A Good Year for Public Funds Investors

It’s been a good year for public funds investors.

- Cash and short fixed income strategies produced their highest returns in years. With a week to go returns for the year of around 5% for the PFII LGIP indices and in the range of 4.0% for limited duration separate account portfolios (current yields are about 4.25%) should be quite satisfactory.

- The markets avoided any significant risk events. Lots of scary headlines perhaps, but it’s heartening that typical public agency investment portfolios sailed through the year unaffected.

You can access indices and other current information on the Investment Dashboard here.

Meanwhile, reflect on this question: Are interest rates higher or lower than a year ago? As economists are wont to say, “It depends.”

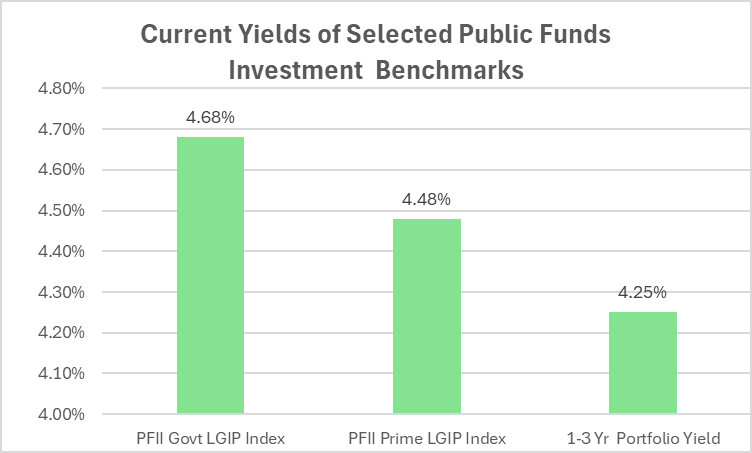

Short-term yields are significantly lower. The Federal Reserve’s policy rate is down by 100 basis points on the year. The PFII prime LGIP index is 4.68% and the government index is 4.48%, reflecting this cumulative easing. These measures still have a bit of downward movement to go because they lag the cash markets, but by historical perspective you can expect a yield in the range of 4.25% (for government funds) or 4.40% (for prime funds) in the first weeks of 2025. Limited duration separate account portfolios reflect this as well. They have returned around 4.0% for the year and their yield is likely to be in the range of 4.25% when we enter the new year.

Yes but. . . Further out the yield curve the story is a bit different. The two-year Treasury yield is now at about the same level as a year ago, while the 10-year Treasury yield is higher by nearly 70 basis points. The limited duration of most public funds portfolios protected them from market value depreciation related to higher rates on longer-duration securities.

For the first time in several years the yield curve has a positive slope, though how it achieved this position was not widely expected.

The investment grade credit markets have been quite friendly. Commercial paper, negotiable bank deposits and—further out the yield curve—corporate bonds—have added significant income without realized risk to portfolios. The low level of current risk is reflected in the cost to insure five-year investment grade bonds against default (as measured by the price of credit default swaps). The level of credit default swaps has spent most of the year below its starting point. There have been no bullets to dodge, no scary headlines to respond to. (Please do not mis-interpret this to mean there is no risk. It’s just that portfolios have gone through the year without realizing risk-related losses or market depreciation.)

And next year we’ll get to do this all over again. Rates at or around four percent—not a bad place to start. (Remember zero interest rates in 2009-2015 and 2020-2021?) As to the rest, we’ll see.

Happy holidays!