Halftime: The Score for Public Funds Investments as of June 30

The first half of 2025 has been kind to public funds investors, delivering solid returns on short-term cash and historically high returns on longer-duration separate accounts.

The first half of 2025 has been kind to public funds investors, delivering solid returns on short-term cash and historically high returns on longer-duration separate accounts.

- LGIP returns, while somewhat lower than in 2024, were close to generation highs, benefitting from the fact that the Federal Reserve has maintained an elevated federal funds rate.

- Individual portfolio strategies built on holding Treasury and high-grade corporate obligations with maturities under five years enjoyed high annualized returns fueled by falling yields on intermediate-tenor bonds.

- Dire warnings of increased market volatility generated by President Trump’s tariff policy, a fear of renewed inflation or the blooming Federal budget deficit failed to materialize or did not derail the underlying themes of market stability and a drift to lower rates.

The details.

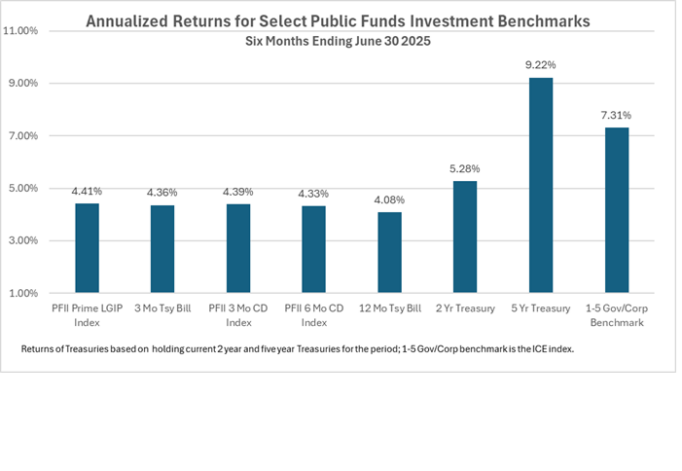

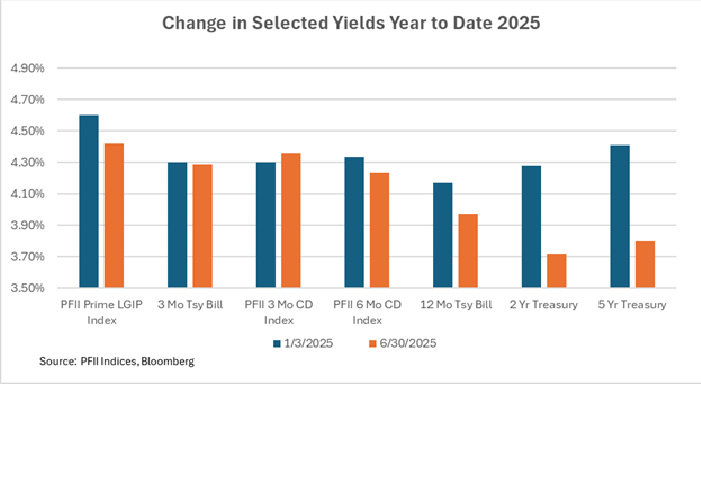

Yields and returns on LGIPs and short-term fixed rate investments are closely tied to the Fed’s monetary policy. Forward rate derivatives prices forecast a single 25 basis point reduction in the Fed funds rate in the first half of the year, but even this modest cut did not happen. As a result, LGIP yields moved in a very narrow range. The PFII Prime LGIP index began the year at 4.60%. It fell modestly through the six month period. An investment at the index rate would have produced an annualized return of 4.41% for the first half year.

Short term fixed rate investments offered yields in January that were somewhat lower than those on LGIPs, and those maturing in less than six months exposed investors to reinvestment risk during the period. As of June 30, the annualized returns were very close to those on LGIPs. For example investing at the rates of the 3 month PFII CD index would have resulted in an annualized return of 4.39% over the six month period.

Short term fixed rate investments offered yields in January that were somewhat lower than those on LGIPs, and those maturing in less than six months exposed investors to reinvestment risk during the period. As of June 30, the annualized returns were very close to those on LGIPs. For example investing at the rates of the 3 month PFII CD index would have resulted in an annualized return of 4.39% over the six month period.

This was a six-month period where reinvestment risk—or its opposite, liquidity—had very little cost or value in the short-term market. Whether an investor locked in a rate at the beginning of the year for a six-month period or maintained liquidity, the result was about the same, with the returns on three-month Treasury bills, three-month CDs, and six-month CDs all in the same range.

Not so with longer-maturities. Two year and five-year Treasury note yields fell by about 60 basis points in the half year, and investors who bought these securities locked in yields in the 4.25% to 4.40% range for the duration. On a total return basis, they would have earned 5.28% on a two-year Treasury and 9.22% on a five-year Treasury.

The bond market rally that boosted returns followed a similar rally in the second half of 2024 when yields on five-year Treasuries fell by nearly 100 basis points. (Of course, what goes up must come down and yields retraced this 2024 move between September and January 2025.) Returns, of course, move opposite yields. The return on intermediate duration benchmarks over the 12-month period was more than six percent.

