Research Note: Commercial Paper Market Should be More Resilient After Money Fund Reforms

Commercial paper is a core holding of many state and local government investment portfolios. It provides a yield boost to separately managed portfolios and prime-based local government investment pools. The commercial paper market is a bit finicky: If you are a buyer there is little flex: you generally receive the rate posted by issuers. If you are a seller, the bids are quite variable and may be nonexistent with the slightest evidence of market stress. In short, we might characterize it as a one-way market, offering a yield premium to buyers on the way in, but offering limited liquidity for those who might want to sell holdings prior to maturity.

Commercial paper buyers (and issuers) have been paying attention to developments in the prime money market arena because in the recent past prime funds have been a major force affecting the CP market. Institutional prime funds effectively froze the CP market in the spring of 2020 when they sold CP to meet Covid-inspired shareholder redemptions, and prudential regulators undertook after-action studies to try to figure out how to make the market more resilient. They settled on a new liquidity fee that would be assessed on institutional prime fund investors who acted precipitously to redeem shares. The new liquidity fee rule, adopted by the Securities and Exchange Commission in 2023, was effective on October 2, 2024.

The rule and related changes in prime fund portfolio holdings appear to have made the market more resilient than it was four years ago.

At a high level:

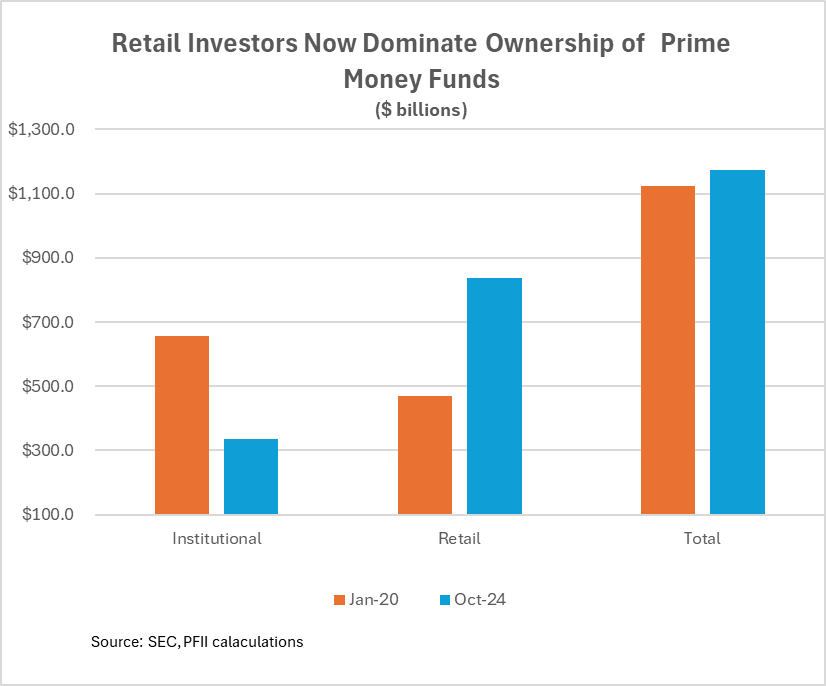

- Today institutional investor prime fund investors hold a notably smaller share of overall prime fund assets than they did as recently as the beginning of 2024. In the months before the rule’s effective date their assets declined from about $656 billion in January 2024 to $337 billion in October.

- The decline in institutional prime assets has been offset by an increase in retail prime assets. They gained $121 billion in this period (and more over the longer period since 2020) and now make up 70% of prime fund assets. Retail shareholdings are likely less volatile than those of institutional investors.

- The change in the share balance between institutional and retail prime fund shareholders should make the CP market less susceptible to the behavior of prime money market funds in the future.

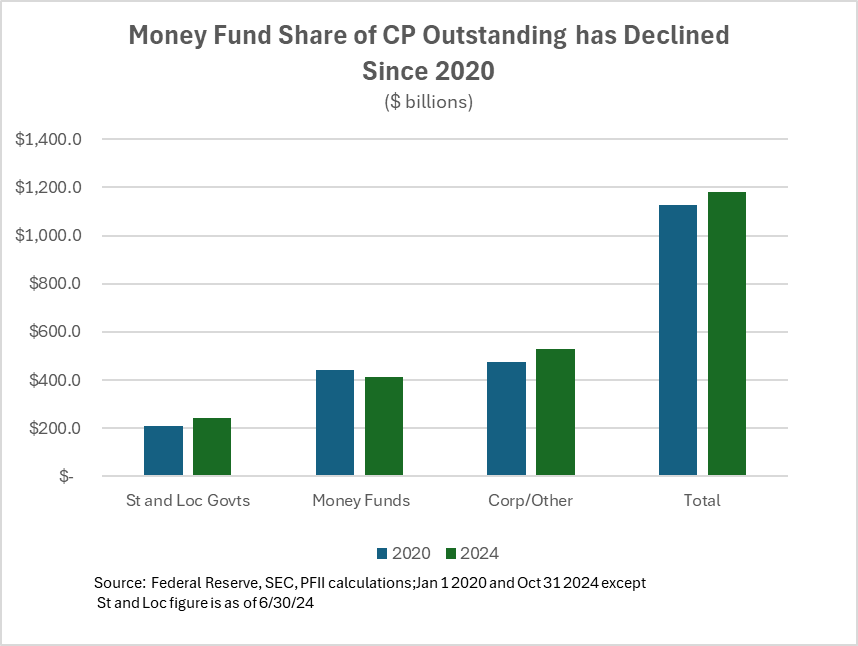

- Prime money funds held $412 billion in commercial paper at the end of October. This was $29 billion less than holdings on January 1, 2020, immediately prior to the Covid freeze, and represented a decline in market share from 39% to 35% (in October). This too should improve resilience because other holders (state and local governments and corporate bodies) are more likely to hold CP securities to maturity.

