An Update on Credit

In November we wrote about cracks appearing in credit, cautioning investors that emerging risks could expose corporate bonds and commercial paper to losses and drag down returns of portfolios that hold them. Six months later the cracks have not expanded. Nor have they healed. But risk premiums for both investment grade and high yield credit have declined, and the sectors have out-performed comparable Treasury benchmarks,

In November we wrote about cracks appearing in credit, cautioning investors that emerging risks could expose corporate bonds and commercial paper to losses and drag down returns of portfolios that hold them. Six months later the cracks have not expanded. Nor have they healed. But risk premiums for both investment grade and high yield credit have declined, and the sectors have out-performed comparable Treasury benchmarks,

- Investors have discounted the warnings, seemingly persuaded by forces that have led to the powerful stock market performance. The premium offered by credit-based investments in many cases has declined, with investors satisfied to invest in corporate credit instruments with lower compensation for risk.

- The positive returns on corporate bonds this year, when compared to Treasuries, came despite the never-ending headlines about inflation, economic dislocation, and rising interest rates.

- High yield bond returns have exceeded those of investment grade counterparts. This segment of the market, which often provides an early warning of troubles ahead, is signaling green.

- For public funds investors who hold credit instruments in their portfolios this is good news, but it should not be taken as a reason for complacency because some of the key underlying fundamentals that support credit have continued to weaken in the past six months. The out-performance of risk-on investments also means that investors who buy or hold corporate credit today will receive less compensation for taking risks than six months ago.

Deep Dive

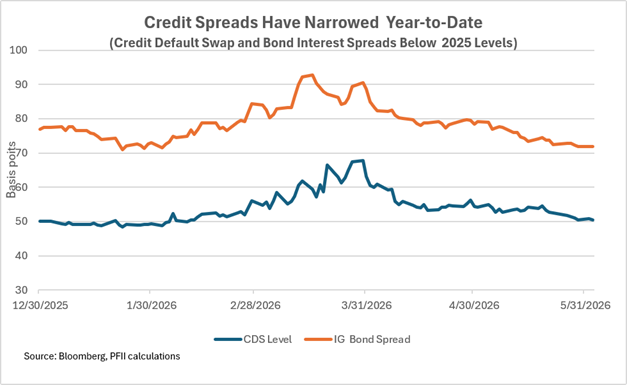

The November Beyond the News post, called out narrow spreads between corporate bond and Treasury yields and the low level of credit default swaps (a form of insurance against defaults). The accompanying chart shows this.

The spread offered by investment grade corporate bonds was about 80 basis points in November. And the cost of a credit default swap with a five-year tenor was about 53 basis points. These are both lower now—71 basis points and 50 basis points at this writing. And they are notably lower than the five year averages. The bond spread averaged 102 basis points over the term.

A consequence of the shrinking spreads is that corporate bond holdings have produced higher returns than those of comparable Treasuries, A benchmark of AAA-A rated corporate bonds with maturities of one to three years returned 0.85%in the five months ending in May. (The annualized return was 2.14%,)This compares with a periodic return of 0.54% for a comparable benchmark of Treasuries. The excess came from both the higher average coupon on the corporate bonds and the narrowing spread over the period. The yield to maturity of the corporate bond benchmark was 4.08% at the start of the year, compared to 3.51% for the Treasury benchmark, so corporate bonds would earn 57 basis points of added income over their lives. The spread narrowed to 47 basis points at the end of May and corporate bond holdings received the benefit of this modest price appreciation as well. (This analysis is based on the ICE BofA Treasury and corporate bond 1-3 year indices.)

High yield bond returns followed this theme. Public funds investors rarely hold these securities, but their performance provides an early signal of credit market distress. Yet benchmark returns for junk bonds exceeded those of Treasuries and investment grade bonds, benefitting from both higher yields to maturity and shrinking spreads.

Cracks in Credit, But . . .

The cracks in credit that we observed in November remain. But so does the overwhelming force of a strong stock market performance fueled by solid corporate earnings and exuberance over the potential for artificial intelligence.

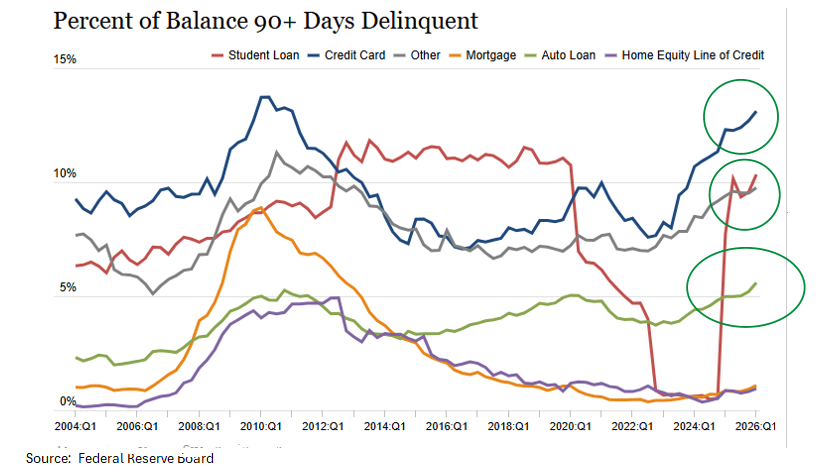

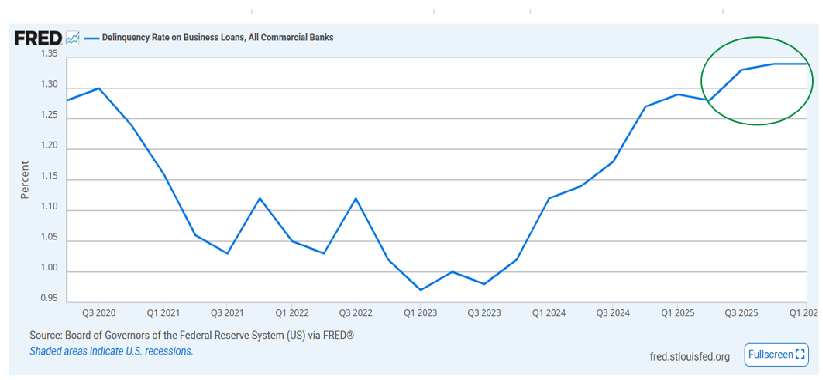

Some key credit indicators remain worrisome. Business and consumer loan delinquencies, elevated when we posted in November, are more stressed today.

Consumers are under pressure because prices have resumed climbing faster than incomes. Consumer spending has weakened, even as consumers have reduced their personal savings rate to maintain it.

It’s not just bond investors who have discounted worrisome loan payment trends and stressed consumers. The Federal Reserve conducts a quarterly survey of senior loan officers at banks and the most recent result, released last month, showed unchanged or easier lending standards across almost all types of loans. This is despite an elevated level of business loan delinquencies.

But the credit markets seem to have downplayed these signs, looking instead to factors that have supported the strong performance of equities.

Equity investors, who seemingly cannot have enough of artificial intelligence-related stocks, have pushed the more speculative indices to out-perform.

At this writing, the S%P 500 Index is up about 11% year to date while the NASDAQ is up about 16% percent and the Dow Jones Index is up 6%.

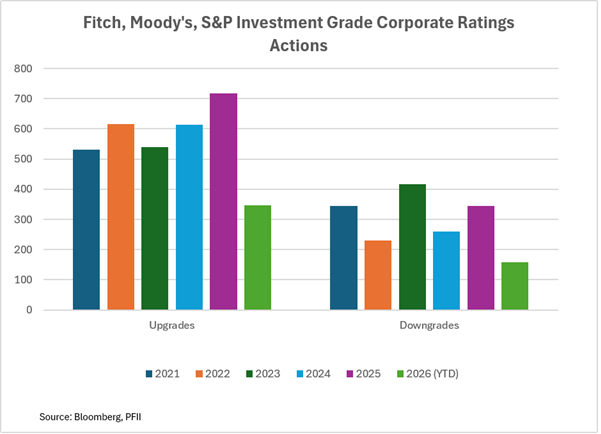

Also, ratings agencies continue to upgrade more credits than they downgrade.

The accompanying chart shows the trend, which includes actions through the end of May. While each rating action stems from an analysis of the particulars of a corporate credit the overall trend supports investors taking risk for historically lean risk premiums.

“New” thinking provides some basis for those who have set aside the “irrational exuberance” warnings issued by some well-known investors. A study recently released by the Federal Reserve Bank of Minneapolis focuses on the free cash flow that corporations generate, rather than the somewhat narrower metric of earnings. It concludes that equity prices, viewed as when when compared with earnings, are not inflated when compared with free cash flow.

What applies to equities could also be applied to bonds because bondholders ultimately look to cash flow for payment of the obligations they hold.

Bottom Line

It’s remarkable that investors continue to purchase commercial paper and corporate bonds at current levels. True the economy is expanding, though at a modest pace, and inflation will make it easier for borrowers to repay obligations, using inflated currency to do so.

It seems as if the dancing will continue until the music stops.