Beyond the Fed: Why This Week’s Events May Be Less important than You Think

I’m guilty of having spent a good deal of time over the last two weeks on the eye-catching news on interest rates: the Senate hearing on whether to confirm Kevin Wash as the next chair of the Federal Reserve, the move by the Department of Justice to end a criminal probe of Jerome Powell, the current Fed chair, the debate over whether trimmed consumer prices are a better way to measure inflation, the decision by Powell to remain a Fed governor when his term as chair ends next month, the dissent by four members of the Federal Open Market Committee from its post-meeting statement, and a bunch of other made for streaming moments.

I think I’m well-prepared to take a monetary policy trivia exam.

But I also have been thinking about developments that are behind the scenes and over time could be much more important factors in the future interest rate path. Individually and collectively they have the potential to keep interest rates elevated for a long time. If that happens investors, including public funds investors, would benefit (while borrowers lose).

Digging deeper

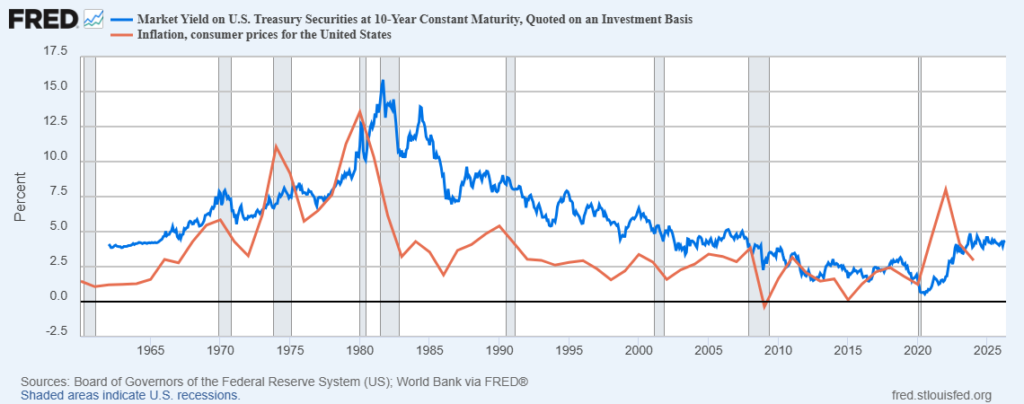

The next years are likely to be characterized by de-globalization of developed market economies, reversing the effect that globalization had on costs and prices over the past 40 years. The accompanying chart tracks consumer prices and 10-year Treasury yields going back to 1965.  Some prominent economists, notably Alan Greenspan the former Fed chair, pointed to globalization, in the period from 1980 to 2000, as the force behind a falling inflation rate that led to record-low interest rates in the post-2008 period. They argued that technology changes, the end of the Cold War, and the emergence of stable political systems in much of the world led businesses to reorganize production offshore and replace domestic supply chains with global ones. The globalization dividend, if you will, was realized when efficiencies reduced price pressures and inflation.

Some prominent economists, notably Alan Greenspan the former Fed chair, pointed to globalization, in the period from 1980 to 2000, as the force behind a falling inflation rate that led to record-low interest rates in the post-2008 period. They argued that technology changes, the end of the Cold War, and the emergence of stable political systems in much of the world led businesses to reorganize production offshore and replace domestic supply chains with global ones. The globalization dividend, if you will, was realized when efficiencies reduced price pressures and inflation.

While there is some disagreement among economists on the cause-effect (the notion that economists would agree to anything is an oxymoron) it is at least interesting to consider a dynamic where the unraveling of globalization will create inefficiencies and new price pressures as businesses move to re-shore production and re-orient supply chains.

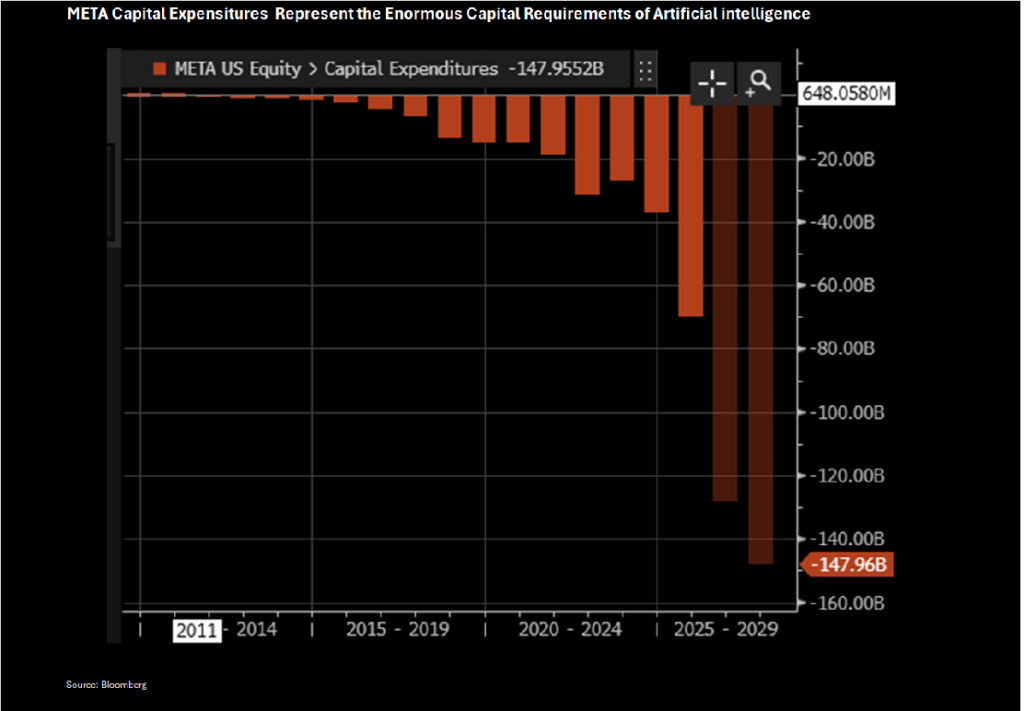

Capital deepening means higher rates. Where will the capital come from to support the hundreds of billions/trillions of dollars contemplated in the artificial intelligence boom and re-shoring move? Take Meta, the former Facebook company. Bloomberg reported that it will spend nearly $150 billion (!) this year on efforts to expand its technology. That’s four times more than it spent on an annual basis in the pre-covid years.

Meta had essentially no long-term debt in 2020. It finished last year with $58 billion, and it is looking to finance as much as $25 billion in a single bond sale as I write this.

To raise this kind of capital—and Meta is but one example—you must make it worthwhile for players in the economy to divert money from other uses. Remember the formula GDP = consumption+investment+government spending from Econ 101? To change the balance, you have to increase the reward for investing/saving.

Capital deepening describes the tendency of an economy to require more capital to support a unit of output as it matures. This makes intuitive sense for manufacturing (or agricultural) output—think costly machines that make workers more productive. But as the Meta example suggests it is also true of the services industry.

The hundreds of billion/trillions of dollars now being poured into building AI capabilities—data centers, computer chips, research and development, etc.—mean diverting resources from consumption into capital.

The diversion can be accomplished by raising the incentive that consumers have to save instead of spending their incomes. Higher interest rates are the way to do it.

Meanwhile there is the requirement to support the growing federal debt. As $39 trillion in total it overhangs the economy and factors into our lives in ways that may be barely visible but are nonetheless significant.

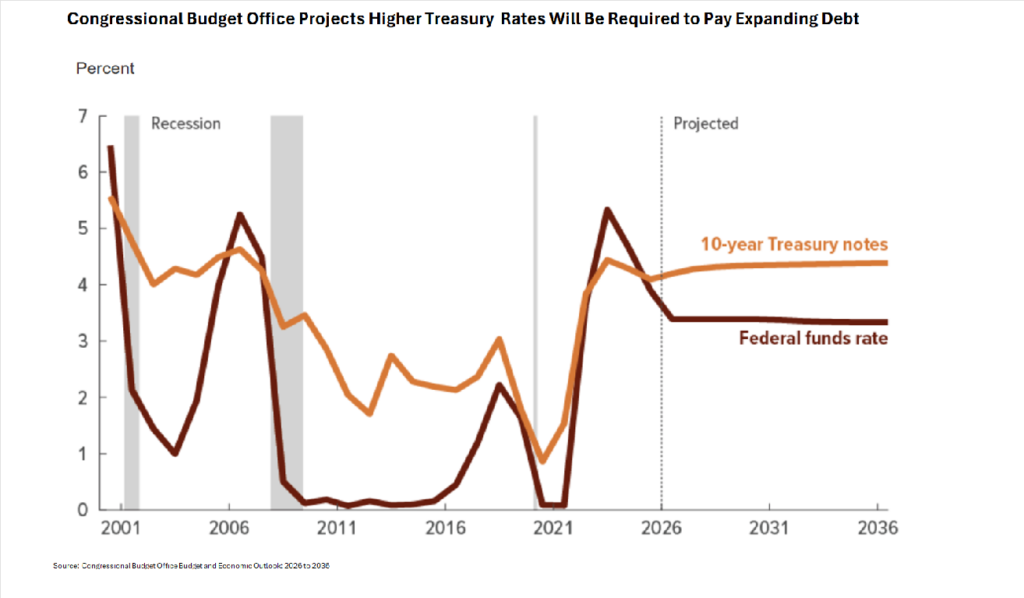

Budget hawks—there are still a few of these about—warn that it will overwhelm the economy. That’s not likely, at least not in the foreseeable future. Treasury will have to raise $2 trillion or more of new debt this year and that or more in subsequent years. This will crowd other borrowers who are seeking the same investment dollars, and it will require an increasing share of national income to pay interest on the debt. The Congressional Budget Office forecast in February that the debt held by the public will grow from $30 trillion to $56 trillion between now and 2036.

The above chart that accompanied the CBO’s February report forecasts federal funds at three percent and 10-year Treasury rates above four percent over this ten-year period. Doable but at high interest rates.

An Ironic Bottom Line

President Trump continues to call loudly for one percent interest rates “NOW.” Until this week’s Fed meeting most economists believed the central bank would lean into lowering rate as soon as it saw an opportunity in the monthly numbers. (The dissenting voters at this week’s meeting suggested this might not be so, but that’s another story.) At the beginning of the year futures markets suggested that at year-end federal funds rate would be three percent. But major Trump initiatives, including efforts to promote re-shoring (via new tariffs), push for changes in the world political order, advocate huge new investments in artificial intelligence, pursue strict immigration policies, and raise federal spending on homeland security and defense all factor into higher interest rates not lower ones.

That’ s not something you observe when you focus on the latest inflation or jobs figures or the current act in the ongoing Washington-based political theatre.