Decoding Kevin Warsh

Twice a year the chair of the Federal Reserve testifies before Congress on monetary policy. It’s a requirement that stems from 1978 legislation that provides accountability and oversight of the independent central bank. This week’s sessions provided some insights into principal elements of monetary policy that are not ordinarily in the rate-setting headlines that monopolize investor attention around the meetings of the Federal Open Market Committee.

Kevin Warsh’s testimony shed light, if only a glimmer, on three other elements of the Fed’s mandate that go beyond setting short-term rates: how it manages its balance sheet, how it regulates financial institutions, and the extent to which financial aspiration influences monetary policy. Central bankers readily acknowledge the first two of these, but careful reading of history suggests the third—it’s long view—is the most important.

Balance sheet

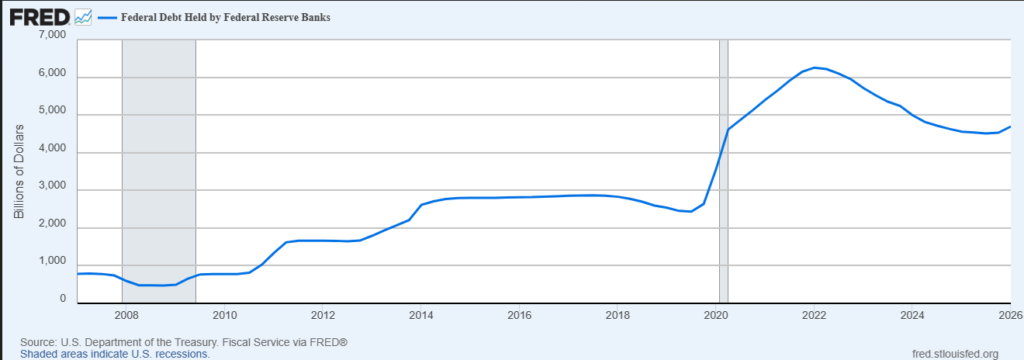

The Fed’s balance sheet and its market presence matter. One might say that the central bank IS the bond market. This is not the usual way its market role is described because to see it this way is to allow that fiscal dominance is in place. But statistics tell the story: the central bank holds $4.5 trillion of open market Treasuries, more than 10% of the total outstanding and more than any other market participant. It also underpins the repurchase agreement market which finances more than$12 trillion of debt. It’s not just the Fed’s holdings, but also the fact that it has nearly unlimited resources to deploy into the market on a moment’s notice that make it so important.

Warsh has long advocated for the Fed to reduce its balance sheet, and other Fed governors and regional bank presidents support this objective. Its Treasury holdings have been worked down from a peak of $6 trillion after the Covid-related financial stresses of 2022 to about $4 trillion in mid-2025. But recently the Fed has found it necessary to BUY Treasuries in order to avoid market disruption around the Treasury’s enormous issuance to fund the federal debt and its balance sheet has grown in the past months.

Warsh described his view as keeping the central bank out of fiscal policy, but that’s not to say he will accommodate fiscal policy—an important distinction, though one he did not make. It’s hard to see the Fed pulling back from the market when Washington seems oblivious to the ever-expanding Federal deficit, likely to be $2 trillion this year and growing to over $3 trillion in 10 years. So, expect the Fed to remain an active market participant in coming years.

That said, the Fed’s open market activities are likely to change. Warsh laid out a strategy of shortening the average maturity of Fed holdings to better align with the maturity structure of overall Treasury debt outstanding. This could mean the Fed will increase its Treasury bill holdings and perhaps sell longer bonds. For those with long memories this is Operation Twist in reverse. It will be good for short-term investors by supporting bill prices and liquidity but will put pressure up longer-tenor yields.

That’s one reason 10-year Treasuries are yielding more than 4.50% and 30-year bonds more than 5% at this writing.

Regulation

The Fed is the lead financial market regulator with responsibility to oversee banks and non-bank financial institutions. Importantly, it has control over the flow of funds, the payment system that girds the domestic and global economies. There are two broad themes here. First, the banks want to be freed from some regulatory requirements (“unnecessary burden” they would say). These stem from the near collapse of the global financial system in 2008 and the resulting recommendations of the Basel Committee on Bank Supervision.

The so-called Basel III protocols have yet to be implemented in the U.S. Warsh noted these are “recommendations” not a mandate, channeling the views of the largest U.S. banks that they would limit their ability to grow and compete in the global economy. From this one can conclude that he is likely to lean into less governance of banking practices and capital requirements.

That would be good for bank shareholders because it would release bank capital and improve shareholder returns. It may also free up capital to be used to make loans that could support economic growth. But the downside is risk and who bears the cost when mistakes are made. Lightly regulated non-bank financial institutions (Bear Stearns, Lehman, and AIG) were central to the 2008 financial crisis. Warsh, who was then a governor of the Federal Reserve, was instrumental in arranging to bail out Bear and AIG and to bring the large broker dealers under banking regulations.

Perhaps that was necessary in 2008 but has now been taken too far. Perhaps bankers and regulators have learned from past mistakes and we can avoid the next crisis while pursuing less regulation. On the other hand, history is replete with financial failures that have overcome economies and (sometimes) required strong government intervention and taxpayer resources to repair damage. Is it prudent to act as if this will not recur?

Warsh is also likely to push for opening the payments system to non-banks. The crypto and fintech players have been pressing for this on all fronts. It could result in new payment technologies that will reduce costs and improve efficiency. Big changes could be in store for businesses, state and local governments and households if this occurs. Whether these technologies will raise or reduce risks around payments remains to be seen.

The Long View

Warsh is not a fan of forward guidance, the effort by the Fed to point the path of monetary policy. Never mind that the concept originated with former Fed chair Alan Greenspan, who Warsh has cited as a model, and was refined and extended by Fed chair Ben Bernanke in response to the 2008 financial crisis, with Warsh, who was a Fed governor from 2006-2011 largely seen as Bernanke’s right hand.

What may well replace forward guidance, if Warsh has it his way, is what one might characterize as the Long View, an aspirational outlook for the course of the economy. And at the center of this would be the artificial intelligence revolution, which Warsh has described as the most consequential economic shift in generations, akin to or more impactful than the Industrial Revolution.

If the vision is fulfilled, AI will increase productivity and reduce supply and other economic frictions that feed inflation. In this outlook self-correcting elements will obviate the need for the Fed to raise rates to combat price inflation and power investors to better assess and manage risk to avoid financial panics.

It’s a bright view of the future.

When describing the massive flow of private capital into artificial intelligence Warsh commented that “They [investors] must see something shiny at the other end of the rainbow.” For some this will be a call to keep hands off and allow the aspiration to fruit. For others it harks back to Greenspan’s comment in 1996 related to the investor exuberance for inflated asset values associated with the dot-com bubble, and the laissez faire attitude of regulators a decade later that foreshadowed the 2008 financial crisis.

Time will tell.

Bottom Line

Hikes vs. cuts, hawks vs. doves and dot plots make for great streaming and social media content but are only one consequence—and perhaps not the major one—of the Fed’s activities. How it manages its massive balance sheet and regulates the financial system matter more. And over all of this, the vision of the future and confidence in realizing it are what matter most.