Beyond the News: Risk, The New Obsession.

I’ve been thinking a lot about risk these days, and so should you. Some investment folks are paid to bet on risk (think hedge fund managers). For them, more risk is better—they just want to bet on the right side. But almost without exception public funds investors are expected to avoid risk, or at least to minimize it.

Until recently this has been straightforward, at least in concept. You might think about risk in two dimensions: one relates to the likelihood of default—and recovery. The second relates to market risk. In theory you might avoid risk entirely by investing in Treasury securities (“risk-free” they say) to the specific dates when payments are due. In the municipal bond world advanced refunding escrow accounts invested in the Treasury’s State and Local Government Series securities are the example. If the investment maturities and cash flows match debt service requirements then the underlying bonds are considered to be defeased—that is the issuer has no further obligation to pay.

Portfolio managers who seek to minimize risk avoid corporate bonds and other credit instruments and work to match portfolio cash flows to cash requirements. Using this approach avoids credit risk but may leave some residual risk in a portfolio related to market moves. If you match portfolio investment cash flows to your best guess as to cash flow requirements by investing in Treasury obligations, there is no market risk. If you are wrong—because cash flow requirements change—you might have to sell an investment prior to maturity or reinvest for a short term.

If you confine your investments to Treasuries, the “cost” of this risk is normally quite modest. Let’s say you invest $1 million in a 12-month Treasury bill earning four percent to meet an expected cash requirement, but the requirement is accelerated by one month. If you were required to sell the holding after 11 months and short-term rates were still 4% you would pay a dealer $25 or $50 to buy your Treasury bill (that is the bid/offered spread). If rates were 1.00% higher than at the time you purchased the bill, you would also lose something like $800 (the difference between book and market value). This would go against total earnings of about $36,700. So, your loss would be small, reducing the annualized earnings rate from 4.0% to 3.9%. (Needless to say, if rates were less than 4% at the time of sale you would have a modest gain.)

Credit risk is another story because impaired securities could end up being worthless, although in history investors who buy investment grade bonds usually recover something. (Reuters estimated that unsecured creditors of Lehman Brothers received about 41 cents on the dollar.)

So, if you avoid credit, have confidence in cash flow requirements and invest accordingly you can largely dismiss concerns over risk. And it follows that best practices advice has been highly focused on the importance of cash flow forecasting as a fundamental approach to investing public funds.

But things have changed and perhaps we should no longer assume that Treasuries are risk-free. There are some odd signs that the investment world has moved in this direction.

Until recently market turmoil–whether brought on by an international incident or domestic market moves (think a sharp drop in equity prices)–would lead investors to a flight to quality and they would rush to buy short-term Treasuries. The effect on short-term Treasury bill prices/yields would be noticeable. Prices would rally by ten, 20 or even 50 basis points in a matter of minutes as investors rushed to buy. Usually, when things settled down the trend would reverse, and they would fall back in line along the yield curve.

For example, the day before Silicon Valley Bank failed three-month Treasury bills were yielding about five percent. A week later they yielded about 4.40%, and a week after that they were back at 4.70%. So, a brief flight to quality.

The Lehman bankruptcy triggered a rally of nearly 1 50%(!) in short-term bills, which then gave up most of this a few days later.

But recently the market has behaved differently. “Liberation Day” when stocks lost nearly 10% of value? The three-month Treasury bill barely budged and over the next two days it lost only four basis points as the stock market sank further.

Perhaps Treasuries are not the haven they were once thought to be.

A second indicator that investors have less confidence in Treasuries is the level of credit default swaps on the United. States. Think of this as default insurance. Five-year CDS levels are now quoted at about 60 basis points, four times higher than Germany (remember how “troubled” the German economy is?) and three times higher than Japan (“old, tired economy”). They are at about the level of Italy and Greece, Europe’s weakest small economies.

Does that mean that the United States is likely to default on its debt? This seems highly improbable, though the credit rating of the U.S. is no longer AAA across the board, and it’s possible that Moody’s, the one credit rating organization that still rates U.S. debt in the top rating, could reduce it in the future.

But the CDS level does suggest that investors could be looking elsewhere to park cash.

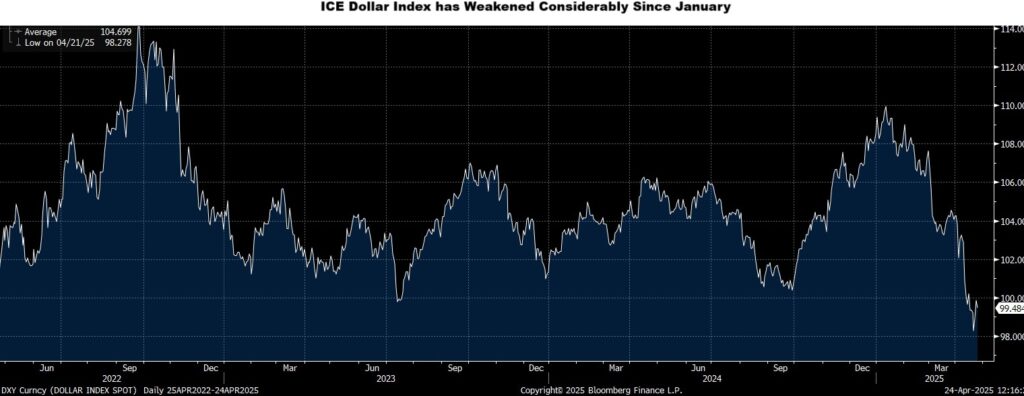

The decline of the US dollar compared to other currencies is another sign. The index of the dollar against a basket of currencies that is computed by ICE has lost about 10% of its value since January. Some (or most?) of the move may be a result of the ever-changing tariff policies of the Trump administration but something else may also be at work: a more general loss of enthusiasm for holding dollar-denominated assets.

