A Bond Fund that Isn’t

If you ask a local government investor what additional offering they might use, they often respond that it would be a fund that invests in longer-maturity investments but allows them to redeem their shares at par whenever they want. Anyone who has taken Investments 101 knows that this is (usually) an impossibility. Investing beyond the very short-term introduces price volatility. When interest rates rise the market value of a fixed income portfolio declines and if you allow investors to exit at par you are asking for trouble. (The result of falling rates would be less painful but still a problem.)

If you ask a local government investor what additional offering they might use, they often respond that it would be a fund that invests in longer-maturity investments but allows them to redeem their shares at par whenever they want. Anyone who has taken Investments 101 knows that this is (usually) an impossibility. Investing beyond the very short-term introduces price volatility. When interest rates rise the market value of a fixed income portfolio declines and if you allow investors to exit at par you are asking for trouble. (The result of falling rates would be less painful but still a problem.)

Indeed, since the 1970s the Securities and Exchange Commission has had rules around what are called stable asset value funds to try to prevent trouble. The Commission strengthened the rules after the 2008 Great Recession and again after the 2020 Covid-related market panic—both times when stable asset value money funds were stressed—to seek to reduce the risk. These days most observers would agree that the rules limiting weighted average maturity to 60 days, requiring that portfolio investments be limited to government obligations or otherwise be diversified, and requiring that where there is a cost to creating liquidity for redemptions the cost be passed on to investors who redeem shares, will be effective in protecting investors in the event of a market disruption.

If someone came along and offered you a fund that sought to invest beyond 60 days—say with a weighted average maturity of nine months or a year—and offered investors the ability to invest at a dollar and redeem at the same price if interest rates rose (or fell) after their investment, those who passed Investments 101 likely would give thumbs down. If the portfolio were invested for 270 days on average and rates rose by one percent after it was bought the portfolio would depreciate in value by about 0.75%. An investor who redeemed at par would leave this loss behind for those investors who remained. And, with the fund’s investor base now smaller (because of the exiting investor) the loss would be magnified.

If you are a proper fund and your plan was to invest out beyond 60 days on average you would register as a bond fund and offer and redeem shares at a floating net asset value to treat all investors fairly—and to stay out of the clutches of the SEC. If you were a fraudster, you should have a satchel of passports and a lot of crypto in your wallet and be prepared to disappear when Uncle Sam or aggrieved shareholders came calling.

Local government investment pools are not subject to the SEC’s rules regarding stable net asset value funds, but they and their sponsors/managers are subject to the SEC’s anti-fraud rules. Presumably, this provides some protection for public sector investors (this is not legal advice), although hopefully the fund sponsor and manager would adhere to fair dealing practices even without the threat of fines and jail.

So, for the most part LGIPs that seek to offer longer-maturity investments either do so for fixed terms or they offer and redeem shares at a floating net asset value. A number of LGIPs offer these types of short-term bond funds.

But suppose a government with an existing portfolio offered you the chance to “ride along” with its investment strategy for free—that is without requiring that if/when you redeem funds your principal would be adjusted for unrealized portfolio losses (or gains). If the sponsor/manager were sophisticated it might limit the amount you could invest so you did not significantly dilute its investment results or burden the fund with your purchase/redemption activities.

If this portfolio had a “risk adverse” investment strategy of placing most funds to meet the expected cash flows of the sponsoring investor over a one to two year period, investing the majority of funds in government obligations, and avoiding leverage, this might be a pretty good opportunity for the free-rider. And as long as the free riders in total held only a minor portion of the fund their involvement would not detract materially from the strategy of the sponsor.

Of course, because of its longer weighted average maturity this fund’s income-based yield would lag that of a stable value fund—a good thing when rates fall, not so good when rates rise. You could either ride along for the long haul, taking the good with the not so good, or move money in and out to improve income. One could argue that this “arbitrage” advantages you over the fund’s main investor—let’s call it a large state. But the main investor might be fine with that under the limits it imposed: restricting the maximum account balance, the number of transactions you could do, and so forth.

There are a couple of risks in this strategy. (All investing entails risk.) The sponsor in effect has agreed to put up most of the equity as a buffer against loss. The fund could have unrealized losses (and gains) from time to time that are material, but these would be allocated largely to the majority investor because your share and the share of other minority investors would be very small.

There is also the risk that an investment could become impaired. As long as the sponsor maintained 70%-80% of the fund’s equity, invested most of the funds in government obligations, did not use leverage, and limited its credit investments to those with high quality, the amount of loss you might experience from an impairment would be quite small. If the fund were a large one—let’s say $100 billion—and your investment was $50 million, your share would be five basis points of the fund’s total. If you have the inclination, you can quickly do a back of the envelope calculation of the magnitude of potential effects of an impairment of a credit holding on the $50 million investor. It’s generally a fraction of expected annual income and likely much smaller than the cost of an impairment on the same $50 million invested in a smaller LGIP that has a larger portion of its assets invested in credit.

