Treasuries: Ya Gotta Love Em

Treasuries are the rarest of birds and also the most common. Rare because they are universally accepted as a safe haven for investment, and the most common because they are in abundant supply. If you don’t like them as they are, well then, the price will go down. And don’t worry about supply: you can buy all you want today, and there will be more in coming months/years.

For public funds investors this is good. Treasuries make up about 40% of public sector investment holdings according to the Federal Reserve, and their presence has grown steadily over the past five years. And for good reasons. They are essentially risk free. In the investment horizon of most public sector portfolios, you can buy a Treasury that matures within several days of any desired cash flow requirement. They pay a market rate of interest—these days between 4.00% and 4.25%. They are highly liquid. You can buy a three-month Treasury bill today and, if you change your mind or need to liquidate it tomorrow, you can do so at a cost of $15 to $20 per million! The bid/offered spread is less than the cost of a couple of Happy Meals. (That doesn’t account for changes in value related to changes in interest rates, but still, this is remarkable.)

And Treasury yields are currently within ten to 20 basis points of yields on high grade commercial paper, an alternative for some public sector investors. That difference represented a big yield pick-up when short term rates were at 20 basis points in 2021, but with yields at current levels the pick-up in income is quite modest.

Treasury’s debt management plans, at least for the foreseeable future, fit well with the goals and strategies of most public funds investors. The Federal deficit is currently estimated at $1.9 trillion for FY 2025, about $100 billion more than last year, so in total Treasury’s borrowing will not differ greatly from 2024. While the Trump administration has proposed large cuts in spending, these are unlikely to affect spending or borrowing for 2025.

About 34% of Treasury debt matures in one year or less, and about 54% matures in under three years, according to a recent Treasury release. So, there is a lot to choose from—nearly $15 trillion maturing on or before January 31,2028.

Want to match cash flows? There are 70 different Treasury bill maturities in the next 12 months and also 50 note/bond maturities in this span. There are about another 50 maturities in the one-to-two-year time period.

Treasury bill issuance has grown by more than 60% in the past four years, as the surge in Federal spending and effect of lower tax rates have grown the Federal deficit. You can count on new bills to be issued on a weekly basis with regular maturities out to six months and on a monthly basis with a maturity of one year.

Treasury issues bills in part to manage the overall maturity of its outstanding debt, but the major drivers of volume and timing in recent years have been Treasury’s seasonal needs for cash. Thus, it ramps up issuance to account for the uneven seasonal flow of revenue. This year it plans to issue $364 billion this quarter, then pay down $382 billion in the April-June period after it receives tax payments due April 15.

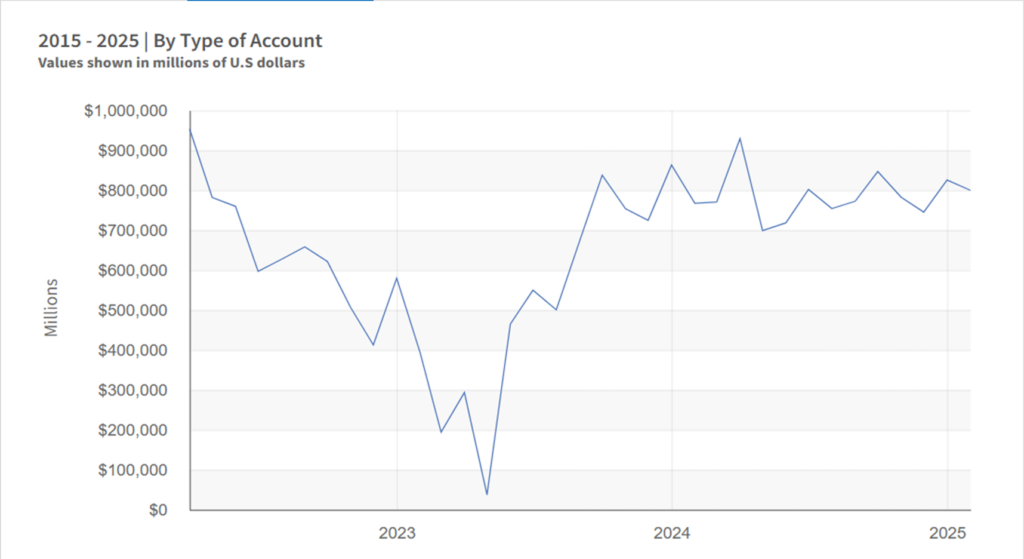

In recent years, the Treasury has maintained a cash balance of around $800 billion. (See below chart.) Changes in this balance will have a direct effect on the volume of bills issued.

Treasury Cash Balance

During the presidential campaign Trump, and his now Treasury secretary Scott Bessent, criticized the Biden Treasury for over-reliance on short-term Treasuries to fund the government, but earlier this week, with the Trump administration now in charge, the Treasury announced plans for borrowing for the next two quarters that maintain the recent historic balance between short and long term borrowing, so perhaps the issue is not so pressing, or maybe not an issue after all.

Failure to extend the debt ceiling could interrupt Treasury’s plans and disrupt the bill market. In May 2023, when the government came perilously close to running out of cash, Treasury ran its cash balance down to under $100 billion (chump change!) and investors shied away from maturities that were close to the date when Treasury might run out of cash and be unable to roll-over its bills.

We now have another debt ceiling drama nearly upon us. In this cycle the government could run out of cash in the June/July time frame if the debt ceiling is not raised or eliminated. Bill prices for June and July maturities could fall (and yields rise) by 25 to 50 basis points if we get close to June without resolution.

Money funds are the biggest buyers of short-term Treasuries, and their presence dominates the markets. This is not a bad thing because they provide a continuing source of demand and liquidity, but money funds that seek to maintain a constant net asset value will avoid holding bills maturing around the zero cash date so there could be some market disruption later this spring.

We noted Treasury’s strong reliance on the short-term markets (dominated by Treasury bills) for funding, but fixed income investors, other than money market fund managers, state and local governments or corporate cash managers are largely focused on Treasury’s plans to issue notes and bonds that mature in two to 30 years. It is here that Treasuries compete directly with corporate bonds and the rates on fixed rate home mortgages and other medium and long term obligations.

For these longer-term investors Treasury’s just-announced plans to borrow this quarter and the next were somewhat reassuring. Its plans to auction notes and bonds are unchanged from amounts issued in the past two quarters. They total $233 billion of two-to-five-year debt this quarter and $224 billion in the April-June period. This will favor short-term investors including public funds managers—more supply-à cheaper prices and greater liquidity.

The borrowing forecast should help to stabilize the long-term market. So will recent comments by Treasury secretary Bessent that the Trump administration recognizes the importance of reducing the yield on the 10-year Treasury as a way to reduce corporate bond and home mortgage rates. Bessent’s comments acknowledged that the Federal Reserve’s monetary policy would have less impact on this segment of the market. So perhaps Jerome Powell and his Fed colleagues will escape Trump’s ire for a bit.

Short term Treasury bill rates are closely tied to the Fed’s monetary policy, especially the level of its main policy rate and its actions to manage the size of its balance sheet.

The current outlook for two cuts in the Federal Funds rate this year is a major reason six-month Treasury rates are around 4.15%- and one-year rates are around 4.00%. With the current Federal Funds target rate in the range of 4.25%-4.50% the rate on one-year Treasury bills is consistent with a policy rate in the 3.75% to 4.00% range by year-end.

Meanwhile the Fed is in the latter stages of reversing the quantitative easing program that it initiated in 2020 to respond to the pandemic. When the Fed ends its quantitative tightening program, widely expected in the third or fourth calendar quarters of the year, it will step away as a buyer of Treasuries. The Treasury’s quarterly refunding analysis showed it expected purchases by the Federal Reserve would total between $170 billion and $270 billion this fiscal year, so ultimately this will have to be absorbed by the public markets.

