Why the Director of National intelligence is Involved in the Federal Agency Market

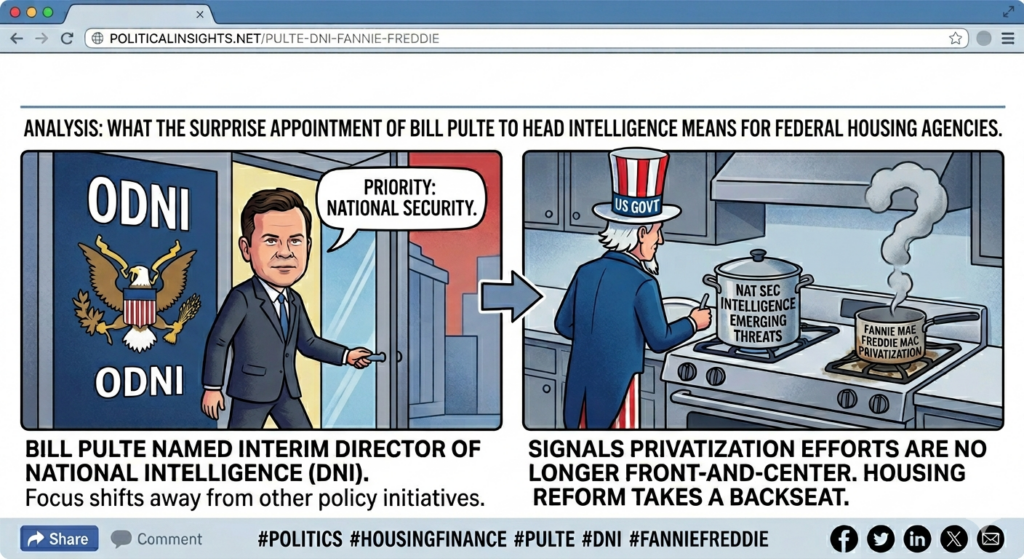

It may not be immediately apparent, but President Trump’s naming Bill Pulte Interim Director of National Intelligence has implications for the Federal agency market where $450 billion of public funds are invested. Before you dismiss this as crackpot, consider:

- Pulte is also the head of the Federal Housing Finance Agency and chairman of both Fannie Mae and Freddie Mac, two major federal agencies. He will retain these roles, but his new responsibility should be seen as an acknowledgement that Trump has backburned the effort to privatize the housing giants. The effort was lagging before Pulte’s appointment. Now it’s going nowhere.

- Meanwhile Fannie and Freddie will continue to operate under conservatorship as they have since 2008. This assures investors that there is minimal risk to holding their direct debt obligations but also means they are likely to offer only small income margins compared to Treasuries.

Catch Up

This is a quick catch-up of a deep dive we made into the agency market last August.

Before the Great Recession federal agencies were the basic building block for public funds portfolios, offering lots of supply at attractive spreads compared to Treasuries. It was not unusual to find public funds portfolios with three quarters or more of their holdings in agencies.

In 2008 overall state and local government portfolios held nearly as much in Federal agency obligations ($444 billion) as Treasury obligations ($523 billion.) The overwhelming majority of agency holdings were issued by Fannie and Freddie whose combined volume that totaled about $1.6 trillion.

Fast forward to today. The $450 billion Federal agency holdings in public funds portfolios compares with $1.6 trillion of Treasuries (out of a total of $4.1 trillion of state and local government investment assets).

Before the Great Recession it was not unusual to obtain 20 or 25 basis points of added yield by investing in agencies. The spread these days is in the single digits—and sometimes negative!

Today the federal agency market is about two thirds the size it was in 2008 ($2.0 trillion vs. $3.2 trillion) and is dominated by the FHL Banks. This has changed its character and the drivers of issuance and value as it is now a central mechanism for the nation’s banks to raise money on a wholesale basis. Bank use rose after the failure of Silicon Valley Bank and has remained elevated.

Fannie and Freddie $1.6 trillion of outstanding debt (pre Great Recession) is now diminished to about $350 billion, mostly deployed as working capital to facilitate its mortgage backed securities business. Collectively the two agencies’ securitized pools account for about $7 trillion of the nation’s $12 trillion outstanding mortgages. State and local governments ae not significant investors in these securities. Estimated holdings are less than $20 billion.

The two federal housing agencies also hold some MBS on their balance sheets and finance this by issuing discount notes and other direct obligations. In January, the Trump administration announced a program to increase this direct purchase program by $200 billion to try to move mortgage rates lower.

This initiative should lead to a modest increase in direct issuance by the agencies and increased reliance on callable issues. Indeed, year to date through May 31 Fannie and Freddie’s combined issuance of long term direct obligations (this excludes discount notes) totaled $90.4 billion vs. $55.3 billion last year. Callables made up nearly 50% (through March 31) vs. 32% in 2025.

Callable securities offer the potential for increased income, but they also introduce uncertainty into portfolio results. There is no free lunch here and what may appear to be a benefit from an outsized initial coupon may evaporate over time.

What This Means for Public Funds Investors

Business as usual is not a bad path. The credits of Fannie Mae and Freddie Mac remain strong: they are effectively government-owned enterprises so their credit effectively is backed by Uncle Sam.

Although there is always the possibility that Trump will upend things with a social media post, as events have unfolded over the past year we’ve learned that the enormous complexity of the mortgage market and its many competing interests are strong reasons why tweets seem to have little effect on reality.

As to whether to include federal agencies in your portfolio: when they offer clear value compared with like maturity Treasuries, holding them makes sense, but (a) don’t expect much in the way of incremental yield (b) keep in mind that they may be less liquid than Treasury bills or notes and (c) when securities are callable, they have added uncertainty. Too often a look back fails to show real value from these securities.