a struggle to succumb to or resist Trump’s thumb on the scale. But there is another perspective—that this will reduce the Fed’s involvement in matters that are seen as not central to setting monetary policy.

The Fed’s efforts during the Biden years to incorporate climate change, consumer protection and diversity, equity and inclusion in its policies drew strong pushback from banks and free market advocates. When the clock turned in 2024, the central bank worked with other regulators, the Federal Deposit Insurance Corporation and Office of the Comptroller of the Currency, to rework regulations around bank capital requirements and stress testing, remove requirements that banks consider reputational risk in their business, and eliminate explicit efforts around climate change, diversity, equity and inclusion.

A truly “independent” Fed might resist these efforts to coordinate policy with that of the administration but the banks, who are the Fed’s first line constituents, and Republicans in Congress, who are now in the majority, supported the current round of coordination to undo the prior coordination that they objected to.

What will they say when the politics in Congress and the administration change?

A cynic might guess that they will not be amused if a new administration argues for coordination of central bank policies when the policies take on a different flavor.