One of the surprising things about the year thus far is the positive result in the investment grade corporate bond market. Investment grade corporate bonds added income and boosted returns. The return on the ICE 1-5 Year government/corporate benchmark was 7.31%. A comparable duration benchmark limited to Treasuries returned 7.17%, indicating the corporate bond allocation had the potential to add 10 to 15 basis points to a typical portfolio. (About one quarter of the benchmark we evaluated was invested in corporate obligations and this contributed the added return of 14 basis points in the six month period.)

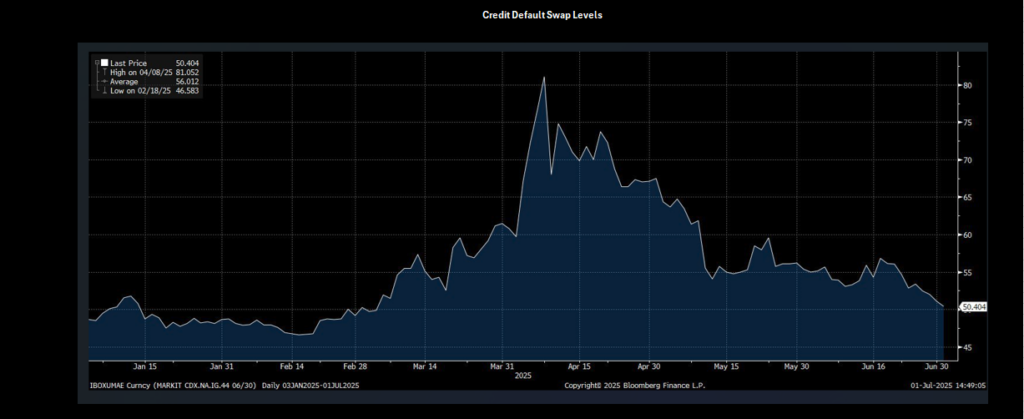

Credit spreads, represented by the level of credit default swaps shown on the above chart, are now at about the same level as they were in January, as shown in the accompanying chart of credit default swap levels. The volatility around the April tariff announcement was short-lived and investors quickly gained comfort owning credit-based bonds based on an outlook that the economy would avoid a recession in coming months.

Credit spreads, represented by the level of credit default swaps shown on the above chart, are now at about the same level as they were in January, as shown in the accompanying chart of credit default swap levels. The volatility around the April tariff announcement was short-lived and investors quickly gained comfort owning credit-based bonds based on an outlook that the economy would avoid a recession in coming months.

What’s Next?

Bond investors foresee lower rates ahead, at least for short and intermediate tenor bonds. This is despite warnings from the sidelines about the possibility of tariff-fueled inflation and worries about the level of Federal debt that overhangs the markets.

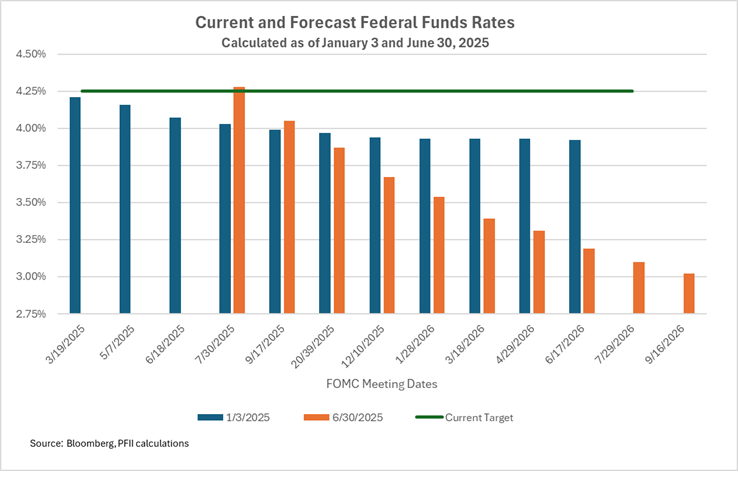

Here is how futures prices forecast the level of rates now, compared with January 2025:

Where the early-year forecast was for federal funds to be at 3.90% by year-end, the current forecast is for the main policy rate to be at about 3.50%. Softening business activity and unrelenting pressure from Trump seem to have had their impact: The Fed likely will resume its rate-cutting unless there is a nearby surge in inflation.

Where the early-year forecast was for federal funds to be at 3.90% by year-end, the current forecast is for the main policy rate to be at about 3.50%. Softening business activity and unrelenting pressure from Trump seem to have had their impact: The Fed likely will resume its rate-cutting unless there is a nearby surge in inflation.

The ultimate resting point for federal funds is likely to be around 3%. Indeed, that is the forecast in the Summary of Economic Projections produced by the central bank after its June meeting.

The risk of recession could push short-term rates sharply lower—perhaps to the one percent level. The Federal Reserve’s own measure marks the risk at about 15%, while economists surveyed by Bloomberg place the level at a bit less than 40%.

The more likely path for the economy is for sluggish growth and inflation that sticks above the Fed’s two percent goal for the next year or two. This suggests that interest rates in the segment of the market where public funds are invested will have a three handle on them in coming quarters.

If something breaks of course rates could plunge. Or the overhang of growing Treasury debt and a weakening dollar that depresses foreign demand for Treasuries could pressure long-term rates higher. But portfolios invested in bonds that mature within the next several years should be somewhat insulated from these moves.