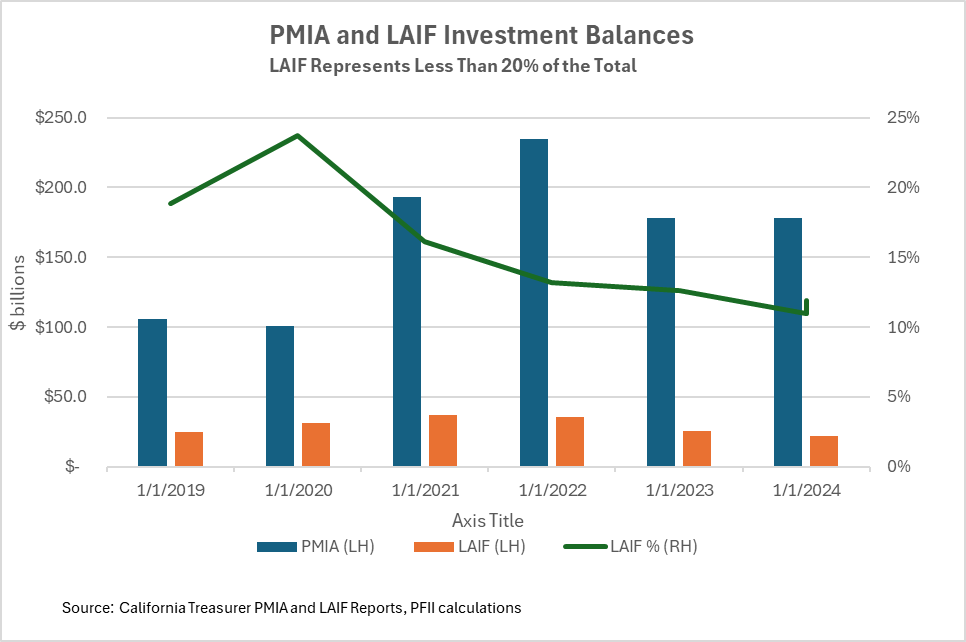

The most likely venue for a bond fund that isn’t is a state-sponsored LGIP. A number of states sponsor LGIPs and put up a portion of the state’s investment assets to invest in the fund. The largest by far is the California Local Agency Investment Fund that currently has about $22 billion in assets from local agencies invested along with approximately $140 billion of state money in the Pooled Money Investment Account. The size of the overall program and the fact that the state’s assets represent 80% or so of the total set it apart from some others.

From time to time someone will question the viability of propriety of LAIF. At one point in its history some local agency officials raised concerns that the state might impound their assets to deal with a state budget deficit, though state law prohibits this. When interest rates rise sharply, as they did beginning in 2022 some observers may warn of a “run” on the fund as investors draw down money to invest at higher yields in the cash market. Indeed LAIF’ assets declined from $37 billion in June 2021 to $26 billion in June 2023 to $21 billion at the end of 2024. These are large amounts, but the drawdown, spread over two years, cumulated only 7-8% of the PMIA’s total assets, and the PMIA’ investment strategy appeared to accommodate this without stress.

LAIF is an unusual investment vehicle, but that does not mean it is a bad investment. It’s operating model may be hard to duplicate but it has offered value for its investors over nearly 50 years.

Coda: I began thinking about this theme of a bond fund that isn’t after I listened to the annual webinar that the California Local Agency Investment Fund conducts for its investors. LAIF has been in existence since 1977 and from time to time it has come under criticism because it is managed beyond the investment limits that ordinarily apply to stable value funds but offers a dollar-in dollar-out. But as long as the state maintains 70%-80% of the fund’s equity, invests largely to match its expected cash flow needs and has a low-risk portfolio, from the perspective of the local agencies who get to free-ride it offers many of the advantages of a short-term bond fund without a mark to market valuation that is often puts-off investors.

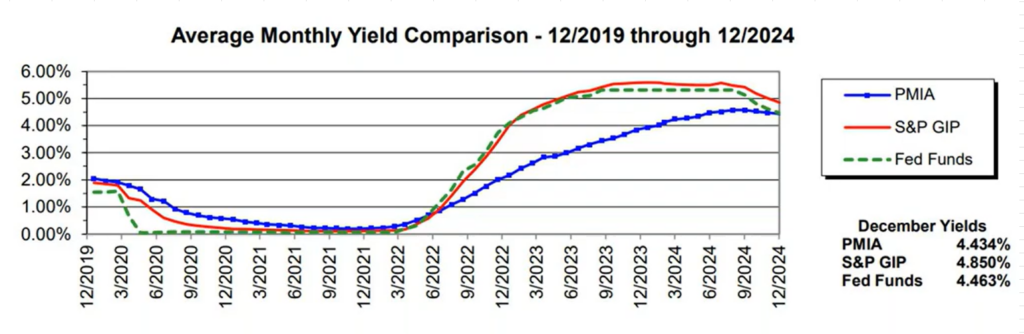

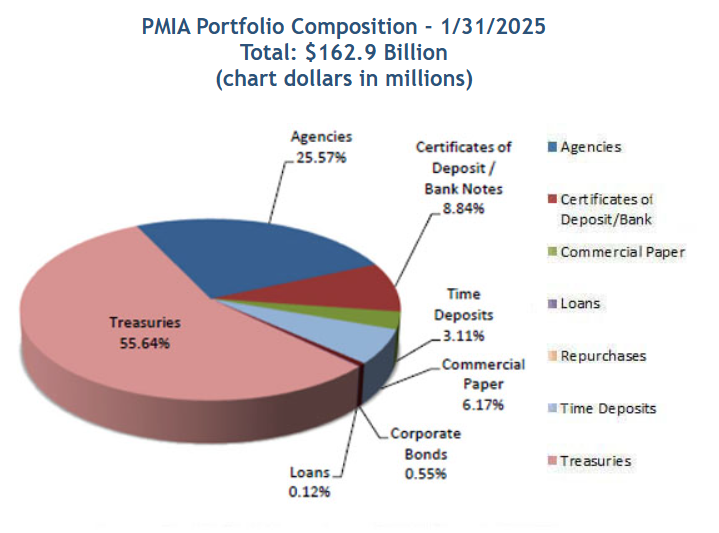

Three charts may help to inform: