Why Five Percent Yield on the 30 Year Treasury is a Big Deal

The yield on the 30-year Treasury bond broke above five percent this week, and it’s kind of a big deal. It’s not that five percent triggered some pre-set realignment in the financial markets, or that the level resulted in a quantum change in gains, losses or winning and losing positions as compared with those positions a week or two ago when the 30-year bond traded at a yield of around 4.90% or 4.95%. (Full disclosure: it briefly touched five percent a couple of times but not in a convincing way.)

Rather it is a very visible sign of the power of psychology on investor behavior.

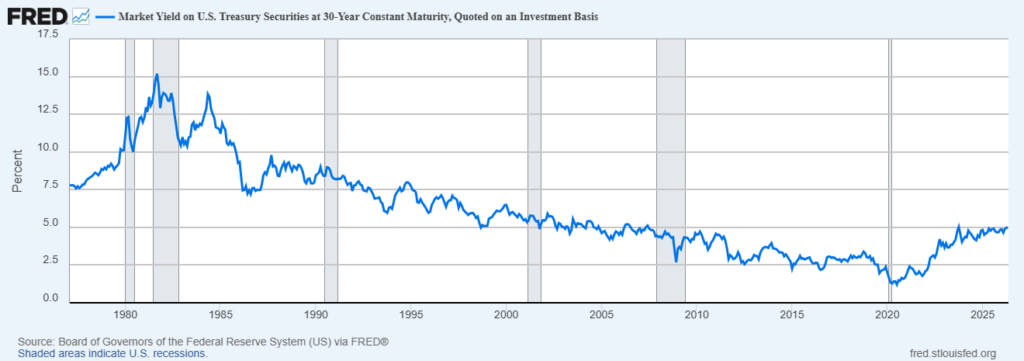

Taking a long view, as the accompanying chart shows, the move is almost insignificant. Since 2020 the 30-year Treasury yield has ranged from around one peercent in February 2020 to its current level. Though it should be noted that if you bought the bond at its low yield, you would have lost about 55% of its value in the past six years!

Going back to the 1980s, the yield on the 30-year Treasury was as high as 15%. It ended last week with a yield of 4.93% then added seven basis points of yield to break through five percent early this week.

To understand how a (mere) seven basis point move in yield could generate headlines you have to put math and quantitative analysis to the side.

The sophisticated valuation models that have been created by economists, mathematicians and quants do not provide a satisfying explanation for the psychological forces that move markets.

Five is a round number; 4.93% is not, but that is only a small part of the story.

In some weird way five percent is significant simply because (some) investors believe it is, and for them the bond yielding greater than five percent has crossed a line. It’s not a line that is drawn because of fair value pricing, breakeven analysis, or another financial math expression. It is because it is.

Bond market bears point to inflation (this week’s measure showed consumer prices rose at an annual rate of 3.8% in April), oil prices (retail gas is now about $4.50 up from $3.15 a year ago), failure of Washington to deal with the growing federal budget deficit (it is forecast to be about $2 trillion this year) and rising fiscal dominance (personal savings rates are down, the need for capital to fuel the economy is up).

But all these factors were present and moving in the same direction last week or last month.

Why not call it when the 30-year yield broke through 4.93% last week or 4.90% last month?

Well, it’s because financial markets are moved by psychology as well as by math.

At the risk of over-simplifying, asset valuations—yield in the case of bonds—seem to derive from two sets of factors. One (the efficient market hypothesis) argues that they reflect available information and if we could collect and interpret all information relevant to an asset’s value we could “predict” the value accurately.

Bigger models, faster models, more data are fused in the search for clarity around the value of an asset. Michael Bloomberg built a fortune around efforts to further this hypothesis and today many investment managers rely heavily on it.

Before they buy a two year Treasury they want to know it’s recent prices, where other, similar securities are priced, what economic and market data may be released in the near term that could affect its value, what other investors are willing to pay for securities that derive value from the two year Treasury, etc. etc.

Whether the information collected leads to the correct decision will be known only after the fact, but collecting and analyzing it does constitute evidence of diligence and sound thinking. Particularly important for those who operate in the public funds investment fishbowl.

By contrast, if you were to buy the two-year Treasury on a “hunch” informed by checking Reddit to take the “pulse” of the market and chatting with some buddies while playing the latest version of Roblox that might be viewed as being highly unprofessional, to say the least.

It’s not to dismiss the hypothesis that information and an efficient market framework is informative, but rather to recognize, as with the five percent threshold, that psychology matters, and sometimes it matters a whole lot.