Research Note: The R Word

This is a wonky post, and I hope it is not out of reach to some readers, but I think it’s important to provide context to the current market.

Sentiment in the bond market has undergone a subtle shift in the past couple of weeks with some investors now expecting a slowing economy. And even the thought of a recession is out there. Not that a sharp downturn seems imminent, but the bond markets are undergoing a change from the euphoria of a month ago. Recession? Not likely at this point but risks are rising.

Consider this:

-

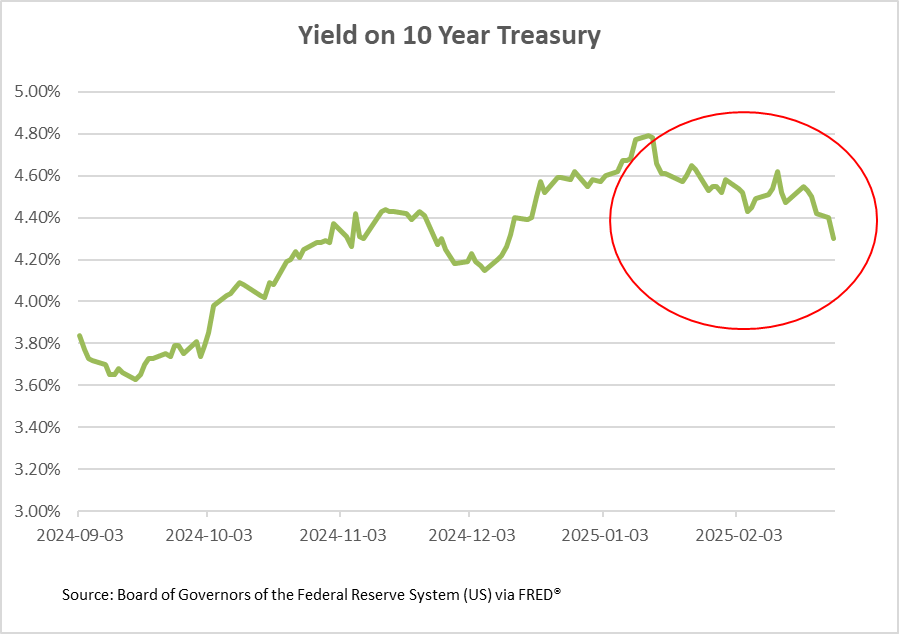

- Long term Treasuries have rallied from a yield of 4.80% in mid-January to 4.30% at this writing. (See above chart.) This while mid-term inflation expectations, as represented by the University of Michigan survey of consumer expectations for inflation over the next 5-10 years, rose to 3.50%–its highest level since the 1990s. Normally a revision of the outlook for inflation pushes long-term rates higher, not lower.

-

- Treasury is planning to issue at least $4 trillion of new debt over the next several years to fund an extension of the 2017 tax cuts and Federal spending. This is the amount of debt ceiling expansion that is in the budget reconciliation package passed by the House of Representatives. Trump administration policies may or may not stimulate growth in the medium and long term—there are arguments on both sides of this—yet over the short term (next 12-24 months) fiscal policies are likely to be a drag on growth.

-

- The activities of the “move fast and break things” effort in Washington may or may not be successful over the long term in improving government and private sector efficiency, boosting economic growth and taming inflation. Time will tell. But over the short term it is hard to see how they will not cause some disruption of economic activities, creating supply chain kinks and uncertainty throughout the economy that do not seem to be reflected in the market outlook.

What is surprising is that the economic forecasts tracked by Bloomberg have not changed in months. The most recent survey of 91 economists published last week is for growth to slow gradually from the fourth quarter level of 2.3% to 2.0% in 2026 and unemployment to rise modestly in 2026 and 2027 from its current 4% level.

Consumer level inflation (CPI) is forecast to remain elevated, declining only to 2.4% in 2027. This outlook is little changed from that in December 2024. The probability of recession forecast recently ticked up a bit from 20% at the end of 20234 to 25%, but this is far from the level of 65% estimated at the end of 2022 and start of 2023 when an economic hard landing was the consensus

Drill down. Are economists missing the boat? Or did the models they ran in December comprehend the recent developments in Washington that have significant economic implications? The headlines are filled with stories on major tax and spending policies, the imposition of worldwide tariffs (with possible retaliation), a reordering of the world political order, the shuttering of many Federal programs (which, depending on your view will either hamper the economy or free it for phenomenal growth). Yet the response from market economists seems to be “yeh.”

To be sure, as much as many investors hang on the words of market economists, forecasters do not have a stellar record of forecasting. Their words make for good conversations with a glass of something in your hand, but bet real money on their outlooks? Maybe not.

And this conclusion should not be a surprise to forecasters. In September The economic research arm of the New York Fed published a blog post that pointed out the limitations of professional forecasters efforts in recent years.

That’s not to say forecasts are of no use to portfolio managers. Their economic models contain some very useful insights into what drives economic activity and provides signals to the financial markets. (Whether financial markets respond consistently to these signals or discount/ignore them to focus on other factors is another story entirely.)

Most of the professional forecasting models are in a black box, but one of them, offered by Bloomberg economics, is a useful tool for those who can afford a Bloomberg terminal license. Not that the ultimate result will be accurate. This I do not know. But the model does allow one to get a sense of how growth drivers interact with each other and the timing of when they might impact the markets.

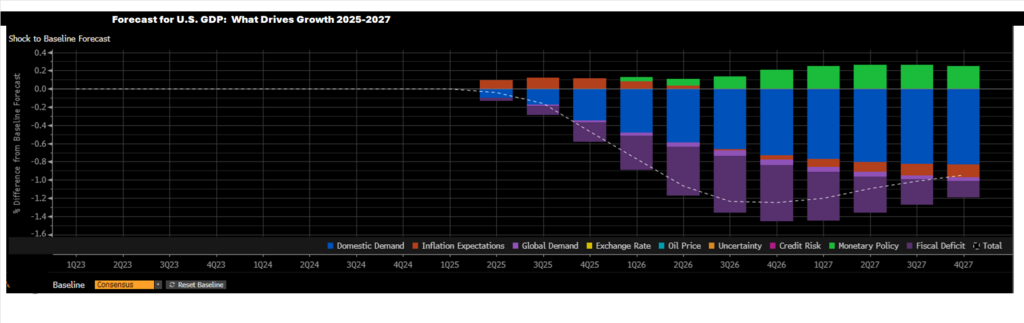

To see how the evolving Federal tax, tariff and spending policies might affect the outlook for growth that may not be captured in current economic forecasts, I ran a scenario that is summarized in the accompanying chart. It represents the impact by quarter on GDP growth of changes in the input assumptions related to consumption, inflation, monetary policy, and fiscal deficit.

From a baseline of GDP expanding by about 2% a year, I made some assumptions that consumption would slow a bit from the current trend, fiscal policies would become somewhat less stimulative, and the Fed would accelerate its easing to offset slowing growth.

The bars on the below chart represent the effect that these assumptions have on the outlook for growth particularly on the relative weights (the biggest drivers are consumption(the blue bar) and fiscal policy (the purple bar). Fed policy (green bar) would not be sufficient to offset these). Note also the timing of impact: Fed policy has lagged effects; inflation expectations (orange bar) affect both current and future quarterly growth.

Source: Bloomberg Economics, PFII calculations.

Here are a few observations from the effort:

-

- In total the assumptions would reduce GDP growth to less than 1% mid-2026. Key drivers would be consumer behavior and fiscal policy. So, much lower growth but no recession.

-

- The biggest component of GDP is consumption, which represents about 70% of the total. It should be no surprise that consumer reaction to the tax, spending, tariff and restructuring moves of the Trump administration will be really important. The path for the economy, at least in the next several years, is likely to be heavily influenced by consumer behavior. Even a small pullback in consumption would result in a period of sub 2% growth.

-

- Global demand is not a big factor in U.S. GDP, as it contributes only about 12% to the total. Thus, retaliatory tariffs or a decline in the non-US economy would have only a modest effect on GDP.

-

- Higher inflation expectations would boost growth in the next several quarters as consumers accelerate purchases, then reduce growth in later periods. We’ve already seen some of this and there could be more to come.

-

- A modest decline in the Federal fiscal deficit would reduce growth by as much as 0.5% of GDP. Reducing the deficit will have a negative effect on GDP in the short run. Not something that has been widely recognized.

-

- Fed policy would not be sufficient to offset a slowdown in consumption and less expansive fiscal policy. The analysis assumes Federal funds are at a level of about 3% by the end of next year, but even an aggressive move to reduce this to 2% would not come close to offsetting other factors.

-

- This scenario is not enough to push the economy into recession, but it is still notable that growth could decline to about 1% and the unemployment rate would rise to 4.7%.

The bottom line. Any slowdown in the pace of growth has implications for state and local government revenue and spending. Beyond that, it is instructive that this model forecasts little change in interest rates other than the Fed’s policy rate, which would fall to 3.5% next year and then 3%. The outlook for the 10-year Treasury yield, both in the consensus forecast that Bloomberg tracks, and in the more pessimistic scenario that I described above, is nearly the same in 2027 as it is today. There is a different drummer to which long term rates respond.