Many analysts believe also that this is behind the increase in the term premium on long-dated Treasuries—that is the additional income that investors demand to buy/hold these bonds. It seems to have risen by one-half to one percent in recent months.

That would be consistent with the rise in CDS levels. It’s not that there is real risk in Treasuries defaulting, it’s. . . well. . .just that there is so much uncertainty that Treasuries (and dollars) may not be the best place to stash cash.

A weaker dollar might be good for the overall US economy since it will make our exports more competitive, but it will also tend to push up the cost of imports and thus the rate of inflation.

Whether in the long run we are better off remains to be seen. But higher risk premiums are not good under any circumstances, as they tend to pressure higher other rates like those on home mortgages, corporate borrowing, and municipal bonds.

This can be off-putting to investors. Indeed, that is the case with broad classes of investors from retirement account holders to hedge funds.

There’s not much that public funds investors can do about all of this, as the alternatives (Crypto? Gold? Foreign sovereign bonds?) may not be legal investments. And they have their own market-based risks that are many times those of Treasuries (if you are interested, look into the price volatility of these alternatives.)

There is also this saving grace: as long as the obligations of a state or local government are dollar-denominated the loss of value of dollar-denominated investments should not be worrisome because ultimately those investments will be deployed to pay dollar-based obligations (grants, transfer payments, employee salaries, etc.)

Meanwhile the short end of the market appears well-insulated from these forces. Yes, bond market volatility is elevated. The MOVE Index shown below presents a good picture of this: It is elevated but not out of range, as it is currently at about the average of levels observed over the past three years.

The MOVE Index represents volatility across the entire Treasury curve from two to 20 years, so it measures maturities that are not normally in public sector portfolios.

Another measure of volatility in the segment of the market that is the focus of most public funds investors shows remarkable calm. Since January 1, the intra-day yield of the two-year Treasury note has moved by more than ten basis points eight times, and its average intra-day move has been 4.9 basis points. In the comparable period last year, the yield move exceeded ten basis points seven times, and the average intraday move was 4.0 basis points. That’s not as sophisticated a measure as the MOVE Index, but it does tell a story.

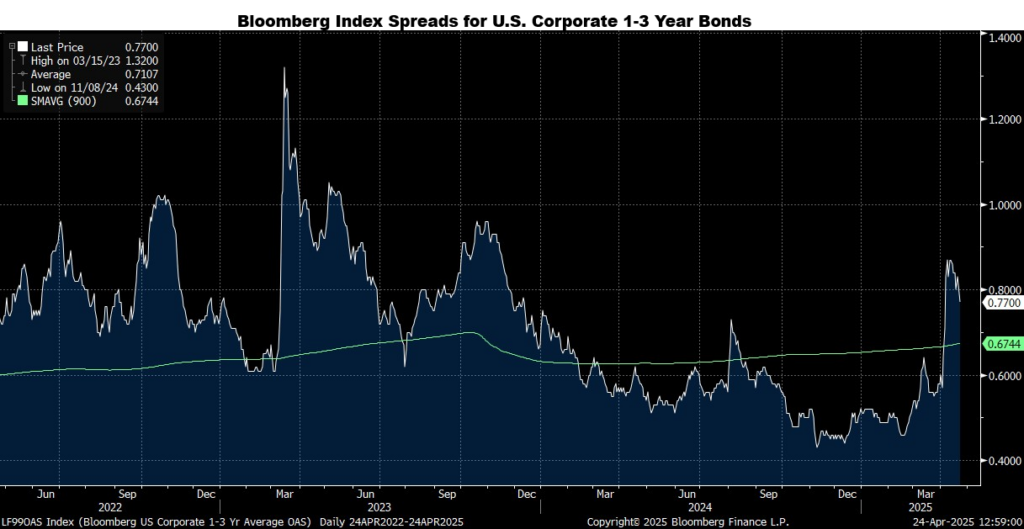

And credit spreads—the additional interest that investors demand to hold corporate bonds vs. Treasuries—have also been contained. A measure of this is the spread between the yield on 1–3-year Treasuries and that on 1–3-year investment grade corporate bonds. At this writing, as indexed by Bloomberg it is 77 basis points, which is somewhat above the average level (67 basis points) over the past three years.

It’s a way of illustrating this point: the water level seems to have risen for all boats floating in the dollar-denominated sea. There are plenty of scary headlines about elevated risk. But the risk has not (yet?) overtaken the short end of the markets.

It may be that tectonic shifts in the fundamentals of risk have barely moved the ground we’re on.