The Fed reports currently holding only about $195 billion of Treasury bills, so the pace at which it unwinds its position should have only a modest effect on Treasury bill rates. (Recall the biggest buyers are money market funds with nearly $5.6 trillion).

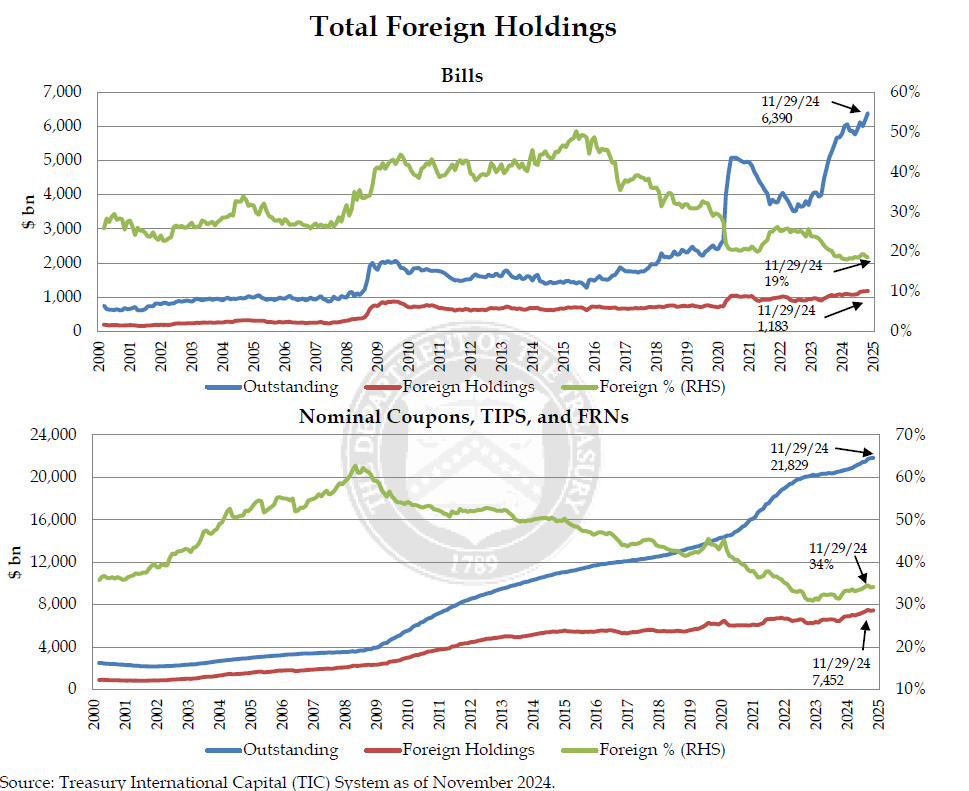

A final factor is holdings by foreign buyers. The percentage of Treasury debt held by foreign accounts has declined steadily for at least a decade as incremental issuance of bills, notes and bonds has been absorbed by domestic issuers. Holdings have not declined, it’s just that supply has grown, and these buyers have not kept pace. The accompanying chart from the Treasury’s report to the Treasury Borrowing Advisory Committee this week documented this trend.

The TBAC showed that foreign accounts own about 19% of outstanding Bills. They have a bigger impact on the longer- maturities where they own 34% as of Nov 29, 2024. Global trade or political tensions could roil the markets, but there has been little evidence of this so far.

Bottom line: It’s for good reasons that value in the short term fixed income market is measured against Treasury benchmarks. Years ago—back in 2000 or so, to be exact—the Federal government ran a modest budget surplus, and some folks began wondering or worrying about what would replace Treasuries if new issuance ceased. For better or worse, that worry seems farfetched today.