Fair Weather: Public Funds Investors Are Well-Positioned to Meet Investment Expectations

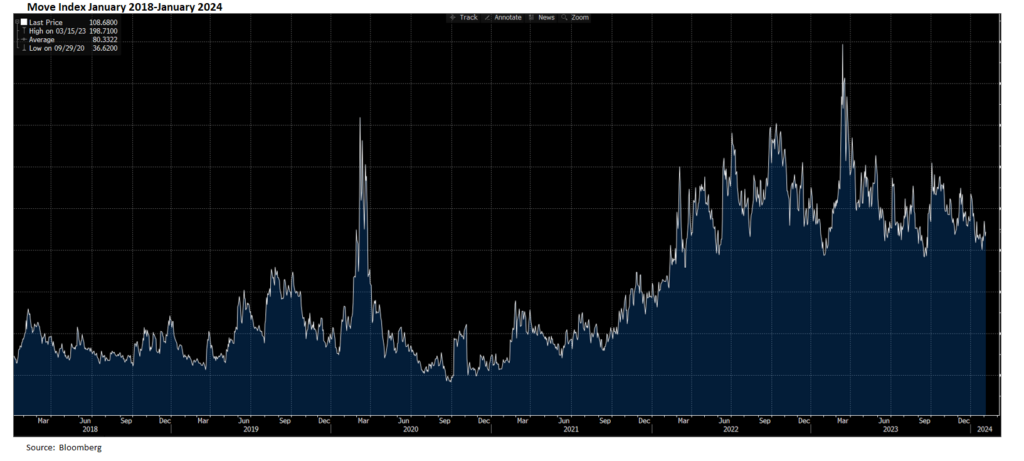

The accompanying chart of recent moves in yields speaks volumes about the current market environment and its implications for public funds investors. Since the year began short-term money market rates have been at or near their generation highs. And they have barely noticed the big moves in market sentiment. LGIP rates, as measured by the […]

Banking Crisis + 1 Year: Should Federal Deposit Insurance Reform Be Part of the Response?

A year ago, after the wreckage of the bank failures led by Silicon Valley Bank had been cleared, reforming deposit insurance was offered as a way to reduce the risk of future bank runs More recently, the effort has been sidelined by the battle over proposed rules to raise bank capital requirements and liquidity. Down […]

First Quarter Investment Returns: Cash Led the Way Again

• Local government investment pools and money funds once again produced market-leading returns in the 2024 first quarter. The beat by cash-type investments followed the strong showing for cash-type investments in 2023. • Returns of longer-duration portfolios were dragged down by a modest rise in interest rates. • The yield curve also worked against longer-duration […]

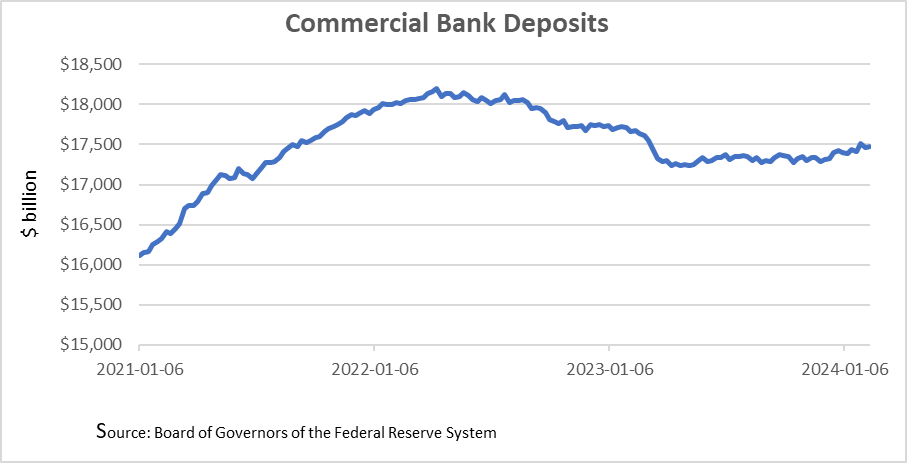

Public Sector Investment Assets Grew Strongly Last Year, Providing a Budget Cushion for States and Localities

The details. Investment assets grew by 7.5% last year, propelled by strong state and local tax collections, budget surpluses and investment earnings at rates that finished the year at their highest levels in a generation. The growth came after two years, 2020 and 2021, where Covid relief funds swelled state and local budgets. In that […]

More on Bank Capital Rules: The Fed Chair Speaks

If you were the CEO of one of the nation’s largest banks you might say that the most significant element of last week’s monetary policy report to Congress by Federal Reserve chair Jerome Powell was not about interest rates—“When will you cut them?”—or the state of the economy—“Are we in a recession or not?” Rather […]

Illinois LGIP Could Open a Pool for Non-Profits

Illinois by Nick Youngson CC BY-SA 3.0 Pix4free The Illinois Treasurer is seeking authority to create a local government investment pool for non-profit organizations. Senate Bill 3157 (and an identical bill in the House) would authorize a Non-Profit Investment Pool to operate in a manner similar to the Illinois Public Treasurer’s Pool (Illinois Funds), the […]

Local Government investment Pools: The Cash Keeps Flowing

Cash continues to pour into money funds and stable value local government investment pools. Assets of the stable value LGIPs rated by S&P Global grew by $71 billion or 23% in the 12 months ended February 9, 2024 to nearly $377 billion. Assets of money funds tracked by the Investment Company Institute rose to $6.001 […]

Basel III Endgame Could Change the Playing Field for Public Funds Investors

Opposition to the Basel III Endgame capital rules proposed by the federal bank regulators has intensified as the public comment period ended in mid-January, with new TV ads criticizing the proposal, a blizzard of comment letters filed with the regulators, and a flurry of Congressional hearings to warn of harm to bank lending if the […]

Prime Money Funds: How Changes Could Affect Public Funds Investors

Plans by a little-known money market fund to alter its investment strategy could be a harbinger of changes to the industry that have significant implications for public funds investors. The implications are three-fold: 1) state and local governments invest in money funds directly and some local government investment pools (LGIPs) invest in them as well, […]

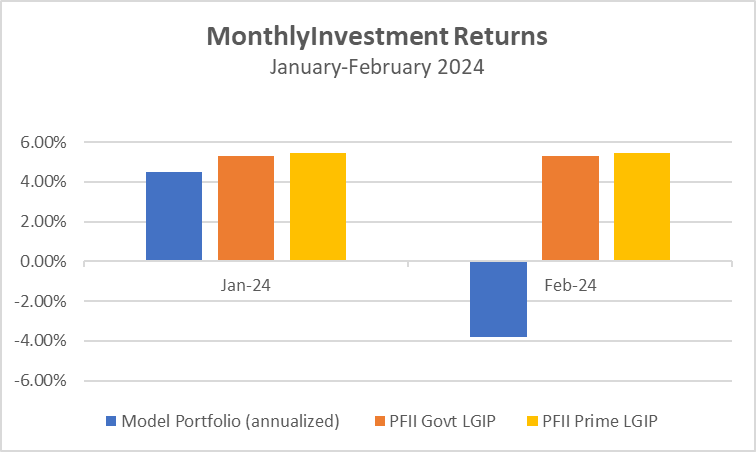

Beneath the Surface: Market Volatility Remains

January was not a kind month for bonds. On the surface, all was well. LGIP rates were largely static in the month and the yield on the two-year Treasury—a good bell weather for separately managed public funds portfolios—ended the month not much above where it started. But beneath the surface heightened volatility prevailed. There is […]