- Commercial paper yield spreads widened modestly in October. Spread widening was predicted by some market commentators in the months preceding the rule’s effective date. But the difference in yields in favor of commercial paper (by five to basis points recently) is well within levels that we’ve observed over long periods. It’s not clear whether the difference is a result of the new liquidity penalty rule or other factors. Nevertheless, the modest widening is not likely to change issuer or buyer behavior.

- The changes in the marketplace are unlikely to change CP market liquidity, which is still iffy in periods of market stress. Buyers of CP should not count on being able to liquidate it prior to maturity, particularly if the liquidation were to be required by macro conditions like an economic downturn or interruption of tax or other government funding.

The Longer View

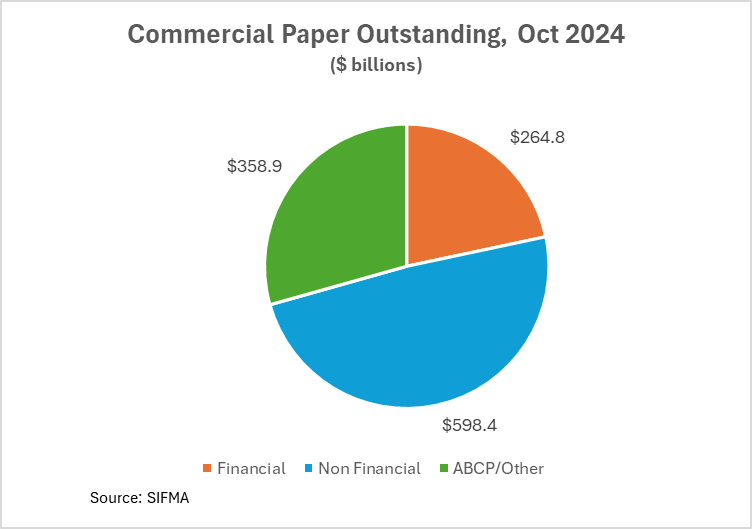

The CP market is about the same size today as it was in 2020, with outstandings of about $1.2 trillion. Issuance is heavily concentrated: financial issuers (and sponsors of asset backed CP) represent 78% of outstanding paper. These issuers are closely supervised by prudential regulators and many of them are effectively too big to fail, so that adds a level of protection, but it also means that portfolio diversification opportunities are limited.

Other money market segments have expanded significantly in the past four years—Treasury bills outstanding have nearly doubled in volume to $6.5 trillion—so today CP is a much smaller segment of the money market space.

Commercial paper held by state and local government has grown modestly in this period, offsetting a decline in money fund holdings. Public agencies held about $240 billion as of June 30, 2024. We estimate that roughly $150 billion is held by state and/or local sponsored LGIPs. The balance is in separately managed portfolios, largely concentrated among states and larger local governments.

The change in relative holdings is a positive for market stability. Corporate holders likely buy and hold CP, and their holdings are not likely to be impacted by unforeseen liquidity demands from third parties. Similarly, the decline in the share of CP held by money funds is a positive because a run on these funds in 2020 precipitated the market freeze. CP held in LGIPs could be subject to runs, but history tells us that LGIPs did not experience runs in either 2008 or 2020.

Prime money funds are now largely a vehicle for retail investors, a dramatic shift from 2020. While the overall size of prime funds is about the same now as it was in January 2020, institutional shareholders hold less than 30% of the assets. The shift in prime money fund assets from institutional to retail investors (see accompanying chart) is notable and should mean greater resilience for financial markets. These investors are more likely to demand liquidity in times of stress, and also involve investment portals in their decisions. Portals can facilitate mass redemptions. Retail investors who invest in prime funds are doing so through retail brokers, where decision-making is highly distributed.

Spreads between CP yields and those of comparable-maturity government securities are not notably wide. In the months prior to October some market commentators suggested that CP yield spreads could move wider because of changing demands related to the liquidity fee rule.

The accompanying table shows the history of spreads for 90-day investments at various time periods between 2020 and now.

Over the entire period they averaged 13.3 basis points. They were actually negative at some points, particularly early this year, but the averages for 2024 year to date and since October do not show unusual dimension. The reason may be that overall prime fund holdings of commercial paper, at $441 billion in October, are close to the levels held at the beginning of 2024 and in January 2020. In other words, money funds remain a consistent holder of CP, with the decline in the holdings of institutional portfolios offset by increases in holdings in retail funds.

Bottom line. If you take a long view of the underlying CP market today it appears to have a stronger investor base—a positive for issuers and good news for public agencies that invest in short-term credit instruments, either directly or through local government investment pools where CP and CDs are utilized to boost returns and may make up to 70-80% of some portfolios.